Behavioral Finance: Impact of Psychology, Market Forces, and Social Influence on Portfolio Returns

Naveed Ul Haq1* ,Uzma Kashif2, Rabia Shahzad3, Ali Sajjad2, and Saira Sharif1

1University of Management and Technology, Lahore, Pakistan

2Superior University, Lahore, Pakistan

3Univerity of South Asia, Lahore, Pakistan

ABSTRACT

Traditional finance assumes rational decision-making in the stock market. This is challenged by behavioural finance, which postulates that cognitive biases, market dynamics, and social persuasion influence investors. Hence, this study on 300 retail investors at the Pakistan Stock Exchange (PSX) explores the impact of these factors on portfolio returns. The results indicate that cognitive biases, such as anchoring and overconfidence, lead to suboptimal decisions. Conversely, investors attuned to market dynamics make more successful choices, while resistance to social persuasion enhances decision quality. The findings highlight the need for investor awareness and mitigation of cognitive biases. Fund managers should incorporate these insights into strategies and regulators should educate investors on biases, while implementing policies against market manipulation.

1. INTRODUCTION

Investment stands as a fundamental instrument acknowledged for its pivotal role in creating economic stability and driving progress within a nation's economy (De Bondt et al., 2013). This dynamic involves the movement of capital between borrowers and lenders, culminating in the creation of aggregate demand (Wu et al., 2022). Diverse investment vehicles span various categories, presenting a spectrum from easily tradable and liquid options to less marketable and illiquid ones. Lenders allocate capital to borrowers based on their risk appetite, requirements, and projected returns (Narang et al., 2022). The intricate process of investment decision-making rests in the hands of investors or is sometimes delegated to managers. The term investment manifests in two distinct ways, namely economic and financial. Economic investment materializes through the allocation of capital to procure tangible assets, while financial investment entails the allocation of funds toward purchasing bonds, shares, debentures, mutual funds, and insurance (Ghosh & Aithal, 2022). This category of financial investment contributes significantly to the expansion of the capital market within an economy, facilitating the trade of long-term debt and equity-backed securities. Capital markets offer a platform where both borrowers and investors derive advantages surpassing what would have been attainable without engaging in these markets (Ahmadi & Peivandizadeh, 2022). Consequently, an economy experiences flourishing outcomes, including heightened income, consumption, savings, employment, and overall demand-supply equilibrium (Jia et al., 2020).

Capital markets are further segmented into primary and secondary markets. In primary markets, novel instruments such as bonds or shares are issued and acquired by various entities, including governmental bodies and corporations (Shaik et al., 2022). On the other hand, secondary markets revolve around the trading of pre-existing stocks or bonds, with individual securities undergoing multiple trades. The stock market serves as a linchpin within a nation's financial framework. It provides a venue for the listing and daily trading of prominent corporations' stocks, empowering these enterprises to amass supplementary capital by relinquishing ownership through share issuance to the general populace (Akçay & Hirshleifer, 2021). The shares held by investors boast liquidity attributes, facilitating swift and effortless security sales. The stock market's robust performance and efficient functionality enhance lenders' yields, tapping into proficiencies and enabling the optimal deployment of investments in liquid form, thus elevating its appeal to the broader public (Gong et al., 2022). Enterprises commanding higher share prices tend to attract more business investments, exerting influence over household consumption patterns and individual wealth. Hence, a country's capital market serves as a reflective mirror of its underlying economic landscape.

Risk management is a structured process that evaluates and analyzes risks to invest in opportunities and adjusts events that can affect the portfolio. It is crucial in situations where dependencies between portfolio components are high, the cost of failure is high, or when risks increase the risks of other components. Risk management identifies potential performance improvements, which can improve quality, customer satisfaction, and service levels for the organization and portfolio components (Abdolazimi et al., 2021). Behavioural finance is a field that combines behavioural and cognitive psychological theories with conventional economics and finance to explain people's economic decisions. It aims to address the inconsistencies in traditional utility maximization frameworks by focusing on human behaviour, both individually and in groups. Behavioural finance assumes that information structure and market participant characteristics influence investment decisions and market outcomes. Human brain processes information using shortcuts and emotional filters, leading to irrational behaviour, risk aversion, violations, and predictable errors in forecasts. These suboptimal financial decisions have significant implications for capital market efficiency, personal wealth, and corporate performance (Baker & Nofsinger, 2010).

Real-world market participants frequently behave differently from ideal ones, posing questions for theories such as the Efficient Market Hypothesis (EMH) and the Capital Asset Pricing Model (CAPM), for acting unpredictably (Asim et al., 2024). Investor bias is a prominent feature of behavioural finance, encompassing tendencies such as situations (representativeness) and availability bias, where recent events unduly influence decision-making based on overstated probabilities. The advent of behavioural finance has reshaped practitioners' perspectives on investment strategies, leading to a paradigm shift in the approach to capital market development (Subash, 2012). Bhanu (2023) conducted a survey that illuminated the benefits and challenges of behavioural finance. While the field offers a comprehensible framework to comprehend this phenomenon, its drawback lies in the ongoing struggle to decipher the underlying facts behind aggregate stock market dynamics, average returns, and individual trading patterns (Ady et al., 2020). The above research identified two pillars underpinning behavioural finance, that is, limits to arbitrage and psychology. Limits to arbitrage postulate that rational investors find it arduous to counteract or prevent dislocations created by their irrational counterparts. These dislocations manifest as mispriced assets and returns resulting from the behavioural biases of irrational investors. These instances theoretically present arbitrage opportunities, yet practical barriers impede their exploitation. Arbitrageurs encounter fundamental risk when hedging mispriced assets that lack fairly priced substitutes (Subash, 2012). High transaction costs associated with arbitrage trades pose another challenge. Moreover, short selling may be infeasible due to stock scarcity or regulatory restrictions. The second pillar, psychology, explores deviations from rational behaviour that are expected to occur in practice (Jing et al., 2023). The application of cognitive behaviour in risk perception includes investors undervaluing the hazards associated with their investments due to optimism and overconfidence.

