| Review | Open Access |

|---|

Environmental Attitude and Green Competitive Advantage: Mediating Roles of Green Production Strategy and Environmental Management Accounting in Pakistan’s Manufacturing Sector |

|

|---|

![]() Muhammad Hamza Khan* and Atique Ahmad

Muhammad Hamza Khan* and Atique Ahmad

Hailey College of Commerce, University of the Punjab, Lahore, Pakistan

The current study aimed to explore the nature of manufacturing sector in Pakistan, the interactions between Environmental Management Accounting (EMA), attitude towards risk, Green Competitive Advantage (GCA), and Green Production Strategy (GPS). Therefore, in line with the quantitative research paradigm, the study explored how these constructs exist within the framework of environmental attitudes within Pakistan’s relatively heterogenous manufacturing environment. The results suggested that a positive attitude towards risk facilitates both EMA and GPS, leading towards a competitive advantage. Nevertheless, the association between attitude towards risk and GCA is not very strong, suggesting areas worth further investigation. GPS findings underscored the necessary and compelling need to promote an environmental management culture with regard to sustainability within enterprises. In light of certain issues that are currently besetting manufacturing industries in Pakistan, such as issues of quality and compliance among others, this study offered insights to policymakers in the industry who wish to upgrade on their efficiency and competitiveness.

1. INTRODUCTION

As global environmental problems are getting severe, knowing how managers' perceptions of sustainability determine organizational capital is relevant, especially in Pakistan, where the need for efficient environmental management is increasing (Ahmad et al., 2020). By comparing the results, it may be noted that there are very few publications on the attitudes of managers of different countries and companies related to environmental problems and their solutions (Taqi et al., 2021). Furthermore, the literature review on the psychological factors and perceptions held by managers regarding the environment is scarce in the developing world, particularly in Pakistan. Therefore, due to environmental pollution in Pakistan, there is a need to adopt Environmental Management Accounting (EMA) in order to advance environmental protection.

Concerning Michael's force model, an area or field of interest most directly observable in the given case of strategic management is marked by the influence of organizational, firm-level strategy, and actions on the individual forces at play due to the pivotal role of strategic choices made by top managers in shaping the overall organization (Dwirandra & Astika, 2020). The externalities also influence the strategies employed by firms to address environmental concerns, while internal factors are equally significant. The Green Production Strategy (GPS) helps in the cause of environmental conservation; the conventional structure of GPS fosters the organizational GCA (Namazi & Rezaei, 2024).

Some research has been conducted on Green Competitive Advantage (GCA) in recent years. For instance, Damerji and Salimi (2021) revealed that green core competencies enhanced GCA and that green intellectual capital has a positive relationship with GCA. Moreover, theoretical and empirical literature revealed that upper managers' characteristics, strategic choice behavior, information systems design and use, and organizational performance are related (Cruz & Manata, 2020). Still, the connections between the attitude towards the environment, the GPS, EMA, and the GCA have not been investigated well enough by researchers.

Originally, the UET model was the life of 1984 without a moderating variable. However, Cullen et al. (2020) incorporated the variable of managerial discretion as a moderating variable consisting of three categories. As much as Dwirandra and Astika (2020), the moderating variable in UET is involved in the process of decision-making. The Government of Pakistan, over the recent years, seems to have developed a concern pertaining to the issue of environmental protection (Ahmad et al., 2020). The current National Environmental Policy of Pakistan, formulated in 2022, applies to all organizations running businesses in Pakistan, especially how they execute their manufacturing strategies (Taqi et al., 2021). In this regard, regulatory pressure is an external environmental characteristic which defines the choice of GPS and utilization of the EMA information. In light of the global environmental issues, corporate organizations should ensure that the environment is merged into the company's accounting system as well as environmental responsibility reporting.

The current research is a significant contribution towards filling the literature gap given that it develops a conceptual framework, connecting manager's environmental attitudes, GPS choices, EMA, and GCA. Firstly, the study analyzed if there is a relationship between (1) managers' environmental attitudes and the decision towards a green production approach and (2) managers' environmental attitudes and the EMA approach (Caputo et al., 2021). Taking Pakistan's transition economy as its context, the study provided evidence of the impact of environmental attitudes on managerial behavior in GPS and EMA choice in managerial decision-making. Generally, the existing literature has been silent as to how can managers contribute best to the enhancement of GCA towards manufacturing enterprises in Pakistan. Notwithstanding the countrywide escalating interest in environmental management practices, EMA is under researched in Pakistan's manufacturing industry. Although, the relevance of EMA in terms of providing impetus to the practice of sustainability and its potential on managerial decision-making process in emerging economies has often been under explored, particularly in industries on a path to green, the scope of opportunity still offers a great deal of promise.

The current study highlighted the human factor of upper management's environmental attitudes in forming administrative behavior towards the adoption of corporate GCA strategies in businesses. The study is organized as follows: the existing literature of EMA, GPS, and GCA is reviewed in section 2. Section 4 comprises analysis of the findings based on the research methodology and data collection process described in section 3. Section 5 concludes with policy implications and directions for future research.

Literature Review

The EMA has developed as a key dimension to put sustainability in place, for organizations. EMA collects, analyzes, and uses environmental data for support to make management decisions and to enhance environmental performance (Dwirandra & Astika, 2020). Previous studies have revealed that EMA reduces the decision-making time of managers by providing them detailed information related to the environmental costs that have resulted from productions' processes. This allows them to identify the opportunities of cost saving and sustainability improvement (Ahmad et al., 2020). Although, EMA is often used in developed economies, its use in other emerging economies, such as Pakistan, is still unexplored, as EMA could contribute to greener practices and support environmental decision-making (Taqi et al., 2021). Integration of EMA in Pakistan's manufacturing sector could lead to environmental as well as economic benefits by increasing competitiveness and operational efficiency.

