Role of Managerial Innovation Behavior for moderating the effect of the Dynamic Innovation Capability on Banking Performance: Evidence from Pakistan

Zahid Bashir1* , Maryam Ashraf2, Hina Arif3

1Department of Commerce, University of Gujrat, Pakistan

2University of East London, England

3University of Sindh, Jamshoro, Pakistan

ABSTRACT

The current study attempts to address the role of dynamic innovation capabilities, along with innovative work behavior of managerial employees, to explain banking performance in Pakistan. Furthermore, it also examines the moderating role of innovative work behavior. For testing the set of proposed hypotheses, the data was collected from 413 participants working at managerial positions in different banks across Pakistan. The study employed Structural Equation Modeling (SEM) to achieve the research objectives. The results revealed internal and external reliability and validity along with a statically fit model. It was found that innovation capabilities, especially organizational innovation and process innovation, along with managerial innovation behavior have a strong optimistic effect on banks’ performance in Pakistan. Furthermore, innovative work performance strongly moderates the impact of dynamic innovation capabilities on banking performance in Pakistan. The study has managerial and practical implications for policymakers, leaders, higher management, and decision-makers in the banking sector of Pakistan. Furthermore, limitations and suggestions for future research are also incorporated.

1. INTRODUCTION

Several studies around the world cite innovation in processes and products, new markets, and organizational structures as the most critical element in performance improvement across industries. Among the first to investigate the different dimensions of innovation, viz-a-viz organizational performance, were Damanpour and Gopalakrishnan (1998). They stated that innovation fosters a new element in an industry. This novelty, either in product or process, enhances overall performance. Indeed, studies have established that government agencies also make innovations through the adoption of new technologies while responding to environmental changes and the needs of consumers to satisfy them further (Lyytinen & Rose, 2003; Peltier et al., 2012).

Business performance has tactical, operational, financial, regulatory, and organizational development dimensions. Innovation becomes significant in creating uniqueness of products and adding value to organizational growth, especially in facing challenges from new competitors (Tülüce & Yurtkur, 2015). Banking executives, when aware of the innovation requirement based on shifting market risks, use organizational capabilities to innovate and boost performance (Rajapathirana & Hui, 2018). Business performance refers to the degree to which an organization fulfills its objectives or aims (Garg, 2019). Dynamic efficiency and organizational gain have been discussed in relation to each other by different scholars. Furthermore, efficiency refers to how productively a firm operates in pursuit of its aims or targets (Mayer, 2021). Hence, innovation is critical to new organizational models, shaping improved operations and enhancing innovation capability.

Innovation is the prime driving force behind all institutional performance, including the banking sector, which is changing rapidly (Rajapathirana & Hui, 2018). Modern banking services related to innovative approaches and market, organizational processes, and product innovations have been recognized in the Pakistani banking sector (Imran et al., 2022). The innovations give a colossal boost to banks regarding better performance, whereas failure to adapt these innovations makes banks non-competitive. This research tries to sift through the market and innovation-based performances of Pakistan's banks in light of dynamic capabilities across these dimensions. Socioeconomic descriptions of banking institution employees, such as job experience, education, and employment position, are also examined to investigate the moderating effect on the innovation-performance relationship.

Research Objectives

The research seeks to examine the role of dynamic innovation capabilities along with innovative work behavior of managerial employees in explaining the banking performance in Pakistan. Additionally, it investigates innovative work behavior as the moderating variable between dynamic innovation capabilities and banking performance. The specific objectives of the study are as follows:

- To study the role of dynamic innovation capabilities in explaining the banking performance in Pakistan.

- To determine the impact of innovative work behavior of managerial employees in determining the banking performance in Pakistan.

- To explore the moderation impact of innovative work behavior of banking managerial employees between the dynamic innovation capabilities and banking performance in Pakistan.

- To draw the practical and managerial implications for the policymakers of the banking sector in Pakistan based on the outcomes of this study.

Research Significance

These days, businesses face complex consumer needs and global market pressures. Innovation in modern firms is primarily required in processes, products, markets, and organizational configurations to compete. Innovation driven by consumer expectations and executive goals help the businesses adapt better (Bocken & Konietzko, 2022). It is the key to high competition, changing markets, and a shortage of resources, with a reaction to the call from society for sustainability. According to Chaudhuri et al. (2024), innovation while having a positive influence on performance can only be successful if there is enough organizational support. While product and process innovations are significant in alignment and improvement of business operations, marketing and organizational innovations are at the core of performance enrichment and are often overlooked in the banking sector (Chatterjee et al., 2024).

Novelty and Research Gap

Innovation around multiple dimensions has been researched considerably worldwide but leaves major lacuna, particularly in research focused on the Pakistani banking sector. Most of the past studies consider only a few aspects of innovation, not looking into the overall impact of market, organizational, product, and process innovations on performance. This study aims to address this knowledge gap in a rather distinctive way by integrating the dimensions of innovation within the Pakistani banking sector, marked by its rapid adoption of innovative practices amidst a rather dynamic economic environment. The novelty provided by the study on the way these multidimensional innovations interact with banking performance has filled an important gap in the literature and provided major insights into theory and practice in emerging markets.

Literature for Innovation and Performance

Rasool et al. (2019) found that both process and product innovation positively influence organizational performance. Similarly, Wang and Hu (2020) did the same when they realized improved performance was derived through innovative supply chains. It was also noted that organizational innovation acted as a mediating factor towards the relationship of human resource practices to bank performance (Imran et al., 2022; Iqbal et al., 2021). Similarly, Tarí et al. (2023) found that process innovation enhances the performance, while product innovation reinforces financial performance. More recent studies using PLS-SEM reported weak mediation and moderation of organizational innovation (Hashem & Aboelmaged, 2024; Maqdliyan & Setiawan, 2023). Therefore, the study aims to test the following hypothesis:

H1: The dynamic innovation capability has a strong and positive role in explaining the Banking Performance in Pakistan.

Theoretical Underpinnings and Hypothesis Development

Organizational Innovation

Service innovation strengthens market orientation and financial performance of industries whereas organizational learning on account of dynamic changes also gives a high positive impact on firm performance. Garousi et al. (2020) demonstrated that using resources for innovation contributes more to performance than merely reinforcing existing collaborations. Technological and operational innovation facilitate the performance of SMEs in increasing success across foreign markets and enhancing their overall performance (Jalil et al., 2021). Organizational innovation is often more critical than technological innovation in SMEs. Modern research studies support the strong and optimistic impact of organizational innovation on banking performance (Sánchez-Hernández et al., 2023; Tripathi & Dhir, 2024). Therefore, the study aims to test the following hypothesis:

H2: There is a strong and optimistic link of Organizational Innovation with the Banking Performance in Pakistan.