Research Questions

The research questions of this study are as follows:

- How do cognitive biases, such as overconfidence, anchoring, and loss aversion, impact the portfolio decisions of retail investors in the Pakistan Stock Exchange (PSX)?

- In what ways do market dynamics influence the portfolio management strategies and investment outcomes of retail investors?

- What role does social persuasion, including herding behaviour and broker recommendations, play in shaping the investment decisions of retail investors?

- How do cognitive behaviours, market forces, and social influences interact to affect the overall returns of investment portfolios?

Objectives

Accordingly, the objectives of this study are as follows:

- To analyze the impact of specific cognitive biases on investment decisions and portfolio performance of retail investors in PSX.

- To evaluate how market trends, technological advancements, and economic conditions influence portfolio decisions and returns.

- To investigate the effect of social influences, such as peer behaviour and media information, on investment choices of retail investors.

- To explore the combined effect of cognitive behaviours, market dynamics, and social persuasion on portfolio returns.

Statement of the Problem

This study is concerned with stock market dynamics, with a particular focus on PSX and the role non-institutional investor behaviour plays in influencing market outcomes. The study highlights the crucial function performed by retail investors in the secondary market, stressing their participation directly or utilizing the Central Depository Company of Pakistan Limited as a broker. The profits from trading in the stock market are emphasized as being based on competence, while investor behaviour patterns are important factors that influence shareholder sentiment. This issue highlights a knowledge vacuum about the financial preferences and behaviours of retail investors at PSX, calling for a thorough examination of the variables affecting their performance and decision-making, considering PSX's increasing appeal as a destination for investments within the country. As long as there is strong market functionality, investor activity, and unanticipated events, the stock market's superior fluidity and potential for large but volatile returns are recognized. The problem statement highlights the necessity of investigating the factors impacting investor performance and decisions when interacting with PSX-listed firms. In doing so, the study seeks to close a major research gap by adding to a thorough understanding of the complexities associated with non-institutional investor involvement in the stock market, particularly in the context of the PSX.

Significance of the Study

The current research contributes significantly to the field of behavioural finance, particularly in the context of an emerging market such as Pakistan. Traditional finance theories such as the Efficient Market Hypothesis (EMH) and the Capital Asset Pricing Model (CAPM) assume rational decision-making by investors. However, real-world market participants often behave irrationally due to cognitive biases, social persuasion, and market dynamics, leading to suboptimal portfolio decisions and returns (Asim et al., 2024). By examining the interplay of these behavioural factors, the study offers a deeper understanding of the impact of investor psychology on market outcomes, challenging the assumptions of traditional finance and highlighting the necessity for a more nuanced approach to market analysis and portfolio management (Jing et al., 2023).

This study is novel in its comprehensive examination of multiple behavioural biases and their combined effect on investment decisions and portfolio returns at PSX. Previous research on behavioural finance often focused on isolated biases, such as overconfidence or herding behaviour (Qadri & Shabbir, 2014). In contrast, this study integrates a broader range of biases including cognitive biases (such as anchoring, availability bias), market dynamics (such as technological advancements, economic conditions), and social persuasion (such as peer influence, media reports). It also employs robust methodological approaches including Exploratory Factor Analysis (EFA), Confirmatory Factor Analysis (CFA), and Structural Equation Modeling (SEM) to validate the findings, providing a holistic view of the factors influencing investor behaviour and market efficiency.

Literature Review

Scholars in the field of behavioural finance analyze how people's psychological and social characteristics impact their investment decisions and portfolio performance through mediation and moderation analysis. These effects can either enhance or reduce the association between different behavioural aspects and investment performance. Biases such as overconfidence, anchoring, and availability bias are some of the major biases that affect investment decisions. Buying high and selling low are the effects of overconfidence. This is because investors are more willing to trade and think they have a competitive edge, hence boosting their portfolio returns if their trades are positive (Solares et al., 2022). Another source of inefficient decisions is anchoring in which investors make subsequent decisions based on the initial information; however, it can be helpful only if the initial information is correct (Qie et al., 2022). Also common is the availability bias where individuals make decisions based on the information that is more readily available or easily recalled; this also applies to trading behaviours and trading outcomes (Shafique, Sohail, et al., 2023).

It is in this context that the market forces of technology, the condition of the economy, and the prevailing trends in the markets influence investment plans, as well as the profitability of the portfolio. The investors who respond to market signals can adapt the structure of the portfolio to avoid risks and avail opportunities. It can moderate the effect of cognitive biases on portfolio returns, which is very helpful in improving decision-making quality and performance (Shirazi & Fuinhas, 2023). Thus, social influence, such as a reference group and media influence, has a strong influence over investors' decision to herd (Alkaraan et al., 2023). Such behaviour may create market trends that do not correlate with real economic values but can be rather beneficial in short-term, provided the majority is going in the right direction. However, it can also produce bubbles and crashes when the herd is wrong (Broietti et al., 2022).

Cognitive biases, market forces, and social persuasion can have mediating and moderating effects on the investment decision process. For example, portfolio decisions moderate the effect of cognitive behaviour on portfolio returns and also mediate between market forces and portfolio returns (Zahra et al., 2022). This mediation assures that cognitive biases and market characteristics affect the rate of portfolio return, mainly by affecting portfolio selections. Moderators are also meaningful in the same sense. For instance, the role of cognitive biases in the formation of a portfolio can be mitigated by an investor's ability to perceive and adapt to the market environment. An investor who is more sensitive to the market will also reduce the impacts of overconfidence or anchoring, resulting in positive investment performances (Gupta et al., 2022). Past researchers have also pointed out these mediation and moderation effects. Badhani (2024) asserted that limits to arbitrage and psychological factors are components of behavioural finance where cognitive factors and markets interact to influence investments.