Another critical variable, that is, GPS directly impacts a firm's capability to decrease environment affects while maintaining product excellence and profit. GPS encompasses a variety of practices, such as energy-efficient production, waste reduction, and the use of eco-friendly materials (Kazancoglu et al., 2021). GPS adoption is a way to gain a competitive advantage, such as cost savings, regulatory compliance, and an improved brand reputation. To meet the rise in consumer demand and international environmental standards in Pakistan, the manufacturing sector is now putting into practice the use of GPS. (Tan & Zhu, 2022). Nevertheless, slow adoption of GPS is attributed to the financial constraints, lack of awareness, and limited access to green technologies. This highlights the need for research into what determines the adoption of GPS in the country.

Upper Echelons TheoryScarpellini et al. (2020) conceptualized a top manager's characteristics model that explains organizational business environment interaction, strategic decision-making, and organizational performance. Additionally, the use of psychological factors was introduced into financial accounting and auditing a decade ago. Taking the primary method of quantitative research, the psychological attributes defined for the field of accounting and auditory include low levels of self-esteem, self-interest, negativity towards risk, and positivity towards risk (Hanlon et al., 2022).

Examining the impact of momentum, Shahab et al. (2020) underscored psychological characteristics in the top managers. While at the same time, substantial weight was given to the backdrop components, as a result of the fundamental issues that arise when attempting to measure the underlying cognitive structures and beliefs of the prefrontal cortex and framework of the top executives. More investigation is needed to explore the psychological factors that convert the background variables of top managers into strategic choices using control systems and performance (Ali et al., 2022). As mentioned by UET, one of the most important deficiencies of the studies currently available in the literature regarding research models is that while there are very few studies in which the performance is represented as a dependent variable, the FP only is taken into consideration in the models but no attention is paid to the GCA (Bassyouny et al., 2020; Tian, 2022).

Managers' Attitude towards the EnvironmentPersonal values and attitudes are assumed to be the two most salient aspects of human psychology (Tan & Zhu, 2022). In the previous research, two different kinds of environmental attitudes have been distinguished. This study included two types of environmentally-relevant attitudes proposed by Debrah et al. (2021): (1) attitude towards the environment, and (2) attitude towards organic performance. The perceptions of ecological behavior are covered in only a small part of the study on this theme. However, it is relevant to assert that environmental concern is as close as having a positive environmental attitude (Kazancoglu et al., 2021). This term refers to the natural or inherent behavioral dispositions residing in the human character that influence environmental behaviors (Sabirov et al., 2021). The review of personal values includes the phrase 'attitude towards the environment'. To some extent, attitude towards the environment is concerned with a person's predetermined disposition towards a specific behavior (Munawar et al., 2022). According to Song et al. (2021), an environmental attitude refers to what a person believes, perceives, and intends to do amid environmental stimuli and tasks.

Green Production Strategy (GPS)Environmental management strategy relates to the extent to which environmentally-sustainable features have been placed into the strategic planning of the firm (Blomé et al., 2020). Environmental measures are often more legislative or competitive than value-based. In today's manufacturing, the GPS is the realization of sustainable development strategy. It is quite common for the term "green" to be substituted with "sustainable". In the context of green production, it involves the use of environmentally friendly materials, the adoption of sustainable methods and processes, the achievement of eco-friendly outcomes, and ultimately, products that are less harmful to dispose of at the end of their lifecycle (Zameer et al., 2020).

Environmental Management Accounting (EMA)D'Souza et al. (2006) defined EMA as the process of identifying, accumulating, analyzing, and using information about costs and other resources. This supports organization's environmentally and economically sustainable management decisions. EMA would be a helpful system for managers as it may assist them to minimize their company's contribution to environmental degradation. Moreover, it may also help make right decisions as they face pressures from the outside world (Baines et al., 2012). The EMA information may be utilized by managers to identify, acquire, apply, and interpret financial data to make appropriate environmental management decisions. EMA utilizes information from environmental and economic accounts to explain how managerial decisions impact a company's financial performance (Albino et al., 2009). An example of such a system is EMA which facilitates collection, storage, aggregation, and analysis of data on the environment. EMA may give information to the management of the potential for lowering pollution and, thus, could also facilitate the decision-making and performance management processes (Rehman et al., 2023).

Green Competitive Advantage (GCA)Competitive advantage is stated as the ability or position of the organization in relating to competition in terms of resource utilization (Nuryanto et al., 2020). Therefore, in this study, to achieve sustainable development, GCA was included as an important feature. A workplace would have GCA when it deploys a particular approach that entrants cannot attain or may not be able to attain in the future or when competitors can derive similar value. Thus, the association GCA would assign to it would be a relative rank in the business. They also achieve a GCA when they are able to introduce different goods that are recognized and respected by the buyers. Such products cannot be segmented hence, counterfeited by the contestants (Chen, 2007; Muisyo et al., 2022).

Hypotheses DevelopmentCorporate environmental strategy is also an organizational competency since it entails the use and integration of multiple perspectives (such as the manager's attitude and knowledge) to attain a specific goal (Papadas et al., 2019). Board perception of environmental issues impacts opportunities for and use of voluntary environmental strategy (Chiou et al., 2011). Concerning the natural environment, it is expected that firms with managers who are positively disposed towards the environment would be more concerned with natural environmental problems (Chang, 2011). An owner-manager who has an appreciation for the natural surroundings is critically important in both the development and the sustenance of the firm's contained deliberate environmental management strategy (Chen & Cao, 2023). GPS aims at minimizing the environmentally degrading effects of the production processes as well as the desire for economic profits. By doing so, this would help to bring down the impacts that the organization has on the environment in which it is situated.

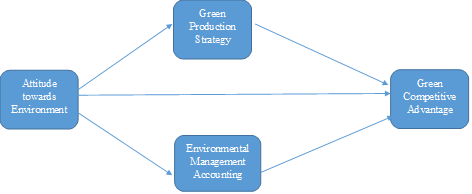

H1: Managers' attitude towards the environment would have a positive impact on GCA.