Product Innovation

Wang et al. (2021) reached a conclusion that product innovation positively influences the business aspect. They also stated that customers' confidence in product innovation can lead to an increase in market value. Similarly, both basic and advanced product development enhance the performance of a company by providing competitive edge advantages (Farida & Setiawan, 2022). In addition, a number of research studies in emerging economies also support the positive influence of product innovation on performance (Adomako et al., 2024; Larios-Francia & Ferasso, 2023). Therefore, the following hypothesis is proposed for testing:

H3: The Product Innovation significantly accelerates the Banking Performance in Pakistan.

Process Innovation

Medda (2020) proved that process innovation enhances the market performance of manufacturing companies. Also, De Giovanni and Cariola (2021) identified a positive influence of process innovation in supply industries. Furthermore, Zamani et al. (2022) explored the relationship between predictive and prescriptive innovation in both product and process innovation for SMEs. Modern research also found a strong link between process innovation and performance (Chatterjee et al., 2024; Larios-Francia & Ferasso, 2023). Therefore, the study aims to test the following hypothesis:

H4: Process Innovation significantly improves Banking Performance in Pakistan.

Market Innovation

Peñalba-Aguirrezabalaga et al. (2022) reported that performance in service organizations relies more on marketing innovation than on product innovation. Based on the evidence from branchless banking, Ashiru et al. (2023) report that the market innovation significantly enhances banks' market share. Furthermore, a number of latest researches have concluded that market innovation positively impacts performance (Ayinaddis, 2023; Chang et al., 2024). Therefore, this study aims to test the following hypothesis:

H5: The Market Innovation strongly enhances the Banking Performance in Pakistan.

Managerial Innovation Behavior and Organizational Performance

Managerial innovative behavior refers to the ability of managers to develop new products, technologies, and work methods, as well as to adopt and implement them. According to Asurakkody and Shin (2018), four important dimensions of innovative behavior include exploration, the generation, promotion, and implementation of ideas. Managerial innovative behavior has been found to relate to organizational performance (Berdecia-Cruz et al., 2022; Kör et al., 2021). Furthermore, there is strong evidence of a positive relationship between innovative work behavior and banking performance (Shahbaz et al., 2024; Suhandiah et al., 2023). Therefore, the following hypotheses are required to test for this study:

H6: The Innovative Work Behavior of the bank employees has a positive and strong influence on determining the Banking Performance in Pakistan.

H7: The Innovative Work Behavior significantly moderates the relationship between Dynamic Innovation Capability and the Banking Performance in Pakistan.

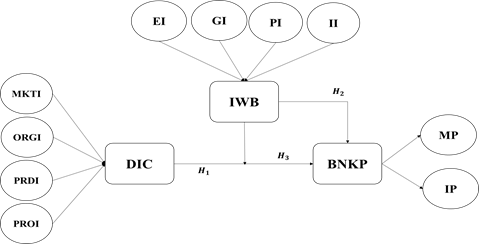

The Research Framework

The paper looks into the dynamic innovative capability-market, organizational, product, and process-performance as it affects banking institutions in Pakistan using the conditional performance-enabled-innovation framework by Ahinful et al. (2024). It emphasized the high role played in improving performance by product and process innovations.

Figure 1Research Framework

Research Methodology

Research Design

The study aims to investigate the impact of dynamic innovation capabilities on banking performance in Pakistan with the moderation role of innovative work behavior. The researchers used the quantitative method of primary data approach for data collection and analysis. The data collection was made possible with the help of a survey questionnaire from bank managers working in different branches of all the leading banks in Pakistan across the country.

Population and Sampling

The motivation for targeting banks in Pakistan is stems from the significant innovations that have emerged in both Islamic and interest-based banking over the past two decades. The focus will be on government, private, local, and foreign banks. For the sample to be consistent, only domestic scheduled banks listed in the State Bank of Pakistan have been researched, excluding foreign banks. Individual bank branches will be the unit of analysis, while the managerial employees will serve as observation unit, because employees at this level hold the authority to make important decisions and take part in innovative work behavior.

Research Instrument and Data Collection

The structured online survey questionnaire was forwarded to 900 managerial employees in different branches of public and private sector banks across the country. The survey instrument was sent via email, WhatsApp, and social media platforms such as Facebook, Instagram, and LinkedIn, taking into consideration the COVID-19 safety measures. A total of 413 fully completed questionnaires were received, thus rendering the response rate at 45.88%. This survey was based on four sub-scales, namely, personal and social characteristics included gender, age, marital status, qualification, job tenure; dynamic innovation capabilities trait included market, organizational, product, and process innovation; bank performance included market and innovative performance; innovative work behavior included idea exploration, generation, promotion, and implementation.

Variable Measurement

The study aimed to investigate the direct impact of dynamic innovation capabilities on banking performance in Pakistan. Furthermore, a moderating role of innovative work behavior of banking employees (managers) was also examined in the study. Banking performance, dynamic innovative capabilities, and innovative work behavior were used as the exogenous, endogenous, and moderating variables respectively. The measurement and scaling of the construct’s variables are explained under their specific heading, with definitions and references given in Table 1.

Endogenous Variable

Banking performance was used as the endogenous variable of the study. This variable was further measured with two sub-dimensions; market performance, and innovative performance with 6 items to measure each one. The variable was scaled using Likert five points; strongly disagree, disagree, natural, agree, and strongly agree. References for the measurement and scaling of banking performance, its dimensions, and their ultimate items are reported in table 1.

Exogenous Variables

Dynamic innovation capability is used as the exogenous variable of the study. This variable further measured with four sub-dimensions: market innovation, organizational innovation, production innovation, and process innovation with five items to measure each one. The variable was scaled using Likert five points; strongly disagree, disagree, natural, agree, and strongly agree. The references for the measurement and scaling of banking performance, its dimensions, and their ultimate items are also reported in table 1.

Moderating Variable

Innovative work behavior was used as the moderating variable of the study. This variable was measured through its four sub-dimensions: exploration of an idea, generation of an idea, promotion of the idea, and implementation of an idea with four items to measure each one. The variable was scaled using Likert five points; strongly disagree, disagree, natural, agree, and strongly agree. The references for the measurement and scaling of banking performance, its dimensions, and their ultimate items are provided in table 1 below.