Behavioural Finance

A major component of behavioural finance is investor prejudice which can take the form of overconfidence, availability bias, and representation (Badhani, 2024). These biases can change viewpoints on investment approaches and have an impact on the growth of the stock market. Badhani (2024) identified two pillars in behavioural finance, namely limits to arbitrage and psychology. Limits to arbitrage posit that rational investors struggle to counteract the mispricing caused by their irrational counterparts, citing practical barriers like transaction costs and short-selling constraints.

Portfolio Decision and Portfolio Returns

Strategic distribution of investments to meet the predetermined monetary objectives is known as portfolio decision (Gupta & Shrivastava, 2023). To balance the risk and return of an asset mix, an investor must be very careful and thoughtful regarding time horizon, risk tolerance, and investment goal. When making portfolio decisions, investors must follow the practice to diversify the asset class according to different types. It is done to mitigate the risk attached to the various classes of securities (Kumar et al., 2022). For successful portfolio administration, careful positioning of investments, identifying considerations for risk, and adjusting market trends for shifting is required. The complexities of portfolio decision-making are highlighted by market forces, cognitive behavior, and the intersection of social influence.

Cognitive Behaviour and Portfolio Decisions

Mental heuristics, which can impair the ability of judgement, are influenced by cognitive processes on which financial investor frequently relies while making financial decisions to establish portfolios (Almansour et al., 2023). Individuals often make logical assumptions while making decisions. Moreover, investors also focus on economic assumptions, termed as cognitive biases, while driving financial decisions (Majewski & Majewska, 2022). Sometimes investors are overconfident based on their past experiences and believe that they can anticipate the market. Occasionally, investors confirm and trust their information sources which makes them confident in selecting and opting for a portfolio, even if they have very limited experience regarding the wider perspective (Shafique, Rashid, et al., 2023).

Market Dynamics and Portfolio Decisions

Ever changing market landscape influences investment strategy and the creation of portfolios (Spelta et al., 2022). Investors' continuous vigilance, improvements in technology, and prevailing economic trends have a significant impact on the financial sector (Shirazi & Fuinhas, 2023). Logical association between various classes of assets, liquidity, variations, and understanding the trends are the factors which can help to make attractive portfolio decisions (Sinha et al., 2022). Investors seek higher risks for higher returns for particular ventures in a bullish market; however, these investors become loss-aversive and protect themselves in times of economic downturns (Gunjan & Bhattacharyya, 2023).

Social Persuasion and Portfolio Decisions

Occasionally, financial investors also practice discussing and taking guidance from their close circles, so social persuasion has a positive impact on portfolio decisions (Alkaraan et al., 2023). Various investment prospects such as the news from media, economic indicators, and the behaviour of peers also have a significant impact on investors' decision-making process (Qie et al., 2022). Fear of Missing Out or FOMO is a well-known terminology which manifests the herding nature of investors to go with the voices of their social circle, rather than investigating the findings from cognitive processes. The same is the case with the news from social media which can also create a positive influence on a particular class of an asset to agree or not to invest. Furthermore, investors get financial advice from close friends and important personalities who have potential importance in the public to invest or not to invest (Broietti et al., 2022).

Social Persuasion, Cognitive Behaviour, Market Dynamics, Portfolio Decisions, and Portfolio Returns

Portfolio decisions have a mediating impact between social persuasion, cognitive behaviour, market dynamics, and portfolio returns (Zahra et al., 2022). Social persuasion is the investment strategy in which investors rely on the news from social groups, peers, and potential personalities and include it in their decision-making process (Wei et al., 2022). Cognitive behaviour is acknowledging, identifying, and processing market data most logically. This helps the investors to make rational and knowledge-supported choices which can lead them to the correct path and get them maximum returns on investment (Hoffmann, 2023).

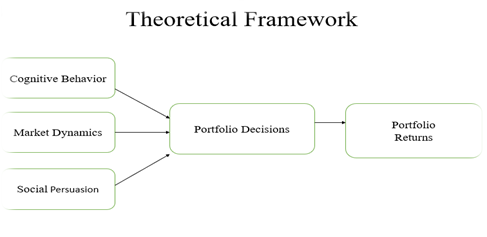

Figure 1Conceptual Model

Hypotheses

H1: Cognitive biases, such as overconfidence and anchoring, significantly influence portfolio decisions of retail investors in PSX.

H2: Awareness and responsiveness to market dynamics have a significant impact on portfolio decisions of retail investors in PSX.

H3: Social persuasion, including recommendations from peers and media influence, significantly affects the portfolio decisions of retail investors in PSX.

H4: Portfolio decisions made by retail investors in PSX significantly influence their portfolio returns.

H5: Cognitive biases, such as overconfidence and loss aversion, have a significant impact on portfolio returns of retail investors in PSX.

H6: Being attuned to market dynamics significantly enhances the portfolio returns of retail investors in PSX.

H7: Social persuasion significantly affects the portfolio returns of retail investors in PSX.

H8: Portfolio decisions mediate the relationship between cognitive behaviour and portfolio returns among retail investors in PSX.

H9: Portfolio decisions mediate the relationship between market dynamics and portfolio returns among retail investors in PSX.

H10: Portfolio decisions mediate the relationship between social persuasion and portfolio returns among retail investors in PSX.

H11: Cognitive behaviour, market dynamics, and social persuasion collectively have a significant impact on the portfolio decisions of retail investors in PSX.

H12: Cognitive behaviour, market dynamics, and social persuasion collectively have a significant impact on the portfolio returns of retail investors in PSX.

Underpinning Theories

Behavioural finance poses challenges to the classical finance theory by highlighting the impact of psychological factors and social factors in financial decisions. The theoretical framework of behavioural finance consists of two main pillars, namely limits to arbitrage and psychology (Badhani, 2024). The limits to arbitrage imply that rational investors cannot always eliminate market inefficiencies resulting from irrational behaviours because of factors such as transaction costs and restrictions on short-selling (Mitchell & Pulvino, 2012). The psychology pillar examines how individuals have a set of cognitive and affective heuristics that causes them to commit systematic mistakes and inefficient choice-making regarding risk and investment (Velte, 2023).