Eco-friendly entrepreneurship entails the undertaking of active environmental activities to achieve competitive benefits and to counterbalance several market inefficiencies (Muisyo et al., 2022). The goal of sustainable development is to create chance for the enhancement of goods and manufacturing methods that meet the expectations of people (Waqas et al., 2021). This is because customers are becoming more and more concerned with and are beginning to require the goods that they consume to be ecologically responsive (Riva et al., 2021). An environmental management strategy that establishes social responsibility as the organization's strategic theme perfectly aligned with the core business of the enterprise can be a strong competitive weapon (Setyaningrum et al., 2023). Green production may enhance an enterprise's competitive edge; choosing to go green meets the needs of green consumers.

H2: GPS would have a positive impact on GCA.

The study found that there is a positive performance implication of adopting EMA in organizations (Ribeiro & Steiner, 2021). Undoubtedly, the adoption of EMA compels organizations to develop tactics that would enhance their competitive strategies in the ecological marketplace. Here, executives have realized that the highest value of EMA is to identify potential opportunities in order to enhance the organizational reputation and make strategic decisions in the corporation (Zameer et al., 2021). Particularly, EMA enactment enhances environmental management and efficiency. Most notably, utility cost and pricing strategies, resource utilization, revenue generation, and market access promotion of the businesses and investment capital are enhanced (Gürlek & Tuna, 2018). EMA allows managers to understand the conflict between economic gain and harm to the environment. Moreover, it helps determine how to minimize the negative effects on the environment and at the same time increase economic performance.

H3: EMA would have a positive impact on GCA.

Literature has supported the role of GPS in improving GCA (Saputra et al., 2023). A favorable attitude towards the environment advances the common practice of green production in organizations which, in turn, enhances the competitiveness of the firm by positively influencing its environmental standing and perception (Bintara et al., 2023). This suggests that green production is targeted at achieving superior environmental outcomes through competitive advantages that firms with proactive environmental stance factors employ (Lin & Chen, 2017). Such strategies include the exploitation of resources in a sustainable manner and using environment-friendly methods of production. This enables a firm to deploy a competitive strategy in a given market. Therefore, it is theorized that GPS would dramatically mediate the environmental attitude and GCA, demonstrating the importance of attaining competitive success.

H4: The relationship between attitude towards the environment and GCA would be significantly mediated by GPS.

EMA's solution confirms that positive environmental attitudes can be translated into tangible competitive benefits for firms (Cao et al., 2022). EMA is the process of including environmental costs and benefits in the overall financial decision-making. This helps a firm to pursue sustainable practices towards the achievement of a GCA. The literature has found that organizations with a clear focus on the environment are more likely to incorporate EMA practices, thereby achieving improved environmental outcomes and competitive advantage (Arseculeratne & Yazdanifard, 2014). EMA enables enhanced environmental reporting, control over costs, and strategic planning that may greatly affect the GCA of a firm by integrating financial and environmental objectives (Esty & Winston, 2009). Consequently, the research assumes that EMA would contribute largely to the interaction between the attitude towards the environment and GCA. Hence, there is a need to incorporate the environmental perspective into the financial management function.

H5: The relationship between attitude towards the environment and GCA would be significantly mediated by EMA.

Figure 1.

Conceptual Framework

Methodology

Variable MeasurementThe study used a standardized instrument to assess the variables. Environmental attitudes were measured by the scale developed by Dunlap et al. (2000) of ecological concern present in each respondent. GPS was assessed based on Zameer et al. (2020) in which the extent of environmentally-sustainable production practices was captured. EMA was assessed in view of the features identified by Chaudhry and Amir (2020), mainly regarding the incorporation of environmental costs into financial decisions. Lastly, GCA was evaluated following Lin and Chen's (2017) scale, establishing the capacity of a firm to obtain competitive edge through sustainability.

Sample CollectionManufacturing firms in Pakistan were selected for this study due to the significance of environmental strategy, EMA deployment, and environmental performance for these organizations. Thus, the study population was limited to the listed manufacturing firms in Punjab, Pakistan. This is because these organizations reflect the country's manufacturing industry perfectly and may report reliable information about their environmental attitudes, strategic choices, and EMA adoption. A cross-sectional research design was used and sample was collected through convenience sampling technique. When conducting a survey, it is paramount to make sure that the sample used represents the population being studied.

Convenience sampling is a non-probability sampling technique which was adopted in this study as the level of variation in the population is low or irrelevant (Hair et al., 2019). In this case, various manufacturing enterprises' managers possess similar characteristics and responsibilities. Furthermore, this method is also cheap as compared to other methods and may encourage timely data collection.

Since probability sampling methods including the stratified or the simple random sampling are deemed more scientific, they could not be adopted for a number of reasons. Firstly, it is difficult, time-consuming, and expensive to compile and access a sampling frame of all managerial population in the manufacturing sector in Pakistan. This is because the list of managerial population is often scarce or difficult to obtain. Secondly, due to managers' non-acquaintance with survey research in Pakistan, compounded by time constraint and limited respondent readiness, probability-based methods were not feasible.

Convenient sampling, on the other hand, made it easier for the researchers to obtain data from any willing participants. Therefore, the researchers were able to ensure that the sample size was large enough to meet the recommended power for Partial Least Squares Structural Equation Modelling (PLS-SEM). To reduce external validity problems associated with convenience sampling, the study aimed at a sample of 320, which is also above the recommended number of respondents for PLS-SEM analysis. Additionally, bootstrapping procedures were conducted to increase internal and external validities of the sources of support since the study was limited by the convenience sampling approach.