Table 1Operational Depiction of Constructs| Construct | Description/Definition | Referred by |

|---|---|---|

| Dynamic Innovation Capabilities (DIC) | Marketing innovation refers to a company's capacity to market items based on such an awareness of customer needs, competitiveness, expenses, including advantages, and invention adoption. |

(Hashem & Aboelmaged, 2024; Maqdliyan & Setiawan, 2023) |

It is the creation of a new organizational approach for business administration. It is not just an administrative process but also involves the development of exterior relationships between a business and third parties. |

(Sánchez-Hernández et al., 2023; Tripathi & Dhir, 2024) | |

The invention as well as the eventual launch of the new or upgraded version of previously existing goods is considered product innovation. |

(Adomako et al., 2024; Larios-Francia & Ferasso, 2023td> | |

It is the introduction of a new or considerably improved production and distribution method. Major improvements in methodology, technology, and/or programs are part of it. |

(Chatterjee et al., 2024; Larios-Francia & Ferasso, 2023) | |

| Managerial Innovative Behavior (IWB) | New approaches to upgrade existing products and services are sought at this phase. It includes actions such as developing company processes and improving product/process options. |

(Shahbaz et al., 2024; Suhandiah et al., 2023) |

Associated with developing innovative products, services, or processes and resolving corporate challenges through information gathering and productivity improvement. |

(Shahbaz et al., 2024; Suhandiah et al., 2023) | |

Methods to increase accessibility, affordability, or quality of goods/services. Examples include promotions or price reductions to attract customers. |

(Shahbaz et al., 2024; Suhandiah et al., 2023) | |

Turning innovative ideas into action. If not applied, the ideas lack value. Their implementation reflects their usefulness. |

(Shahbaz et al., 2024; Suhandiah et al., 2023) | |

| Bank Performance (BNKP) | Indicators include operating income, market dominance, profitability, competitive edge, customer loyalty, and commitment. |

(YuSheng & Ibrahim, 2020) |

Application of creativity and innovation to enhance products, procedures, and methods in terms of relevance, utility, and efficiency. |

(YuSheng & Ibrahim, 2020) |

Method of Estimation

This study uses SEM with Smart PLS because it models complex relationships among multiple variables and tests such hypotheses that incorporate latent constructs precisely. Besides, SEM was preferred in view of it being more robust than the other methods that simultaneously assess direct and indirect effects, take care of measurement errors, and validate theoretical models precisely. The analysis includes the estimation and reporting of the personal and socio-economic characteristics of participants using SPSS. Additionally, the remaining analysis includes the estimation and reporting of an outer model, outer loadings, outer VIF, convergent validity & reliability, discriminant validity & reliability, affect size, and R-square along with model fit indices, and finally the inner model, and structural model estimation for hypothesis testing.

Data Analysis and Discussion

This research studies the direct impact of dynamic innovative capabilities and innovative work behavior on banking performance in Pakistan. Moreover, innovative work behavior moderates such a relationship. In the present research, the quantitative approach will be applied, in which 900 online surveys will be forwarded to managerial employees across all scheduled bank branches; in total, responses received were 413 completions (45.88%). The method used for testing the hypotheses is structural equation modeling; SPSS was used to summarize the personal and socio-economic characteristics, and Smart PLS for estimating the SEM model together with the validity and reliability of measurements.

Participants’ Summary

Table 2 provides an overview of the personal and socio-economic characteristics of the participants using SPSS. The variables included gender, age, marital status, education, and job tenure. The highest number of participants were male, falling in the age group of 31-35 years, married, having up to 16 years of education, and experience in the banking industry ranging from 6-10 years. The percentages for these characteristics were 81%, 43%, 46.85%, 54%, and 54.5%, respectively. The Pakistani banking sector seems to be dominated by males, middle-aged, married managers who hold a graduate degree and have fairly extensive experience, having been accustomed to innovation and performance.

Table 2Personal & Socio-Economic Features Summary|

Features |

Categories |

N |

% |

|---|---|---|---|

|

Gender |

Male |

335 |

81 |

|

Female |

78 |

19 |

|

|

Age (Years) |

< 24 |

17 |

4 |

|

25 – 30 |

128 |

31 |

|

|

31-35 |

178 |

43 |

|

|

36-40 |

50 |

12 |

|

|

> 40 |

41 |

10 |

|

|

Marital Status |

Unmarried |

137 |

33.15 |

|

Married |

194 |

46.85 |

|

|

Divorced/Separated |

83 |

20 |

|

|

Qualification |

14 or Less years |

112 |

27 |

|

16 years |

223 |

54 |

|

|

18 or more years |

78 |

19 |

|

|

Job Tenure (Years) |

< 1 |

10 |

2.5 |

|

1-5 |

95 |

23 |

|

|

6-10 |

225 |

54.5 |

|

|

> 10 |

83 |

20 |

The hypothesis of the study was tested using the structural equation modeling (SEM) approach with a two-step procedure as the method of estimation (Henseler et al., 2015). The SEM approach requires measuring the outer model, also called the measurement model along with convergent validity & reliability, discriminant validity & reliability, and model fitness indices as the first step (Hair et al., 2020). The second step involves estimating the inner model based on bootstrapping procedure with SEM estimations of direct, and moderation impact of the study (Hair et al., 2020).

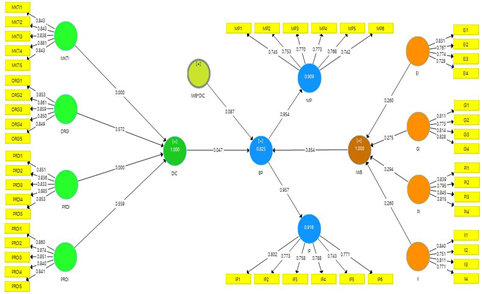

Figure 2Outer/Measurement Model

Outer Model Assessment

Figure 2: Smart PLS-estimated outer model that links constructs to their respective indicators. The outer loading value for each indicator should be higher than 0.70 to establish validity with regard to each factor. First-order reflective constructs for market, organizational, product and process innovation-MKT, ORG, PRD, PRO-respectively-and dynamic innovation capability DIC as a second-order formative construct. Besides, innovative work behavior (IWB) and banking performance (BNKP) are assessed as second-order constructs. The path coefficient between DIC and banking performance is 0.047; IWB and banking performance, 0.854; and the moderating effect of DIC*IWB on banking performance, 0.087. The coefficient of determination for banking performance is 0.825, depicting that 83% variance in banking performance is explained by variation in DIC, IWB, and their interactions.

Outer loadings and VIF Values

Items/factors loadings and variance inflation factor measured internal consistency of the outer model. A loading is reliable if it is higher than 0.70, and all factors have higher loading than 0.70 at the first and second-order levels. VIF values to establish that there is no multicollinearity problem since they should always be less than 5, showed no problem of multicollinearity for the constructs.