Behavioural finance combines behavioural and cognitive psychological theories with classical economics and finance paradigms. The aim is to describe and analyze why investors make wrong decisions in the context of financial markets and practice, contrary to the rational expectations of the neoclassical theories of finance. Conventional finance theories, such as EMH and CAPM, presuppose that an investor is an economic man since s/he behaves rationally to attain the highest level of satisfaction given the available information (Baker & Nofsinger, 2010). However, in actual situations, investors are often observed to make undesirable decisions due to the effects of cognitive biases, social pressure, and market dynamics, resulting in the creation of non-efficient portfolios and inefficient markets (Asim et al., 2024).

Conceptual biases play a crucial role in shaping investors' decisions because they alter how information is evaluated and risks and rewards are estimated. Examples of cognitive biases are overconfidence, anchoring, and loss aversion. Overconfidence bias makes investors overestimate their knowledge and ability to predict future prices, leading to overtrading and risk-taking (Solares et al., 2022). Anchoring bias leads investors to give a lot of weight to the first piece of information received (the anchor), thus they make wrong decisions on investment (Qadri & Shabbir, 2014). This is an investment behaviour where investors are more willing to avoid an equivalent loss than acquire an equivalent gain. This is because investors are risk averse and this makes them avoid investment opportunities that may not give them the best returns (Shafique, Sohail, et al., 2023).

Some of the most important factors that affect investment decisions include market forces, such as technology, economics, and trends. It is wise for investors to be sensitive to such factors so that they can always move to the next level, whenever the market catches them up (Spelta et al., 2022). Market characteristics determine the levels of liquidity and volatility of securities, thus impacting the investors' ethical stance and decision-making (Gunjan & Bhattacharyya, 2023). For instance, in the period of rising markets, investors are more likely to seek risks as compared to the periods of falling markets, the time when investors tend to avoid risks.

Relative to other factors, social influence, including herding behaviour and the effect of peers and media on investment decisions, is a major factor. Herding behaviour is one where investors mimic the decisions made by other investors in the market, thereby fuelling bubbles (Broietti et al., 2022). Media and recommendations from brokers and financial specialists also influence investors' decisions, which may lead to irrational investment decisions based on sensationalism or bias for the available information (Alkaraan et al., 2023).

Cognitive bias, markets, and social persuasion are important influences which make decision-making on investment a rather intricate process. Market signals can be interpreted through cognitive biases and, therefore, the response to them is not always rational. For instance, overconfidence can make investors fail to consider bearish signals in the market, since they feel that they can predict the market better than anyone else (Shafique, Sohail, et al., 2023). Likewise, social factors can reinforce cognitive biases as investors might depend on other people's opinions or news instead of doing their own research (Gupta et al., 2022).

Methodology

Data and Method

The current study opted for simple random sampling to ensure that every participant was provided with equal opportunity to become a part of the research. Lahore is also an important hub for stock market operations. A quantitative technique was used to measure the objectivity of variables. So, surveys were sent to brokerage offices via the internet. A sample of 250 retail investors was selected from the Lahore Stock Exchange, in 2022.

The reason for selecting retail investors is critical to understand the broader dynamics of the stock market, particularly in the context of PSX. The behaviour of retail investors is different from that of institutional investors and they are also categorized differently. These differences are usually the result of cognitive and social processes, as well as caused by the limited availability of advanced financial instruments. It has been established that the instances of behavioural biases, such as overconfidence, self-attitudes, anchoring, and herding are more observable in retail investors, thus affecting their investment decisions and portfolio performance (Barber & Odean, 2000). It is important to fully grasp these biases to allow for the formulation of specific approaches that impact the results of their investments. Small investors are a significant proportion of market players in most of the emerging economies, including Pakistan. Collective action in the market by the investors can influence market operations and asset prices. Thus, by concentrating on retail players, this work seeks to establish those behaviours which underpin the fluctuations in the market as well as market volatility, which is of direct value to policymakers, regulators, and market players (Bashir et al., 2013). In particular, the field of behavioural finance describes the impact of psychological factors on the behaviour of retail investors in detail. In this way, by focusing on this group, the current study would be able to examine the influence of these factors more specifically, without interference from institutional investors and their strategies, which are generally motivated by different goals and conditions (Subrahmanyam, 2008).

To mitigate the errors and generalizations of findings, a robust research design was prepared. By sending pre-tested surveys to 300 retail investors in the stock market in Lahore, the study exceeded the suggested sample size standards, bolstering the reliability and generalization of the findings. The robust sampling design was aimed to mitigate errors, including sampling, coverage, and measurement errors, fortifying the research's scientific rigour. Aligned with the study objectives, survey emerged as the optimal method for data collection (Hair et al., 2019). Transparency and collaboration with the brokerage ensured a valuable contribution for the current study. Self-administered approach demonstrating respondent commitment and the response rate was 92%.

Results

Table 1 shows the demographic profiles of the respondents of this study. The demographic profiles of the 300 retail investors show a predominance of young to middle-aged, highly educated males with moderate investment experience and income levels. Specifically, the sample consists of 86% male participants and 14% female participants, with the majority aged between 26 and 45 years. Most participants are married (71.3%) and possess at least a Bachelor's degree (67%), with 30% holding a Master's degree, and 6% having a PhD. Income-wise, 43% of participants earn between 50,000 and 100,000 rupees monthly, while 25% earn less than 50,000 rupees. In terms of investment experience, 31% have 3-5 years of experience and 27% have 1-3 years of experience. The largest group of respondents (30%) has invested between 100,000 and 500,000 rupees in PSX, indicating a moderate level of investment activity. This demographic composition provides a useful context for analyzing the behavioural finance factors influencing investment decisions and portfolio returns.