A total of 500 formal copies of the questionnaire were administered in total. The survey questionnaire was distributed to a sample of 420 managers working in the manufacturing industries of Punjab. The managers were identified based on their email addresses from different sources, such as enterprise websites, industry associations, and business networks. Out of the 420 surveys conducted, 328 were considered fit for use. To reduce the risk of sample bias, which may be an issue in convenience sampling, the following steps were taken. This was a comprehensive review of the literature which was conducted using constant prompts (Fink, 2015). To reach the managers, a letter of invitation was emailed to their personal email address which included a link to the online survey. The managers who were extending the invitation responded that they would like to participate by clicking on the link to the web-based questionnaire. Some of the limitations inherent in this methodology included response errors and non-response which affected the precision of estimates and, therefore, the external validity of the study conclusions (Creswell & Zhang, 2009). In response to these concerns, measures were taken whereby, contact was made with the concerned parties, incentives were provided to ensure compliance, and later, follow-up was made by sending reminder emails. In cases where there was no response, consent letters were followed by reminders that were sent at three weekly intervals for three weeks after three months of the initial invitation.

Method of AnalysisThe method of analysis applied in this research involved PLS-SEM under SmartPLS4. PLS-SEM is a highly appropriate statistical method utilized to conduct both exploratory and confirmatory analysis. It makes it possible to estimate the models with complex cause-effect relationship when some of the variables involved in the research model are latent. It is best applied in models which have formative and reflective measures and is helpful in cases where sample sizes are relatively small, or the data is non-normal, both of which are not uncommon in the social sciences.

Results

Table 1:

Measurement Results

| Parameters | Factor Loadings | α | CR | AVE |

|---|---|---|---|---|

| ATE | 0.793 | 0.794 | 0.548 | |

| ATE1 | 0.786 | |||

| ATE2 | 0.729 | |||

| ATE3 | 0.763 | |||

| ATE4 | 0.740 | |||

| ATE5 | 0.679 | |||

| EMA | 0.785 | 0.787 | 0.540 | |

| EMA1 | 0.804 | |||

| EMA2 | 0.681 | |||

| EMA3 | 0.657 | |||

| EMA4 | 0.800 | |||

| EMA5 | 0.721 | |||

| GCA | 0.776 | 0.781 | 0.597 | |

| GCA1 | 0.783 | |||

| GCA2 | 0.797 | |||

| GCA3 | 0.754 | |||

| GCA4 | 0.755 | |||

| GPS | 0.698 | 0.746 | 0.532 | |

| GPS1 | 0.747 | |||

| GPS2 | 0.842 | |||

| GPS3 | 0.790 | |||

| GPS4 | 0.487 |

Attitude towards risk also proved to have an internal consistency where Cronbach alpha (α) equals 0.793, Composite Reliability (CR) was 0.794, and Average Variance Extracted (AVE) was 0.548. The alpha coefficients (ATE1 to ATE5) reveal high factor loadings and ranging from 0.679 p < 0.05 to 0.786 thus, signifying acceptable evidence of the construct. In the current study, EMA also gave good reliability figures as measured by α of 0.785, CR of 0.787, and AVE of 0.540. The factor loadings for EMA items (EMA1 to EMA5) ranged from 0.657 to 0.804, in their capacity to measure the construct of EMA in decision-making and in relation to environmental performance. GCA showed a slightly higher reliability than resource allocation but had a lower Cronbach's alpha of 0.776 and a CR of 0.781. However, it showed a higher AVE of 0.597 which suggests that the model extracts more variance than some of the constructs. The loadings of GCA1-GCA4 ranged from 0.754 to 0.797 in support of their usefulness to assess this construct. Finally, in GPS, the lowest reliability in terms of α of 0.698 and CR of 0.746 and AVE of 0.532 was obtained. Indeed, the loadings for GPS items (GPS1 to GPS4) were quite different and GPS4 which loads at 0.487 was lower than the rest and may not be a very good reflection of the true construct.

Table 2:

Hetrotrait-Monotrait Ratio (HTMT) Correlation

| HTMT | |

|---|---|

| EMA<-> ATE | 1.080 |

| GCA<-> ATE | 0.416 |

| GCA<-> EMA | 0.464 |

| GPS<-> ATE | 0.973 |

| GPS<-> EMA | 1.005 |

| GPS<-> GCA | 0.428 |

More specifically, when comparing the practices of EMA with the ATE, the Hetrotrait-Monotrait Ratio (HTMT) value equals to 1.080 which is over the allowable threshold of 1.0. This raises the question of discriminant validity, where these frequently seem to be too close or too similar in the definitions of these constructs. The result is contrasted to the logic, showing that GCA has a moderate positive relationship with ATE, HTMT value of 0.416 which is sufficient to maintain some uniqueness. Additionally, the HTMT value of 0.464 between GCA and EMA adds to the idea that the two are related, however, distinct. The relationship between GPS and ATE has an HTMT value of 0.973 closer to 1 but below 1.0. This suggests that there is a strong positive relationship between the two while at the same time recommending that the two are separate constructs. However, the value of HTMT equals to 1.005 between GSP and EMA which also indicates the poor discriminant validity of the construct. Finally, when comparing the GPS and GCA, the HTMT value of 0.428 means that the relationship is weak to moderate. Therefore, the chosen constructs are quite distant from one another.