Table 3Internal Consistency| Construct & Dimension | Item | Factor Loading (First Order) |

VIF Value (First Order) |

Factor Loading (Second Order) |

VIF Value (Second Order) |

|---|---|---|---|---|---|

| Market Innovation (MKTI) | MKTI1 | 0.843 | 2.421 | 0.743 | 2.001 |

| MKTI2 | 0.843 | 2.401 | 0.745 | 1.995 | |

| MKTI3 | 0.838 | 2.268 | 0.709 | 1.825 | |

| MKTI4 | 0.881 | 2.494 | 0.771 | 2.051 | |

| MKTI5 | 0.843 | 2.385 | 0.747 | 1.975 | |

| Organizational Innovation (ORGI) | ORGI1 | 0.853 | 2.498 | 0.767 | 2.401 |

| ORGI2 | 0.861 | 2.591 | 0.768 | 2.509 | |

| ORGI3 | 0.859 | 2.576 | 0.750 | 2.501 | |

| ORGI4 | 0.850 | 2.517 | 0.751 | 2.409 | |

| ORGI5 | 0.849 | 2.436 | 0.753 | 2.381 | |

| Product Innovation (PRDI) | PRDI1 | 0.851 | 2.383 | 0.746 | 1.989 |

| PRDI2 | 0.836 | 2.628 | 0.721 | 2.195 | |

| PRDI3 | 0.833 | 2.521 | 0.719 | 2.018 | |

| PRDI4 | 0.885 | 2.452 | 0.783 | 1.967 | |

| PRDI5 | 0.853 | 2.549 | 0.739 | 2.176 | |

| Process Innovation (PROI) | PROI1 | 0.860 | 2.571 | 0.753 | 2.536 |

| PROI2 | 0.874 | 2.867 | 0.775 | 2.756 | |

| PROI3 | 0.851 | 2.535 | 0.738 | 2.426 | |

| PROI4 | 0.840 | 2.362 | 0.735 | 2.322 | |

| PROI5 | 0.841 | 2.407 | 0.758 | 2.284 | |

| Exploration of Idea (EI) | EI1 | 0.831 | 2.291 | 0.776 | 1.798 |

| EI2 | 0.767 | 1.721 | 0.714 | 1.521 | |

| EI3 | 0.774 | 2.072 | 0.723 | 1.598 | |

| EI4 | 0.728 | 1.997 | 0.698 | 1.405 | |

Convergent Validity & Reliability

Convergent validity and reliability test the separation of indicators of a construct from those of other constructs. In this study, convergent validity was tested at first and second order through Cronbach's Alpha via composite reliability and average variance extracted via Smart PLS. A 0.70 for both Cronbach's Alpha and composite reliability, and 0.50 for AVE, are the minimum levels required. As shown in Table 4.3, all constructs exceed the threshold level in terms of the above-mentioned requirements, which confirms the convergent validity of the data. The following Table 4 also shows the average and standard deviation for each construct and its dimensions.

Table 4Convergent Validity & Reliability (1st & 2nd Order)| Constructs and Dimensions | CA | CR | AVE | Mean | Std |

|---|---|---|---|---|---|

| Bank Performance (BP) | 0.921 | 0.932 | 0.535 | 5.00 | 0.22 |

| Market Performance (MP) | 0.852 | 0.891 | 0.576 | 3.97 | 0.27 |

| Innovative Performance (IP) | 0.865 | 0.899 | 0.597 | 4.02 | 0.01 |

| Dynamic Innovative Capabilities (DIC) | 0.916 | 0.930 | 0.570 | 3.91 | 0.41 |

| Market Innovation (MKTI) | 0.904 | 0.928 | 0.722 | 3.70 | 0.13 |

| Organizational Innovation (ORGI) | 0.907 | 0.931 | 0.730 | 3.71 | 0.20 |

| Production Innovation (PRDI) | 0.907 | 0.930 | 0.726 | 3.69 | 0.16 |

| Process Innovation (PROI) | 0.907 | 0.930 | 0.728 | 3.74 | 0.22 |

| Innovative Work Behavior (IWB) | 0.943 | 0.949 | 0.540 | 4.11 | 0.10 |

| Exploration of Idea (EI) | 0.779 | 0.858 | 0.602 | 4.37 | 0.23 |

| Generation of Idea (GI) | 0.821 | 0.882 | 0.651 | 4.05 | 0.02 |

| Implementation of Idea (II) | 0.804 | 0.872 | 0.631 | 3.98 | 0.34 |

| Promotion of Idea (PI) | 0.842 | 0.894 | 0.679 | 4.87 | 0.79 |

| IWB*DIC (Moderation) | 0.987 | 0.986 | 0.517 | 4.02 | 0.01 |

| BP | DIC | EI | GI | II | IP | IWB | IWB*DIC | MKTI | MP | ORGI | PI | PRDI | PROI | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| BP | 0.731 | |||||||||||||

| DIC | 0.187 | 0.755 | ||||||||||||

| EI | 0.645 | 0.120 | 0.776 | |||||||||||

| GI | 0.630 | 0.161 | 0.727 | 0.807 | ||||||||||

| II | 0.686 | 0.146 | 0.683 | 0.734 | 0.794 | |||||||||

| IP | 0.657 | 0.161 | 0.629 | 0.817 | 0.742 | 0.773 | ||||||||

| IWB | 0.603 | 0.152 | 0.728 | 0.809 | 0.706 | 0.675 | 0.735 | |||||||

| IWB*DIC | 0.481 | 0.109 | 0.424 | 0.386 | 0.431 | 0.423 | 0.449 | 0.563 | ||||||

| MKTI | 0.161 | 0.261 | 0.080 | 0.123 | 0.107 | 0.143 | 0.119 | 0.106 | 0.850 | |||||

| MP | 0.654 | 0.198 | 0.785 | 0.768 | 0.760 | 0.726 | 0.650 | 0.498 | 0.166 | 0.759 | ||||

| ORGI | 0.202 | 0.687 | 0.112 | 0.166 | 0.146 | 0.173 | 0.151 | 0.127 | 0.272 | 0.213 | 0.854 | |||

| PI | 0.652 | 0.132 | 0.706 | 0.776 | 0.717 | 0.722 | 0.629 | 0.410 | 0.125 | 0.705 | 0.130 | 0.824 | ||

| PRDI | 0.187 | 0.133 | 0.147 | 0.140 | 0.168 | 0.172 | 0.173 | 0.027 | 0.531 | 0.185 | 0.121 | 0.180 | 0.852 | |

| PROI | 0.129 | 0.681 | 0.100 | 0.118 | 0.111 | 0.110 | 0.117 | 0.065 | 0.188 | 0.137 | 0.564 | 0.103 | 0.115 | 0.853 |

| BP | DIC | EI | GI | II | IP | IWB | IWB*DIC | MKTI | MP | ORGI | PI | PRDI | PROI | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| BP | — | |||||||||||||