Table 1 Demographic Profiling of Respondents (N = 300)| Demographic Profile | Frequency | % |

|---|---|---|

| Gender | ||

| Male | 258 | 86 |

| Female | 42 | 14 |

| Age | ||

| 18 – 25 | 53 | 18 |

| 26 – 35 | 94 | 31 |

| 36 – 45 | 86 | 29 |

| 46 – 55 | 46 | 15 |

| Over 55 | 21 | 7 |

| Marital Status | ||

| Single | 76 | 25.3 |

| Married | 214 | 71.3 |

| Divorced | 10 | 3.3 |

| Educational Qualification | ||

| Primary Education | 13 | 4 |

| Secondary Education | 54 | 18 |

| Bachelors | 112 | 37 |

| Masters | 90 | 30 |

| PhD Degree | 17 | 6 |

| Others | 14 | 5 |

| Monthly Income in Rupees | ||

| Less than 50,000 | 76 | 25 |

| 50,000 – 100,000 | 128 | 43 |

| 100,000 – 150,000 | 67 | 22 |

| 150,000 Above | 29 | 10 |

| Years of Investment Experience | ||

| Less than 1 year | 23 | 8 |

| 1 – under 3 years | 81 | 27 |

| 3 – under 5 years | 94 | 31 |

| 5 – under 10 years | 51 | 17 |

| Over 10 years | 51 | 17 |

| Amount of Investment in P-S-X (Rs) | ||

| Less than 1 lac | 32 | 10.7 |

| 1 lac – 5 lac | 90 | 30 |

| 5 lac – 1 million | 71 | 23.7 |

| 1 million – 2.5 million | 53 | 17.7 |

| 2.5 million – 5 million | 33 | 11 |

| Above 5 million | 21 | 7 |

Measurement Model Assessment

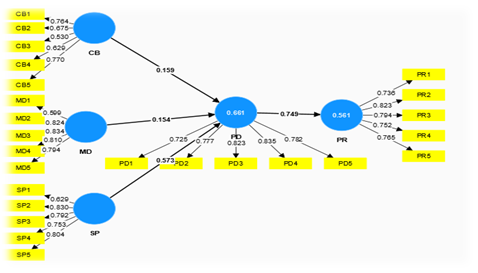

The constructs' factor loadings, Average Variance Extracted (AVE), and Composite Reliability (CR) were used to assess their validity, as shown in Table 2. The validity of the constructs is said to be convergent when items have higher factor loadings (>0.50) (Hair et al., 2019). The results demonstrate that the factor loadings are greater than 0.50. The convergent validity of the constructs was evaluated using AVE and CR. The AVE values for each build are more than 0.50.

Table 2 Convergent Validity| Demographic Profile | Frequency | % |

|---|---|---|

| Gender | ||

| Male | 258 | 86 |

| Female | 42 | 14 |

| Age | ||

| 18 – 25 | 53 | 18 |

| 26 – 35 | 94 | 31 |

| 36 – 45 | 86 | 29 |

| 46 – 55 | 46 | 15 |

| Over 55 | 21 | 7 |

| Marital Status | ||

| Single | 76 | 25.3 |

| Married | 214 | 71.3 |

| Divorced | 10 | 3.3 |

| Educational Qualification | ||

| Primary Education | 13 | 4 |

| Secondary Education | 54 | 18 |

| Bachelors | 112 | 37 |

| Masters | 90 | 30 |

| PhD Degree | 17 | 6 |

| Others | 14 | 5 |

| Monthly Income in Rupees | ||

| Less than 50,000 | 76 | 25 |

| 50,000 – 100,000 | 128 | 43 |

| 100,000 – 150,000 | 67 | 22 |

| 150,000 Above | 29 | 10 |

| Years of Investment Experience | ||

| Less than 1 year | 23 | 8 |

| 1 – under 3 years | 81 | 27 |

| 3 – under 5 years | 94 | 31 |

| 5 – under 10 years | 51 | 17 |

| Over 10 years | 51 | 17 |

| Amount of Investment in P-S-X (Rs) | ||

| Less than 1 lac | 32 | 10.7 |

| 1 lac – 5 lac | 90 | 30 |

| 5 lac – 1 million | 71 | 23.7 |

| 1 million – 2.5 million | 53 | 17.7 |

| 2.5 million – 5 million | 33 | 11 |

| Above 5 million | 21 | 7 |

Discriminant Validity

Table 3 displays the HTMT ratio, a useful method for gaining access to discriminant validity. The HTMT ratio should be less than 0.90 to demonstrate discriminant validity. All ratio values meet this condition, which provides proof that discriminant validity is established (Rasoolimanesh et al., 2022).

Table 3 HTMT Ratio| CB | MD | SP | PD | PR | |

|---|---|---|---|---|---|

| CB | - | ||||

| MD | 0.808 | - | |||

| SP | 0.735 | 0.651 | - | ||

| PD | 0.775 | 0.866 | 0.763 | - | |

| PR | 0.723 | 0.791 | 0.701 | 0.702 | - |

In Table 4, SEM PLS structural model analysis was conducted. The study used the bootstrapping procedure to assess the significance of the path coefficients. According to the tests applied and results derived, all the hypotheses are “supported” since the values of p and t are up to the mark, that is, the p-values are less than 0.05 and the t-values are greater than 1.645.

Table 3 Direct and Indirect Effects|

Hypotheses |

Beta |

t-values |

p-values |

Decisions |

|

|---|---|---|---|---|---|

|

H1 |

CB→ PD |

0.084 |

5.695 |

0.000 |

Supported |

|

H2 |

MD→ PD |

0.099 |

3.827 |

0.000 |

Supported |

|

H3 |

SP → PD |

0.087 |

3.082 |

0.002 |

Supported |

|

H4 |

PD → PR |

0.124 |

3.405 |

0.001 |

Supported |

|

Mediation Analysis |

|||||

|

H5 |

CB* MD*SP→ SCSP →SCGP |

0.186 |

2.838 |

0.005 |

Supported |

Discussion

The investors’ cognitive behaviour significantly influences the portfolio returns at PSX in a positive way. Overconfidence, anchoring, availability bias, and loss aversion are the psychological characteristics included in this variable (Qie et al., 2022). It implies that there is a direct correlation between all of these variables and Return on Investment or ROI. Overconfident investors tend to trade more than logical investors. Moreover, as higher trading translates into better returns, this can have a favourable effect on portfolio returns (Solares et al., 2022). Similarly, availability bias and anchoring also have a favourable effect on performance. Hence, the more people respond to first-hand knowledge, the more transactions they complete, and ultimately, the more returns they generate (Shafique et al., 2023). On the contrary, according to Barberis and Jin (2023), investors who are risk-averse about the particular shares they own typically see positive returns. Even if they perceive less risk, which results in lower returns, it can nevertheless have a positive impact on retail investors' performance by reducing losses and increasing return volatility.