Table 2:

R-Square, Adjusted R-Square, and p-values

| R² | Adjusted R² | p | |

|---|---|---|---|

| EMA | 0.735 | 0.734 | 0.000 |

| GCA | 0.139 | 0.131 | 0.015 |

| GPS | 0.565 | 0.563 | 0.000 |

Regarding the EMA, the coefficient of determination, R² is 0.735 which means that 73.5% of the changes in this construct can be explained by changes in the independent variables in the equation. The adjusted R-Square is slightly lower at 0.734, meaning a very good fit, with regard to the number of predictor variables. Moreover, the F-test chi- square value of 72.85 is significant at 0.000. Therefore, the conclusion is that this model is quite robust. On the other hand, GCA gets little higher value of R² which is 0.139. This means that only 13.9% of its variance is attributed to the independent variables. The adjusted R² is slightly lower at 0.131, showing more simplistic explanation of the data. However, the coefficients indicate that this relationship is only statistically significant at the p-value of 0.015, meaning that while it exists it has a weak predictive power. For GPS, the R² value is 0.565 which implies that 56.5% of GPS data variation is explainable by this set of independent variables in the model. Adjusted R² is reasonably high at 0.563 which gives independent measures test of model fit while accounting for predictor variables. The applied model is relevant because the p-value of 0.000 shows significant statistical significance.

Table 4:

Hypotheses Testing

| Path Coefficient | p | Results | |

|---|---|---|---|

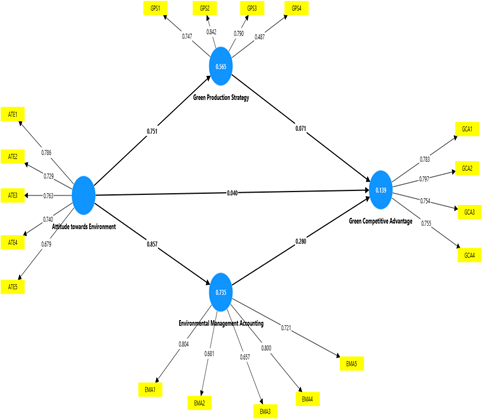

| ATE -> EMA | 0.857 | 0.000 | Accepted |

| ATE -> GCA | 0.040 | 0.737 | Rejected |

| ATE -> GPS | 0.751 | 0.000 | Accepted |

| EMA-> GCA | 0.280 | 0.008 | Accepted |

| GPS-> GCA | 0.071 | 0.439 | Rejected |

The results established a statistically sound positive relationship between ATE and EMA with the path coefficient of 0.857 and p-value of 0.000. Consequently, this hypothesis is accepted, implying that there is a significant relationship between positive ATE and environmental management practices. In contrast, the relationship between ATE and GCA has an insignificant path coefficient of 0.040 and a p-value of 0.737. Therefore, based on this hypothesis, this is a rejection which means that attitudes towards the environment do not improve on the basis of competition advantage. The study of the ATE construct and GPS further confirms this hypothesis with path coefficient being 0.751, p-value of 0.000. This implies that perceived self-efficacy with regard to environment and attitude has a positive relationship with green production strategies. Additionally, the mediating role of EMA on GCA has a path coefficient of 0.280 and a p-value of 0.008, showing a positive impact relationship. Thus, based on the findings of the research, this hypothesis is accepted, suggesting that EMA would lead towards competitive advantage. Last of all, green production to GCA has a path coefficient of 0.071 with a p-value of 0.439, exhibiting no impact. Therefore, this hypothesis is rejected, implying that green production strategies do not significantly cause the improvement of competitive advantage as presented in this analysis.

Discussion

Considering Upper Echelons Theory by Hambrick & Mason (1984), it is specifically noted that managership traits of the top management play an important role in determining the strategic organizational impacts including environmental management. The use of this theory in the Pakistani manufacturing sector explains how the decision-makers' individual values and beliefs, past experiences, and psychological characteristics shape the environmentally sustainable practices. In other words, only the chief executors with the proactive ATE would succeed in implementing EMA into strategic management. This accords with the theory advanced here that managers' cognitive preconditions and values may influence organizational decisions including choosing between profitability and environmental sustainability (Manners et al., 2021).

The factor loadings show more or less reliability and validity of the constructs, such as ATE, EMA, and GPS. For instance, with the reliability estimate of 0.785, the results from EMA can be considered highly reliable, while GPS has a slightly lower estimate of 0.698. This difference highlights the need to revise the measurement items for GPS so that the reliability may be improved. Firstly, literature review states that strong practices of management accounting may help to incorporate environmental factors into cost decisions, particularly when it comes to developing countries. Hence, it becomes critical to have appropriate measurement instruments. The instruments may measure these constructs adequately in the context of emerging markets, such as Pakistan where manufacturing firms are under growing pressure to manage sustainability challenges.

The results also provide more understanding about the linkage between ATE, EMA, GPS, and GCA. Consequently, as per Upper Echelons Theory, managers ATE is the key to implement EMA, which affects the extent of GPS optimization within organizations. The scheme between EMA and GPS is working. EMA offers the environmental information which is fed into GPS thus, helping the organization to monitor and evaluate their green performance. Altogether, these constructs enhance the GCA of an organization as it caters environmental issues to strategy and operation and places firms advantageously in a market environment which is progressively shifting towards sustainable developments (Liang et al., 2022).

Furthermore, the HTMT value of correlation enhanced discriminant validity of the constructs as compared to the analysis of latent variables directly. The correlation of ATE is high with EMA which makes it quite possible that there is confusion on what ATE and EMA are. The above literature observed a problem with combining between management practices and the organization's attitudes to the environment for these reasons (Jermsittiparsert et al., 2020). This challenge conjoined with the cognitive bases of managers. Upper Echelons Theory might help explain why certain organizations still find it difficult to distinguish their strategic behaviors in order to address environmental goals.

The analysis of the squared R-VA values confirms the usefulness of the models for explanation. Hypothesis 2: EMA has a positive impact on appointment attendance.

The above residuals model establishes the goodness of fit to the extent of contextualizing EMA in the equation above by presenting an R-Square of 0.735 thus, making the model exhibit high robustness. This supports the argument that firms with top managers' interest in environmental affairs establish robust environmental management systems leading towards improved green operational performance and GCA (Khan et al., 2023).