| DIC | 0.204 | — | ||||||||||||

| EI | 0.895 | 0.146 | — | |||||||||||

| GI | 0.852 | 0.188 | 0.831 | — | ||||||||||

| II | 0.813 | 0.170 | 0.888 | 0.802 | — | |||||||||

| IP | 0.871 | 0.180 | 0.707 | 0.868 | 0.890 | — | ||||||||

| IWB | 0.868 | 0.165 | 0.883 | 0.732 | 0.742 | 0.868 | — | |||||||

| IWB*DIC | 0.473 | 0.158 | 0.460 | 0.400 | 0.460 | 0.428 | 0.440 | — | ||||||

| MKTI | 0.173 | 0.280 | 0.093 | 0.142 | 0.123 | 0.158 | 0.127 | 0.123 | — | |||||

| MP | 0.777 | 0.224 | 0.862 | 0.814 | 0.817 | 0.861 | 0.846 | 0.510 | 0.185 | — | ||||

| ORGI | 0.221 | 0.870 | 0.136 | 0.195 | 0.171 | 0.196 | 0.165 | 0.152 | 0.295 | 0.242 | — | |||

| PI | 0.867 | 0.149 | 0.894 | 0.831 | 0.892 | 0.863 | 0.740 | 0.423 | 0.140 | 0.850 | 0.148 | — | ||

| PRDI | 0.199 | 0.141 | 0.166 | 0.160 | 0.196 | 0.190 | 0.183 | 0.081 | 0.584 | 0.204 | 0.128 | 0.202 | — | |

| PROI | 0.142 | 0.870 | 0.123 | 0.140 | 0.130 | 0.125 | 0.129 | 0.130 | 0.203 | 0.156 | 0.621 | 0.117 | 0.122 | — |

Discriminant Validity & Reliability

Discriminant validity or external validity implies the degree to which different constructs vary from each other. This study checked for discriminant validity through the Fornell-Larcker criterion and the HTMT ratio, because this set of measures has attained widespread acceptance. A discriminant validity is confirmed if the square root of AVE for each of the constructs is greater than the composite correlation scores of the other constructs. Table 5: Discriminant Validity Confirmed as the Values of √AVE are Greater than Composite Correlation Scores.

According to Hamid et al. (2017), the recommended value of HTMT ratio is 0.90 or less. Similarly, Henseler et al. (2015) also recommended an HTMT ratio with the value of 0.85 or less for establishing the discriminant validity. Therefore, the table 6 confirmed the discriminant validity as per the criteria of 0.85 as well as 0.90 or lesser for all the computed constructs.

Model Fitness

SRMR is a goodness-of-fit measure where the cutoff value of < 0.08 defines the fitness of the model. Furthermore, NFI ought to be more than 0.90 and RMS Theta below 0.12 for the model to be statistically fit. From Table 7, the model has satisfied the statistical fit by having an SRMR less than 0.08, NFI more than 0.90, and RMS Theta less than 0.12.

Table 7 Indices for Model FitEffect Size, Predictive Relevance, and Coefficients of Determination

Table 8 reports F2, Q2, and R2. F2 denotes the effect size. The following thresholds have been suggested for F2: < 0.02 = "no effect, 0.02-0.15 = "small effect, 0.15-0.35 = "medium effect, and > 0.35 = "large effect. According to the study, the effects of dynamic innovation capability and innovative work behavior are large, but the moderating variable IWB*DIC has a small effect. Q2 is predictive relevance, and as long as values are greater than 0, this indicates the model has predictive relevance. According to Table 8, Q2 in each and every construct is greater than 0, hence a confirmation of predictive relevance determination. R2 measures the model fit where values that approximate 1 denote good fit. This is confirmed on Table 8 with R2 value for each and every construct almost close to one, therefore making the model well fitted.

Table 8 F2, Q2, and R2|

Constructs |

F2 (Effect Size) |

Q2 Predictive Relevance |

R2 Coefficient of Determination |

||||

|---|---|---|---|---|---|---|---|

|

Dimensions of DI & IWB |

BNKP |

||||||

|

MKTI |

ORGI |

PRDI |

PROI |

||||

|

Dynamic Innovation Capabilities |

0.001 |

0.631 |

0.001 |

.578 |

0.349 |

0.565 |

1.000 |

|

Innovative Performance |

- |

- |

- |

- |

0.474 |

0.542 |

0.916 |

|

Market Performance |

- |

- |

- |

- |

0.410 |

0.519 |

0.909 |

|

|

EI |

GI |

PI |

II |

|

|

|

|

Innovative Work Behavior |

0.204 |

0.158 |

0.89 |

0.93 |

0.375 |

0.534 |

1.000 |

|

Moderating (IWB*DIC) |

- |

- |

- |

- |

0.039 |

|

|

|

Bank’s Performance |

- |

- |

- |

- |

|

0.437 |

0.825 |

Inner Model Assessment

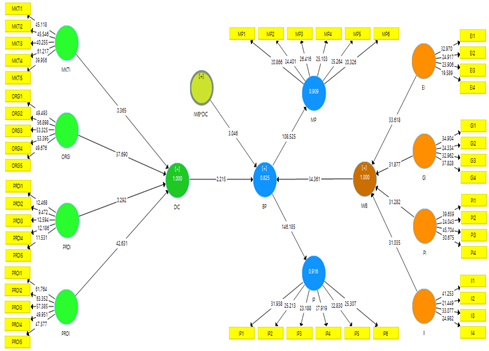

In Smart PLS, bootstrapping is resorted to in assessing the inner/ structural model that shows the relationship between constructs. The inner model is presented on Figure 3 and tables 9 to 11, which show the hypothesis testing results. This shows that the paths between constructs are statistically significant based on their t-values. A t-value > 1.96 signifies significance. Precisely, this study finds strong effects for dynamic innovative capability and innovative work behavior on banking performance, as well as a very strong impact for the moderating variable of IWB * DIC, all at t-values > 1.96.

Hypothesis Testing Using SEM

Table 9: Structural equation model results of the first hypothesis that dynamic innovation capability develops a positive and statistically significant influential effect on innovative performance and market performance in Pakistan banking performance, accordingly. The findings therefore confirm the hypothesis as well as support findings in scholarly literature. Moreover, innovations in organization and processes gave significant contributions to performance, whereas product and marketing innovations did not provide enough evidence to affect the performance in banking.