The study examined some stocks market-related variables that affect investors and ultimately determine their success (Au et al., 2024). Some of the factors include investor overreaction to market fluctuations in share prices, market data, historical share trends, and a preference for dividends or the right shares of a specific listed company. It was determined that every aspect significantly and favourably affects investors' performance (Metawea et al., 2022). Lastly, a small percentage of investors are often risk averse and favour stocks that offer more dividends or rights than other stocks. Even though they still provide lower returns than risk-seeking investors, they are less likely to experience losses since they take on less risk. As a result, they can produce strong portfolio returns in the market. The literature provides support for these conclusions. Herding and broker recommendations are two behavioural elements included in the ‘social persuasion’ variable. The results prove that these factors significantly and favorably affect investors' portfolio returns at PSX (Yuan et al., 2022). The first factor, namely herding, demonstrates that PSX retail investors copy the choices made by others regarding stock types, quantities, and buying/selling behaviours. It influences the portfolio returns in a favorable way. The findings suggest that retail investors typically rely on partnerships to boost their performance and generate erratic returns because PSX is an emerging market in Asia. To maximize returns, these investors who follow the herd, however, must carefully weigh the positive and negative effects of doing so on various parts of their portfolio returns. The results of this investigation are in line with earlier researches.

Conclusion

This research aimed to investigate the behavioural elements influencing retail investors' portfolio returns at PSX and, consequently, their investment decisions. For data analysis, EFA was used along with CFA and regression estimates obtained through the use of SEM, ensuring the validity and reliability of the information gathered from the respondents. Following factor analysis, all fifteen (15) behavioural components were classified into five (05) variables, of which only three (03) were determined to have an effect on retail investors' portfolio decisions at PSX. The first variable, namely investors' cognitive behaviour, was found to have a minor impact on decisions. This variable comprises elements such as overconfidence, anchoring, availability biases, loss aversion, and regret aversion. It was also discovered that other regret- and mental accounting-related factors have little influence on retail investors' choices. The second variable, namely market dynamics, refers to the factors influencing retail investors' portfolio decisions. These include the significant impact of market information, investors' tendency to overreact to price fluctuations, historical stock trends, and a preference for dividends or rights shares. Customer preferences for the company and the underlying stocks' fundamentals were determined to have little bearing on investors’ choices. The final variable ‘social persuasion’ indicated the moderate influence of broker recommendations and herding, whereas the opinions of friends and family were found to have little bearing on the decisions made by investors at PSX. Using SEM, these three variables were examined to determine their impact on retail investors' portfolio returns after low-impact factors were eliminated. The outcomes showed that all three variables significantly and positively impacted portfolio returns. At PSX, it was determined that market dynamics have the most positive significant influence on retail investors' portfolio returns. Furthermore, herding is the second most influential element, while retail investors' cognitive behaviour has the least influence.

Policy Implications

This study will benefit policymakers who want to enhance the efficiency of the market and the investors’ safeguards in PSX. Previous studies revealed that various cognitive biases including overconfidence, anchoring, and availability bias affect the decisions of retail investors.

Implications for InvestorsWith respect to the overall study, it can be summarized that for individual investors, self-control and knowledge about biases should be of essence. Thus, investors should try to comprehend how factors such as overconfidence and loss aversion may affect their decisions and results. Some of these include investing in different areas (so that if one market fails the other may survive), having specific long-term investment goals, and not investing because of the latest trends or peer pressure.

Implications for Financial Institutions and AdvisorsBanking and financial institutions and their advisors have the responsibility of undoing the behavioural biases established in this study. They can come up with specific investment plans that take into consideration the heuristics that are often displayed by the average investor. For example, the provision of decision strategies in financial products can assist in reducing the impacts of overconfidence and anchoring.

Implications for the Stock MarketThe findings of this study can be useful to improve the PSX market structure and the way it deals with investors. The government, financial industry, and other stakeholders can launch investor education campaigns and conduct workshops and seminars based on the behavioural finance concepts that equip retail investors with proper knowledge to deal with market challenges.

Limitations of Study

The current study's sample size is restricted to 300 respondents solely from Lahore, Pakistan. Further research at PSX may yield more accurate results with a bigger sample size. The study was carried out over a time span during which the secondary market exhibited various oscillations, leading to changes in investor preferences and purchasing habits. The impact of these oscillations is too much for this research to measure.

Recommendations

According to the study, retail investors' choices and behavioural traits impact their desire to purchase a specific stock of a listed company at PSX, which may have an impact on their portfolio returns. A thorough understanding of this business would enable retail investors to make better decisions and achieve higher returns on their investments, which would support Pakistan's developing secondary market and may also open up new opportunities for both domestic and foreign investors. Government and relevant authorities should take the initiative to offer training programs to educate investors about their behavioural elements, so they may perform better in the market to attain this goal.

Future Research

It is advised that a larger sample size of investors be used in future studies to validate the findings of this study. The subjective criterion for measuring portfolio returns based on respondents' perceptions is a key limitation of this study. For future research, this suggests the need for a more objective approach to evaluate portfolio performance. Using actual market data, financial statements, or performance metrics may provide a more accurate assessment, reducing biases introduced by individual perceptions. This shift would enhance the validity of the findings and offer a clearer understanding of the factors affecting portfolio returns.

CONFLICT OF INTEREST

The authors of the manuscript have no financial or non-financial conflict of interest in the subject matter or materials discussed in this manuscript.

DATA AVAILABILITY STATEMENT

The data associated with this study will be provided by the corresponding author upon request.