Specifically, as compared with other variables, the reliability of GPS and EMA was relatively low, and the discriminant validity was relatively poor as the HTMT ratio was higher than 1.0. To this end, the items with the lower factor loadings were subsequently reviewed and any items which were either ambiguous or duplicative of other items were eliminated or reformulated. Furthermore, bootstrapping methods were employed to improve the degrees of freedom and thereby make the estimation comparatively more accurate. There was also a marginal increase in reliability and discriminant validity, especially for GPS, based on the final modelling, thus achieving the concept clarification goal of the study.

Conclusion

In conclusion, the study of the correlation between EMA, GCA, and GPS shows the complex interdependency between these constructs and how they affect the organizational performance. The current study revealed that positive ATE facilitates EMA and GPS that are important determinants in the promotion of sustainability in organization. This highlights the need for and direct attention towards the development of environmental management culture to support management accounting practices and strategies. However, the results also have some drawbacks, particularly in terms of limited relationship between ATE and GCA. This means that when organizations adopt a positive environmental attitude as well as establish positive environmental practices, this does not necessarily mean that the organization would come up with competitive advantages. Therefore, this lack of correlation requires expansion of literature on external conditions and market forces that could affect competitive strategy other than the management practices. It is crucial for organizations wanting to use sustainability as a strategic asset to grasp these subtleties. Furthermore, the alterations in the value of R-Square of different constructs suggest a difference in the extent of the explained variance. In its first dependent variable, EMA shows a high performance in variance explanation, although GCA presents a narrower explanatory sphere. This means that other factors could be external or contextual and may sway competitive advantage greatly but were not captured in this study.

Future Implications

The implications of this study have meanings to organizations intending to improve on their effective and optimal control of the external environment and their competitive strategies. The positive significances of ATE, EMA, and GPS highlighted in this study indicate that creating awareness and commitment towards the environment is a critical factor for organizations desirous to enhance their sustainability. As such, emphasizing positive environmental attitudes may help improve EMA practices. Hence, it would increase the efficiency in ways resources are used in companies. Moreover, the adoption of hypotheses associating EMA with GCA reveals that environment management is essential to achieve competitive advantage in the market. Therefore, organizations should ensure that they embrace training and awareness programs to encourage practicing of environmental management resulting in better performances and relationships with stakeholders.

Limitations

There are a number of limitations to be discussed in the framework of this research. One of the important limitations is that the scores on the chosen constructs may be affected by the measurement bias, especially due to the fact that attitudes towards environmental management and the actual practices are based on the respondents' self-reporting. Such reliance on subjective measures might simply lead to the gap between what people claim to do and what they actually do, as evidenced by other authors (Bennett & James, 2017). Furthermore, the applicability of the findings to other industries may also be somewhat constrained. Further research should be extended to involve a wider group of industries and locations in order to increase the generalizability of the findings. Moreover, a cross-sectional research design was used which would limit them from making causal cross-sectional conclusions over time; longitudinal research method of study would be even more informative.

Future Research Directions

The correlation between GPS and GCA appears to be relatively weak, which may be attributed to factors that are specific to certain industries and cultural contexts. In the context of Pakistani manufacturing sector, short-run cost considerations may potentially trump strategic sustainability objectives to a degree that GPS seems to offer few advantages. However, there is a possibility that the awareness and commitment to practice green in the production of manufacturers would not be well-implemented. Moreover, the use of GPS in sample studies might not entirely reflect the details of technique responsible for the achievement of competitive advantage. This means that if the measurement items for GPS are either broad or do not correspond to present practice, there may be a misalignment between what is introduced in the field of GPS and the organizational results expected from the provided strategies. Subsequent research needs to determine the subtleties of deploying GPS to enhance comprehension of its effects on GCA.

Conflict of Interest

The author of the manuscript has no financial or non-financial conflict of interest in the subject matter or materials discussed in this manuscript.

Data Availability Statement

The data associated with this study will be provided by the corresponding author upon request.

Funding Details

No funding has been received for this research

REFERENCES

Ahmad, W., Kim, W. G., Anwer, Z., & Zhuang, W. (2020). Schwartz personal values, theory of planned behavior and environmental consciousness: How tourists' visiting intentions towards eco-friendly destinations are shaped? Journal of Business Research, 110, 228–236. https://doi.org/10.1016/j.jbusres.2020.01.040

Albino, V., Balice, A., & Dangelico, R. M. (2009). Environmental strategies and green product development: An overview on sustainability-driven companies. Business Strategy and the Environment, 18(2), 83–96. https://doi.org/10.1002/bse.638

Ali, R., Rehman, R. U., Suleman, S., & Ntim, C. G. (2022). CEO attributes, investment decisions, and firm performance: New insights from upper echelons theory. Managerial and Decision Economics, 43(2), 398–417. https://doi.org/10.1002/mde.3389

Arseculeratne, D., & Yazdanifard, R. (2014). How green marketing can create a sustainable competitive advantage for a business? International Business Research, 7(1), 130–137.

Baines, T., Brown, S., Benedettini, O., & Ball, P. D. (2012). Examining green production and its role within the competitive strategy of manufacturers. Journal of Industrial Engineering and Management, 5(1), 53–87. https://doi.org/10.3926/jiem.405

Bassyouny, H., Abdelfattah, T., & Tao, L. (2020). Beyond narrative disclosure tone: The upper echelons theory perspective. International Review of Financial Analysis, 70, Article e101499. https://doi.org/10.1016/j.irfa.2020.101499

Bennett, M., & James, P. (2017). The green bottom line. In M. Bennett & P. James (Eds.), The green bottom line: Environmental accounting for management: Current practice and future trends (pp. 30–60). Routledge.