Table 9 Testing 1st Hypothesis using SEM| Relationships | (O) | STD | t-Values | p Values | Hypothesis | Decision |

|---|---|---|---|---|---|---|

| DIC → BP | 0.047 | 0.021 | 2.215 | 0.027 | H₁ | Supported the First Hypothesis |

| DIC → IP | 0.045 | 0.021 | 2.215 | 0.027 | - | Supported the First Hypothesis |

| DIC → MP | 0.045 | 0.020 | 2.215 | 0.027 | - | Supported the First Hypothesis |

| ORGI → BP | 0.027 | 0.012 | 2.200 | 0.028 | H₁a | Supported the 1st dimension of First Hypothesis |

| ORGI → IP | 0.026 | 0.012 | 2.200 | 0.028 | - | Supported the 1st dimension of First Hypothesis |

| ORGI → MP | 0.026 | 0.012 | 2.200 | 0.028 | - | Supported the 1st dimension of First Hypothesis |

| PRDI → BP | 0.000 | 0.000 | 0.248 | 0.804 | H₁b | Not Supported the 2nd dimension of First Hypothesis |

| PRDI → IP | 0.000 | 0.000 | 0.248 | 0.804 | - | Not Supported the 2nd dimension of First Hypothesis |

| PRDI → MP | 0.000 | 0.000 | 0.249 | 0.804 | - | Not Supported the 2nd dimension of First Hypothesis |

| PROI → BP | 0.027 | 0.012 | 2.232 | 0.026 | H₁c | Supported the 3rd dimension of First Hypothesis |

| PROI → IP | 0.025 | 0.011 | 2.233 | 0.026 | - | Supported the 3rd dimension of First Hypothesis |

| PROI → MP | 0.025 | 0.011 | 2.233 | 0.026 | - | Supported the 3rd dimension of First Hypothesis |

| MKTI → BP | 0.000 | 0.000 | 0.290 | 0.772 | H₁d | Not Supported the 4th dimension of First Hypothesis |

| MKTI → IP | 0.000 | 0.000 | 0.289 | 0.772 | - | Not Supported the 4th dimension of First Hypothesis |

| MKTI → MP | 0.000 | 0.000 | 0.290 | 0.772 | - | Not Supported the 4th dimension of First Hypothesis |

Table 10 shows that the innovative work behavior of managerial employees significantly influences banking performance regarding innovation and marketing performance in Pakistan. The results of SEM verified the second hypothesis, which stated that all four dimensions-exploration, generation, promotion, and implementation-of innovative work behavior positively influence performance. The findings therefore confirm the hypothesis as well as support findings in scholarly literature.

Table 10 Testing the 2nd Hypothesis Using SEM| Relationships | (O) | STD | t values | p Values | Hypothesis | Decision |

|---|---|---|---|---|---|---|

| IWB → BP | 0.854 | 0.025 | 34.361 | 0.000 | H₂ | Supported the second hypothesis |

| IWB → IP | 0.818 | 0.026 | 31.230 | 0.000 | - | Supported the second hypothesis |

| IWB → MP | 0.814 | 0.026 | 30.809 | 0.000 | - | Supported the second hypothesis |

| EI → BP | 0.222 | 0.008 | 26.246 | 0.000 | H₂a | Supported 1st dimension of second hypothesis |

| EI → IP | 0.212 | 0.009 | 24.943 | 0.000 | - | Supported 1st dimension of second hypothesis |

| EI → MP | 0.212 | 0.008 | 24.954 | 0.000 | - | Supported 1st dimension of second hypothesis |

| GI → BP | 0.235 | 0.009 | 26.273 | 0.000 | H₂b | Supported 2nd dimension of second hypothesis |

| GI → IP | 0.225 | 0.009 | 25.360 | 0.000 | - | Supported 2nd dimension of second hypothesis |

| GI → MP | 0.224 | 0.009 | 25.180 | 0.000 | - | Supported 2nd dimension of second hypothesis |

| PI → BP | 0.251 | 0.009 | 28.483 | 0.000 | H₂c | Supported 3rd dimension of second hypothesis |

| PI → IP | 0.241 | 0.009 | 28.108 | 0.000 | - | Supported 3rd dimension of second hypothesis |

| PI → MP | 0.240 | 0.009 | 27.639 | 0.000 | - | Supported 3rd dimension of second hypothesis |

| II → BP | 0.222 | 0.010 | 23.124 | 0.000 | H₂d | Supported 4th dimension of second hypothesis |

| II → IP | 0.212 | 0.009 | 22.617 | 0.000 | - | Supported 4th dimension of second hypothesis |

| II → MP | 0.212 | 0.009 | 22.606 | 0.000 | - | Supported 4th dimension of second hypothesis |

By referring to Table 11, it is observed that the moderating variable is found significantly influencing and enhancing banking performance in Pakistan. The confirmation of hypothesis three leads towards indicating that the combination of dynamic innovation capability with innovative work behavior enhances performance related to innovation and market.

Table 11 Testing the 3rd Hypothesis (Moderating impact) Using SEM| Relations | (O) | STD | t values | p Values | Hypothesis | Decision |

|---|---|---|---|---|---|---|

| IWB × DIC → BP | 0.087 | 0.029 | 3.046 | 0.002 | H₃ | Accepted & supported |

| IWB × DIC → IP | 0.083 | 0.027 | 3.058 | 0.002 | H₃ | Accepted & supported |

| IWB × DIC → MP | 0.083 | 0.027 | 3.058 | 0.002 | H₃ | Accepted & supported |

The findings inferred that managerial employees’ working behavior towards innovation along with all its sub-dimension has the biggest potential effect in determining the banking performance in Pakistan. Additionally, the dynamic innovation capability has a strong impact in determining banking performance. However, a careful analysis required the sub-capabilities of innovation like production and marketing to accelerate their potential effect on banking performance in Pakistan. The blend of innovative working behavior of managerial employees along with organizational and process innovation capabilities has a potential effect for boosting the banking performance in Pakistan.

Conclusion

This study explores how dynamic innovation capability and innovative work behavior affect the performance of banking institutions in Pakistan, highlighting how the latter can act as an agent of moderation. Quantitative data collection was done through an email and social media questionnaire to bank managers in Pakistan; 900 in all. This resulted in 413 usable responses due to the restriction on pandemic-related face-to-face interactions, accounting for a response rate of 45.88%. Structural equation modeling was used to test the hypotheses, and accordingly, data analysis involved SPSS for personal features and Smart PLS for convergent and discriminant and structural validity.