Bintara, R., Yadiati, W., Zarkasyi, M. W., & Tanzil, N. D. (2023). Management of GCA: A systematic literature review and research agenda. Economies, 11(2), Article e66. https://doi.org/10.3390/economies11020066

Blomé, M. W., Borell, J., Håkansson, C., & Nilsson, K. (2020). Attitudes toward elderly workers and perceptions of integrated age management practices. International Journal of Occupational Safety and Ergonomics, 26(1), 112–120. https://doi.org/10.1080/10803548.2018.1514135

Cao, C., Tong, X., Chen, Y., & Zhang, Y. (2022). How top management's environmental awareness affect corporate GCA: Evidence from China. Kybernetes, 51(3), 1250–1279. https://doi.org/10.1108/K-01-2021-0065

Caputo, F., Pizzi, S., Ligorio, L., & Leopizzi, R. (2021). Enhancing environmental information transparency through corporate social responsibility reporting regulation. Business Strategy and the Environment, 30(8), 3470–3484. https://doi.org/10.1002/bse.2814

Chang, C.-H. (2011). The influence of corporate environmental ethics on competitive advantage: The mediation role of green innovation. Journal of Business Ethics, 104(3), 361–370. https://doi.org/10.1007/s10551-011-0914-x

Chaudhry, N. I., & Amir, M. (2020). From institutional pressure to the sustainable development of firm: Role of environmental management accounting implementation and environmental proactivity. Business Strategy and the Environment, 29(8), 3542–3554. https://doi.org/10.1002/bse.2595

Chen, R., & Cao, L. (2023). How do enterprises achieve sustainable success in green manufacturing era? The impact of organizational environmental identity on green competitive advantage in China. Kybernetes, 54(1), 71–89. https://doi.org/10.1108/K-04-2022-0597

Chen, Y.-S. (2007). The positive effect of green intellectual capital on competitive advantages of firms. Journal of Business Ethics, 77(3), 271–286. https://doi.org/10.1007/s10551-006-9349-1

Chiou, T.-Y., Chan, H. K., Lettice, F., & Chung, S. H. (2011). The influence of greening the suppliers and green innovation on environmental performance and competitive advantage in Taiwan. Transportation Research Part E: Logistics and Transportation Review, 47(6), 822–836. https://doi.org/10.1016/j.tre.2011.05.016

Creswell, J. W., & Zhang, W. (2009). The application of mixed methods designs to trauma research. Journal of Traumatic Stress, 22(6), 612–621. https://doi.org/10.1002/jts.20479

Cruz, S. M., & Manata, B. (2020). Measurement of environmental concern: A review and analysis. Frontiers in Psychology, 11, Article e363. https://doi.org/10.3389/fpsyg.2020.00363

Cullen, P., Ryan, M., O'Donoghue, C., Hynes, S., & Sheridan, H. (2020). Impact of farmer self-identity and attitudes on participation in agri-environment schemes. Land Use Policy, 95, Article e104660. https://doi.org/10.1016/j.landusepol.2020.104660

D'Souza, C., Taghian, M., Lamb, P., & Peretiatkos, R. (2006). Green products and corporate strategy: An empirical investigation. Society and Business Review, 1(2), 144–157. https://doi.org/10.1108/17465680610669825

Damerji, H., & Salimi, A. (2021). Mediating effect of use perceptions on technology readiness and adoption of artificial intelligence in accounting. Accounting Education, 30(2), 107–130. https://doi.org/10.1080/09639284.2021.1872035

Debrah, J. K., Vidal, D. G., & Dinis, M. A. P. (2021). Raising awareness on solid waste management through formal education for sustainability: A developing countries evidence review. Recycling, 6(1), Article e6. https://doi.org/10.3390/recycling6010006

Dwirandra, A., & Astika, I. B. P. (2020). Impact of environmental uncertainty, trust and information technology on user behavior of accounting information systems. The Journal of Asian Finance, Economics and Business, 7(12), 1215–1224. https://doi.org/10.13106/jafeb.2020.vol7.no12.1215

Esty, D. C., & Winston, A. (2009). Green to gold: How smart companies use environmental strategy to innovate, create value, and build competitive advantage. John Wiley & Sons.

Fink, J. S. (2015). Female athletes, women's sport, and the sport media commercial complex: Have we really "come a long way, baby"? Sport Management Review, 18(3), 331–342. https://doi.org/10.1016/j.smr.2014.05.001

Gürlek, M., & Tuna, M. (2018). Reinforcing competitive advantage through green organizational culture and green innovation. The Service Industries Journal, 38(7–8), 467–491. https://doi.org/10.1080/02642069.2017.1402889

Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2–24. https://doi.org/10.1108/EBR-11-2018-0203

Hanlon, M., Yeung, K., & Zuo, L. (2022). Behavioral economics of accounting: A review of archival research on individual decision makers. Contemporary Accounting Research, 39(2), 1150–1214. https://doi.org/10.1111/1911-3846.12739

Jermsittiparsert, K., Somjai, S., & Toopgajank, S. (2020). Factors affecting firm's energy efficiency and environmental performance: The role of environmental management accounting, green innovation and environmental proactivity. International Journal of Energy Economics and Policy, 10(3), 325–331.

Kazancoglu, I., Sagnak, M., Kumar Mangla, S., & Kazancoglu, Y. (2021). Circular economy and the policy: A framework for improving the corporate environmental management in supply chains. Business Strategy and the Environment, 30(1), 590–608. https://doi.org/10.1002/bse.2641

Khan, M. H. (2023). The influence of green HRM practices and green knowledge sharing on green service behaviors: Environmental sustainability at work: How green HRM and knowledge transfer influence green service behaviors. Inverge Journal of Social Sciences, 2(2), 176–193.

Liang, Y., Lee, M. J., & Jung, J. S. (2022). Dynamic capabilities and an ESG strategy for sustainable management performance. Frontiers in Psychology, 13, Article e887776. https://doi.org/10.3389/fpsyg.2022.887776

Lin, Y.-H., & Chen, Y.-S. (2017). Determinants of GCA: The roles of green knowledge sharing, green dynamic capabilities, and green service innovation. Quality & Quantity, 51(4), 1663–1685. https://doi.org/10.1007/s11135-016-0358-6

Manners, I. (2021). Political psychology of emotion (al) norms in European Union foreign policy. Global Affairs, 7(2), 193–205. https://doi.org/10.1080/23340460.2021.1972819

Muisyo, P. K., Qin, S., Ho, T. H., & Julius, M. M. (2022). The effect of green HRM practices on GCA of manufacturing firms. Journal of Manufacturing Technology Management, 33(1), 22–40. https://doi.org/10.1108/JMTM-10-2020-0388

Munawar, S., Yousaf, H. Q., Ahmed, M., & Rehman, S. (2022). Effects of green human resource management on green innovation through green human capital, environmental knowledge, and managerial environmental concern. Journal of Hospitality and Tourism Management, 52, 141–150. https://doi.org/10.1016/j.jhtm.2022.06.009

Namazi, M., & Rezaei, G. (2024). Modelling the role of strategic planning, strategic management accounting information system, and psychological factors on the budgetary slack. Accounting Forum, 48(2), 279–306. https://doi.org/10.1080/01559982.2022.2163040

Nuryanto, U. W., Djamil, M., Sutawidjaya, A. H., & Saluy, A. B. (2020). The roles of GCA as intervention between core competence and organisational performance. International Journal of Innovation, Creativity and Change, 11(6), 394–414.

Papadas, K.-K., Avlonitis, G. J., Carrigan, M., & Piha, L. (2019). The interplay of strategic and internal green marketing orientation on competitive advantage. Journal of Business Research, 104, 632–643. https://doi.org/10.1016/j.jbusres.2018.07.009

Rehman, S. U., Giordino, D., Zhang, Q., & Alam, G. M. (2023). Twin transitions & industry 4.0: Unpacking the relationship between digital and green factors to determine GCA. Technology in Society, 73, Article e102227. https://doi.org/10.1016/j.techsoc.2023.102227

Ribeiro, O. C. de R., & Steiner, P. J. (2021). Sustainable competitive advantage and green innovation: A review of joint scale propositions. Gestão & Produção, 28(3), Article e5669. https://doi.org/10.1590/1806-9649-2021v28e5669

Riva, F., Magrizos, S., & Rubel, M. R. B. (2021). Investigating the link between managers' green knowledge and leadership style, and their firms' environmental performance: The mediation role of green creativity. Business Strategy and the Environment, 30(7), 3228–3240. https://doi.org/10.1002/bse.2799

Sabirov, O. S., Berdiyarov, B. T., Yusupov, A. S., Absalamov, A. T., & Berdibekov, A. I. U. (2021). Improving ways to increase the attitude of the investment environment. Revista Geintec-Gestao Inovacao E Tecnologias, 11(2), 1961–1975.

Saputra, K. A. K., Subroto, B., Rahman, A. F., & Saraswati, E. (2023). Mediation role of EMA on the effect of GCA on sustainable performance. Journal of Sustainability Science and Management, 18(2), 103–115. https://doi.org/10.46754/jssm.2023.02.008

Scarpellini, S., Marín-Vinuesa, L. M., Aranda-Usón, A., & Portillo-Tarragona, P. (2020). Dynamic capabilities and environmental accounting for the circular economy in businesses. Sustainability Accounting, Management and Policy Journal, 11(7), 1129–1158. https://doi.org/10.1108/SAMPJ-04-2019-0150

Setyaningrum, R. P., Kholid, M. N., & Susilo, P. (2023). Sustainable SMEs performance and GCA: The role of green creativity, business independence and green IT empowerment. Sustainability, 15(15), Article e12096. https://doi.org/10.3390/su151512096

Shahab, Y., Ntim, C. G., Chen, Y., Ullah, F., Li, H., & Ye, Z. (2020). Chief executive officer attributes, sustainable performance, environmental performance, and environmental reporting: New insights from upper echelons perspective. Business Strategy and the Environment, 29(1), 1–16. https://doi.org/10.1002/bse.2345

Song, W., Yu, H., & Xu, H. (2021). Effects of green human resource management and managerial environmental concern on green innovation. European Journal of Innovation Management, 24(3), 951–967. https://doi.org/10.1108/EJIM-11-2019-0315

Tan, Y., & Zhu, Z. (2022). The effect of ESG rating events on corporate green innovation in China: The mediating role of financial constraints and managers' environmental awareness. Technology in Society, 68, Article e101906. https://doi.org/10.1016/j.techsoc.2022.101906

Taqi, M., Rusydiana, A. S., Kustiningsih, N., & Firmansyah, I. (2021). Environmental accounting: A scientometric using biblioshiny. International Journal of Energy Economics and Policy, 11(3), 369–380.

Tian, Y. (2022, March 25–27). A literature review on upper echelons theory [Paper presentation]. Proceedings of 2nd International Conference on Enterprise Management and Economic Development, Dalian, China.

Waqas, M., Honggang, X., Ahmad, N., Khan, S. A. R., & Iqbal, M. (2021). Big data analytics as a roadmap towards green innovation, competitive advantage and environmental performance. Journal of Cleaner Production, 323, Article e128998. https://doi.org/10.1016/j.jclepro.2021.128998

Zameer, H., Wang, Y., & Yasmeen, H. (2020). Reinforcing green competitive advantage through green production, creativity and green brand image: Implications for cleaner production in China. Journal of Cleaner Production, 247, Article e119119. https://doi.org/10.1016/j.jclepro.2019.119119

Zameer, H., Wang, Y., Vasbieva, D. G., & Abbas, Q. (2021). Exploring a pathway to carbon neutrality via reinforcing environmental performance through green process innovation, environmental orientation and GCA. Journal of Environmental Management, 296, Article e113383. https://doi.org/10.1016/j.jenvman.2021.113383