The results show that the majority of managers in the banking sector in Pakistan are male, middle-aged, married, and graduate qualifiers with over five years of experience. Additionally, managers have also been found to be highly knowledgeable in processes, policies, and development of performance targets for innovations. The assessment of the outer model confirmed internal consistency-factor loadings > 0.70 without multicollinearity indicated by VIF values. The convergent validities were established for all the constructs by meeting the Fornell-Larcker and HTMT ratio criteria. The fact that the model fit indices had SRMR < 0.08, NFI > 0.90, and RMS Theta < 0.12 was confirmation of the statistical fit of the model. Dynamic innovation capabilities and innovative work behavior had large effect sizes, while the moderating variable had a small effect size. Q2 values greater than 0 indicated predictive relevance, and a good model fit was depicted by R2 values close to one. Through hypothesis testing, dynamic innovation capability and innovative work behavior were found to positively affect banking performance, while product and market innovations were the lesser drivers.

Overall, the results indicate that innovative work behavior of managerial employees and dynamic innovation capabilities significantly influence banking performance in Pakistan. However, for product and marketing innovations, there is a need to focus on more sub-capabilities to further develop their influence. Banking performance may be further influenced by the combination of innovative work behavior with organizational and process innovations.

Managerial and Practical Implications

The present study recommends some managerial and practical implications for the policymakers, higher management, and leaders in Pakistani banks. These implications include the implementation of organizational and process innovation as the innovative capabilities in the banking sector of Pakistan for boosting their performance. The decision-makers in the banking sector of Pakistan need to revise their core innovation policies regarding innovative products and innovation in the marketing process. Additionally, managerial working employees are directly involved in creating the innovative process, therefore, their innovative working behavior has the potential effect for accelerating process and organizational innovation for an ultimate increase of banking performance in Pakistan.

Limitations and Research Recommendations for the Future

The study comprises of a number of limitations, e.g., the sampling approach as being convenient for online data collection due to the COVID situation around the world. However, future research may consider the random sampling approach once the pandemic restrictions have eased. The study focused solely on the banking sector of Pakistan. The future research may consider the banking sector of other countries/ cross-culture studies, or at least a comparison between conventional and Islamic banks based on present research. Additionally, future research may also consider other sectors/industries for examining the impact of innovation capabilities and firm’s performance along with innovative work behavior of employees as the moderating variable.

CONFLICT OF INTEREST

The author of the manuscript has no financial or non-financial conflict of interest in the subject matter or materials discussed in this manuscript

DATA AVAILABILITY STATEMENT

The data associated with this study will be provided by the corresponding author upon request.

FUNDING DETAILS

No funding has been received for this research.

REFERENCES

- Adomako, S., Gyensare, M. A., Amankwah-Amoah, J., Akhtar, P., & Hussain, N. (2024). Tackling grand societal challenges: Understanding when and how reverse engineering fosters frugal product innovation in an emerging market. Journal of Product Innovation Management, 41(2), 211–235. https://doi.org/10.1111/jpim.12678

- Ahinful, A. A., Mensah, A. O., Koomson, S., Nyarko, F. K., & Nkrumah, E. (2024). A conceptual framework of total quality management on innovation performance in the banking sector. The TQM Journal, 36(4), 1193–1211. https://doi.org/10.1108/TQM-11-2022-0334

- Ashiru, O., Balogun, G., & Paseda, O. (2023). Financial innovation and bank financial performance: Evidence from Nigerian deposit money banks. Research in Globalization, 6, Article e100120. https://doi.org/10.1016/j.resglo.2023.100120

- Asurakkody, T. A., & Shin, S. Y. (2018). Innovative behavior in nursing context: A concept analysis. Asian Nursing Research, 12(4), 237–244. https://doi.org/10.1016/j.anr.2018.11.003

- Ayinaddis, S. G. (2023). The effect of innovation orientation on firm performance: evidence from micro and small manufacturing firms in selected towns of Awi Zone, Ethiopia. Journal of Innovation and Entrepreneurship, 12(1), Article e26. https://doi.org/10.1186/s13731-023-00290-3

- Berdecia-Cruz, Z., Flecha, J. A., & Ortiz, M. (2022). The gender differences in innovative mentality, leadership styles and organizational innovative behavior: the case the "40 Under 40" and their impact on organizational success. European Business Review, 34(3), 411–430. https://doi.org/10.1108/EBR-07-2021-0160

- Bocken, N., & Konietzko, J. (2022). Circular business model innovation in consumer-facing corporations. Technological Forecasting and Social Change, 185, Article e122076. https://doi.org/10.1016/j.techfore.2022.122076

- Chang, C.-Y., Tsai, K.-H., & Sung, B. (2024). Can market knowledge lead to radical product innovation performance? The double-edged sword effect of absorptive capacity. European Journal of Innovation Management, 27(2), 403–423. https://doi.org/10.1108/EJIM-01-2022-0058

- Chatterjee, S., Chaudhuri, R., & Vrontis, D. (2024). Does data-driven culture impact innovation and performance of a firm? An empirical examination. Annals of Operations Research, 333(2), 601–626. https://doi.org/10.1007/s10479-020-03887-z

- Chaudhuri, R., Chatterjee, S., Vrontis, D., & Thrassou, A. (2024). Adoption of robust business analytics for product innovation and organizational performance: the mediating role of organizational data-driven culture. Annals of Operations Research, 339(3), 1757–1791. https://doi.org/10.1007/s10479-021-04407-3

- Damanpour, F., & Gopalakrishnan, S. (1998). Theories of organizational structure and innovation adoption: the role of environmental change. Journal of Engineering and Technology Management, 15(1), 1–24. https://doi.org/10.1016/S0923-4748(97)00029-5

- De Giovanni, P., & Cariola, A. (2021). Process innovation through industry 4.0 technologies, lean practices and green supply chains. Research in Transportation Economics, 90, Article e100869. https://doi.org/10.1016/j.retrec.2020.100869

- Farida, I., & Setiawan, D. (2022). Business strategies and competitive advantage: The role of performance and innovation. Journal of Open Innovation: Technology, Market, and Complexity, 8(3), Article e163. https://doi.org/10.3390/joitmc8030163

- Garg, N. (2019). High performance work practices and organizational performance-mediation analysis of explanatory theories. International Journal of Productivity and Performance Management, 68(4), 797–816. https://doi.org/10.1108/IJPPM-03-2018-0092

- Garousi, N. M., Mahdiraji, H. A., Jafarpanah, I., Jafari-Sadeghi, V., & Cardinali, S. (2020). Investigating the impact of networking capability on firm innovation performance: using the resource-action-performance framework. Journal of Intellectual Capital, 21(6), 1009–1034. https://doi.org/10.1108/JIC-01-2020-0005

- Hair, J. F., Howard, M. C., & Nitzl, C. (2020). Assessing measurement model quality in PLS-SEM using confirmatory composite analysis. Journal of Business Research, 109, 101–110. https://doi.org/10.1016/j.jbusres.2019.11.069

- Hamid, M., Sami, W., & Sidek, M. (2017). Discriminant validity assessment: Use of Fornell & Larcker criterion versus HTMT criterion. Journal of Physics: Conference Series, 890, Article e012163. https://doi.org/10.1088/1742-6596/890/1/012163

- Hashem, G., & Aboelmaged, M. (2024). The dynamic interplay of knowledge management, innovation and learning capabilities in digital supply chain adoption: a mediation-moderation model. Benchmarking: An International Journal, ahead-of-print (Advance online publication). https://doi.org/10.1108/BIJ-04-2023-0235

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/10.1007/s11747-014-0403-8

- Imran, M., Ismail, F., Arshad, I., Zeb, F., & Zahid, H. (2022). The mediating role of innovation in the relationship between organizational culture and organizational performance in Pakistan's banking sector. Journal of Public Affairs, 22(S1), e2717. https://doi.org/10.1002/pa.2717

- Iqbal, S., Rasheed, M., Khan, H., & Siddiqi, A. (2021). Human resource practices and organizational innovation capability: role of knowledge management. VINE Journal of Information and Knowledge Management Systems, 51(5), 732–748. https://doi.org/10.1108/VJIKMS-02-2020-0033

- Jalil, M. F., Ali, A., & Kamarulzaman, R. (2021). Does innovation capability improve SME performance in Malaysia? The mediating effect of technology adoption. The International Journal of Entrepreneurship and Innovation, 23(4), 253–267. https://doi.org/10.1177/14657503211048967

- Kör, B., Wakkee, I., & van der Sijde, P. (2021). How to promote managers' innovative behavior at work: Individual factors and perceptions. Technovation, 99, Article e102127. https://doi.org/10.1016/j.technovation.2020.102127

- Larios-Francia, R. P., & Ferasso, M. (2023). The relationship between innovation and performance in MSMEs: The case of the wearing apparel sector in emerging countries. Journal of Open Innovation: Technology, Market, and Complexity, 9(1), Article e100018. https://doi.org/10.1016/j.joitmc.2023.100018

- Lyytinen, K., & Rose, G. M. (2003). The Disruptive Nature of Information Technology Innovations: The Case of Internet Computing in Systems Development Organizations. MIS Quarterly, 27(4), 557–596. https://doi.org/10.2307/30036549

- Maqdliyan, R., & Setiawan, D. (2023). Antecedents and consequences of public sector organizational innovation. Journal of Open Innovation: Technology, Market, and Complexity, 9(2), Article e100042. https://doi.org/10.1016/j.joitmc.2023.100042

- Mayer, C. (2021). The future of the corporation and the economics of purpose. Journal of Management Studies, 58(3), 887–901. https://doi.org/10.1111/joms.12660

- Medda, G. (2020). External R&D, product and process innovation in European manufacturing companies. The Journal of Technology Transfer, 45(1), 339–369. https://doi.org/10.1007/s10961-018-9682-4

- Peltier, J. W., Zhao, Y., & Schibrowsky, J. A. (2012). Technology adoption by small businesses: An exploratory study of the interrelationships of owner and environmental factors. International Small Business Journal, 30(4), 406–431. https://doi.org/10.1177/0266242610365512

- Peñalba-Aguirrezabalaga, C., Ritala, P., & Sáenz, J. (2022). Putting marketing knowledge to use: marketing-specific relational capital and product/service innovation performance. Journal of Business & Industrial Marketing, 37(1), 209–224. https://doi.org/10.1108/JBIM-07-2020-0369

- Rajapathirana, R. P. J., & Hui, Y. (2018). Relationship between innovation capability, innovation type, and firm performance. Journal of Innovation & Knowledge, 3(1), 44–55. https://doi.org/10.1016/j.jik.2017.06.002

- Rasool, S. F., Samma, M., Wang, M., Zhao, Y., & Zhang, Y. (2019). How human resource management practices translate into sustainable organizational performance: The mediating role of product, process and knowledge innovation. Psychology Research and Behavior Management, 12, 1009–1025. https://doi.org/10.2147/PRBM.S204662

- Sánchez-Hernández, M. I., Robina-Ramirez, R., & Stankevičiūtė, Ž. (2023). Innovation and happiness management enhancing transcendence at work in the banking sector in Spain. European Journal of Innovation Management, ahead-of-print (Advanced online publication). https://doi.org/10.1108/EJIM-07-2023-0615

- Shahbaz, M. H., Naseem, M. A., Battisti, E., & Alfiero, S. (2024). The effect of green intellectual capital and innovative work behavior on green process innovation performance in the hospitality industry. Journal of Intellectual Capital, 25(2/3), 402–422. https://doi.org/10.1108/JIC-02-2023-0034

- Suhandiah, S., Suhariadi, F., Yulianti, P., & Abbas, A. (2023). Autonomy and feedback on innovative work behavior: The role of resilience as a mediating factor in Indonesian Islamic banks. Cogent Business & Management, 10(1), Article e2178364. https://doi.org/10.1080/23311975.2023.2178364

- Tarí, J. J., Claver-Cortés, E., & García-Fernández, M. (2023). How quality management can enhance performance? A model of relationships mediated by innovation. Production Planning & Control, 34(7), 587–603. https://doi.org/10.1080/09537287.2021.1946328

- Tripathi, A., & Dhir, S. (2024). Flourishing organizational innovation through psychological capital and organizational culture: An empirical examination. Journal of Public Affairs, 24(3), e2939. https://doi.org/10.1002/pa.2939

- Tülüce, N. S., & Yurtkur, A. K. (2015). Term of Strategic Entrepreneurship and Schumpeter's Creative Destruction Theory. Procedia - Social and Behavioral Sciences, 207, 720–728. https://doi.org/10.1016/j.sbspro.2015.10.146

- Wang, C., & Hu, Q. (2020). Knowledge sharing in supply chain networks: Effects of collaborative innovation activities and capability on innovation performance. Technovation, 94-95, Article e102010. https://doi.org/10.1016/j.technovation.2017.12.002

- Wang, M., Li, Y., Li, J., & Wang, Z. (2021). Green process innovation, green product innovation and its economic performance improvement paths: A survey and structural model. Journal of Environmental Management, 297, Article e113282. https://doi.org/10.1016/j.jenvman.2021.113282

- YuSheng, K., & Ibrahim, M. (2020). Innovation capabilities, innovation types, and firm performance: evidence from the banking sector of Ghana. SAGE Open, 10(2), 1–12. https://doi.org/10.1177/2158244020920892

- Zamani, E. D., Griva, A., & Conboy, K. (2022). Using business analytics for SME business model transformation under pandemic time pressure. Information Systems Frontiers, 24(4), 1145–1166. https://doi.org/10.1007/s10796-022-10255-8