FUNDING DETAILS

No funding has been received for this research.

REFERENCES

- Abdolazimi, O., Shishebori, D., Goodarzian, F., Ghasemi, P., & Appolloni, A. (2021). Designing a new mathematical model based on ABC analysis for inventory control problem: A real case study. RAIRO-operations Research, 55(4), 2309–2335. https://doi.org/10.1051/ro/2021104

- Ady, S. U., Tyas, A. M., Farida, I., & Gunawan, A. W. (2020). Immediate and expected emotions toward stock returns through overconfidence and cognitive dissonance: The Study Of Indonesian investor behavior. PalArch's Journal of Archaeology of Egypt/Egyptology, 17(3), 1140–1165.

- Ahmadi, S. A., & Peivandizadeh, A. (2022). Sustainable portfolio optimization model using promethee ranking: A case study of palm oil buyer companies. Discrete Dynamics in Nature and Society, 2022, Article e8935213. https://doi.org/10.1155/2022/8935213

- Akçay, E., & Hirshleifer, D. (2021). Social finance as cultural evolution, transmission bias, and market dynamics. Proceedings of the National Academy of Sciences, 118(26), Article e2015568118. https://doi.org/10.1073/pnas.2015568118

- Alkaraan, F., Albahloul, M., & Hussainey, K. (2023). Carillion's strategic choices and the boardroom's strategies of persuasive appeals: Ethos, logos and pathos. Journal of Applied Accounting Research, 24(4), 726–744. https://doi.org/10.1108/JAAR-06-2022-0134

- Almansour, B. Y., Elkrghli, S., & Almansour, A. Y. (2023). Behavioral finance factors and investment decisions: A mediating role of risk perception. Cogent Economics & Finance, 11(2), Article e2239032. https://doi.org/10.1080/23322039.2023.2239032

- Asim, M., Khan, M. Y., & Shafi, K. (2024). Investigation of herding behavior using machine learning models. Review of Behavioral Finance, 16(3), 424–438. https://doi.org/10.1108/RBF-05-2023-0121

- Au, S.-Y., Dong, M., & Zhou, X. (2024). Does social interaction spread fear among institutional investors? Evidence from coronavirus disease 2019. Management Science, 70(4), 2406–2426. https://doi.org/10.1287/mnsc.2023.4814

- Badhani, P. (2024). Behavioral economics in policy making. Indian Insituite of Ahmadabad. https://www.iima.ac.in/sites/default/files/2024-04/MCFME_RPIFME_1_27.03.2024.pdf

- Baker, H. K., & Nofsinger, J. R. (2010). Behavioral finance: An overview. In H. K. Baker & J. R. Nofsinger (Eds.), Behavioral finance: Investors, corporations, and markets (pp. 1–21). John Wiley & Sons.

- Barber, B. M., & Odean, T. (2000). Trading is hazardous to your wealth: The common stock investment performance of individual investors. The Journal of Finance, 55(2), 773–806. https://doi.org/10.1111/0022-1082.00226

- Barberis, N. C., & Jin, L. J. (2023). Model-free and model-based learning as joint drivers of investor behavior (Working Paper No. 31081). National Beraeu of Economic Research. https://www.nber.org/papers/w31081

- Bashir, T., Azam, N., Butt, A. A., Javed, A., & Tanvir, A. (2013). Are behavioral biases influenced by demographic characteristics & personality traits? Evidence from Pakistan. European Scientific Journal, 9(29), 277–293.

- Bhanu, B. K. (2023). Behavioral finance and stock market anomalies: Exploring psychological factors influencing investment decisions. In N. Joshi, D. Sharma, R. P. Mahurkar, Dr. K. Shailashree, R. L. Kumari, T. Ilakkiya, N. Oswal, & P. K. Ingale (Eds.), Advancements in commerce, economics & management: A research compilation (pp. 23–32). Redshine Publication.

- Broietti, C., Rover, S., & Azevedo, G. M. d. C. (2022). Investor behaviour in an environment of uncertainty: the impact of persuasion on investor decisions. International Journal of Applied Decision Sciences, 15(6), 663–680. https://doi.org/10.1504/IJADS.2022.126099

- De Bondt, W., Mayoral, R. M., & Vallelado, E. (2013). Behavioral decision-making in finance: An overview and assessment of selected research. Spanish Journal of Finance and Accounting/Revista Española de Financiación y Contabilidad, 42(157), 99–118. https://doi.org/10.1080/02102412.2013.10779742

- Ghosh, S., & Aithal, P. (2022). Behaviour of investment returns in the disinvestment environment: The case of power industry in Indian CPSEs. International Journal of Technology, Innovation and Management, 2(2), 65–79. https://doi.org/10.54489/ijtim.v2i2.95

- Gong, X., Min, L., & Yu, C. (2022). Multi-period portfolio selection under the coherent fuzzy environment with dynamic risk-tolerance and expected-return levels. Applied Soft Computing, 114, Article e108104. https://doi.org/10.1016/j.asoc.2021.108104

- Gunjan, A., & Bhattacharyya, S. (2023). A brief review of portfolio optimization techniques. Artificial Intelligence Review, 56(5), 3847–3886. https://doi.org/10.1007/s10462-022-10273-7

- Gupta, N., Park, H., & Phaal, R. (2022). The portfolio planning, implementing, and governing process: An inductive approach. Technological Forecasting and Social Change, 180, Article e121652. https://doi.org/10.1016/j.techfore.2022.121652

- Gupta, S., & Shrivastava, M. (2023). Behavioral finance: A critical literature review using Pareto analysis. Thailand and the World Economy, 41(2), 156–183.

- Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2–24. https://doi.org/10.1108/EBR-11-2018-0203

- Hoffmann, C. P. (2023). Investor relations as strategic communication: Insights from evolutionary psychology. International Journal of Strategic Communication, 17(3), 213–227. https://doi.org/10.1080/1553118X.2023.2230575

- Jia, W., Redigolo, G., Shu, S., & Zhao, J. (2020). Can social media distort price discovery? Evidence from merger rumors. Journal of Accounting and Economics, 70(1), Article e101334. https://doi.org/10.1016/j.jacceco.2020.101334

- Jing, D., Imeni, M., Edalatpanah, S. A., Alburaikan, A., & Khalifa, H. A. E.-W. (2023). Optimal selection of stock portfolios using multi-criteria decision-making methods. Mathematics, 11(2), Article e415. https://doi.org/10.3390/math11020415

- Kumar, S., Guha, S., & Ali, S. (2022). Applying behavioural finance approach to investment decisions: determinants of investment. In R. N. Subudhi, S. Mishra, A. Saleh, & D. Khezrimotlagh (Eds.), Future of Work and Business in Covid-19 Era: Proceedings of IMC-2021 (pp. 57–71). Springer.

- Majewski, S., & Majewska, A. (2022). Behavioral portfolio as a tool supporting investment decisions. Procedia Computer Science, 207, 1713–1722. https://doi.org/10.1016/j.procs.2022.09.229

- Metawea, M., Metawa, S., & Metawa, N. (2022). Predicting stock return risk and volatility using neural network. In N. Metawa, M. K. Hassan, & S. Metawa (Eds.), Artificial Intelligence and Big Data for Financial Risk Management: Intelligent Applications (pp. 67–82). Routledge.

- Mitchell, M., & Pulvino, T. (2012). Arbitrage crashes and the speed of capital. Journal of Financial Economics, 104(3), 469–490. https://doi.org/10.1016/j.jfineco.2011.09.002

- Narang, M., Joshi, M. C., Bisht, K., & Pal, A. (2022). Stock portfolio selection using a new decision-making approach based on the integration of fuzzy CoCoSo with Heronian mean operator. Decision Making: Applications in Management and Engineering, 5(1), 90–112. https://doi.org/10.31181/dmame0310022022n

- Qadri, S. U., & Shabbir, M. (2014). An empirical study of overconfidence and illusion of control biases, Impact on investor's decision making: An evidence from ISE. European Journal of Business and Management, 6(14), 38–44.

- Qie, X., Wu, J., Li, Y., & Sun, Y. (2022). A stage model for agent-based emotional persuasion with an adaptive target: From a social exchange perspective. Information Sciences, 610, 90–113. https://doi.org/10.1016/j.ins.2022.07.147

- Rasoolimanesh, S. M., Seyfi, S., Rather, R. A., & Hall, C. M. (2022). Investigating the mediating role of visitor satisfaction in the relationship between memorable tourism experiences and behavioral intentions in heritage tourism context. Tourism Review, 77(2), 687–709. https://doi.org/10.1108/TR-02-2021-0086

- Shafique, M. R., Sohail, A., Nisar, S., & Munir, M. (2023). Examining financial decision-making of retail investors in Pakistan Stock Exchange (PSX): Moderating role of financial literacy. Journal of Applied Research and Multidisciplinary Studies, 4(1), 2–22. https://doi.org/10.32350/JARMs/vol.41.01

- Shafique, U., Rashid, U., Awan, F. G., Anwaar, H., & Nzanywayingoma, F. (2023). Diversification of energy resources for electricity generation in Pakistan via portfolio optimization. IEEE Access, 11, 126724–126732. https://doi.org/10.1109/ACCESS.2023.3328327

- Shaik, M. B., Kethan, M., Jaggaiah, T., & Khizerulla, M. (2022). Financial literacy and investment behaviour of IT professional in India. East Asian Journal of Multidisciplinary Research, 1(5), 777–788. https://doi.org/10.55927/eajmr.v1i5.514

- Shirazi, M., & Fuinhas, J. A. (2023). Portfolio decisions of primary energy sources and economic complexity: The world's large energy user evidence. Renewable Energy, 202, 347–361. https://doi.org/10.1016/j.renene.2022.11.050

- Sinha, A., Sharif, A., Adhikari, A., & Sharma, A. (2022). Dependence structure between Indian financial market and energy commodities: A cross-quantilogram based evidence. Annals of Operations Research, 313(1), 257–287. https://doi.org/10.1007/s10479-021-04511-4

- Solares, E., De-León-Gómez, V., Salas, F. G., & Díaz, R. (2022). A comprehensive decision support system for stock investment decisions. Expert Systems with Applications, 210, Article e118485. https://doi.org/10.1016/j.eswa.2022.118485

- Spelta, A., Pecora, N., & Pagnottoni, P. (2022). Chaos based portfolio selection: A nonlinear dynamics approach. Expert Systems with Applications, 188, Article e116055. https://doi.org/10.1016/j.eswa.2021.116055

- Subash, R. (2012). Role of behavioral finance in portfolio investment decisions: Evidence from India [Master thesis, Univerzita Karlova]. Charles Digital Repository. https://dspace.cuni.cz/handle/20.500.11956/43150

- Subrahmanyam, A. (2008). Behavioural finance: A review and synthesis. European Financial Management, 14(1), 12–29. https://doi.org/10.1111/j.1468-036X.2007.00415.x

- Velte, P. (2023). Sustainable institutional investors, corporate sustainability performance, and corporate tax avoidance: Empirical evidence for the European capital market. Corporate Social Responsibility and Environmental Management, 30(5), 2406–2418. https://doi.org/10.1002/csr.2492

- Wei, J., Liu, X., & Fan, W. (2022). Dynamic sparse portfolio rebalancing model: A perspective of investors' behavior-related decisions. Knowledge-Based Systems, 251, Article e109224. https://doi.org/10.1016/j.knosys.2022.109224

- Wu, C. C., Yan, Y., Yuan, T., Huang, C. C., & Tsai, Y. J. (2022). A study of network negative news based on behavioral finance analysis of abnormal fluctuation of stock price. Discrete Dynamics in Nature and Society, 2022, Article e7952532. https://doi.org/10.1155/2022/7952532

- Yuan, Y., Wang, H., & Jin, X. (2022). Pandemic-driven financial contagion and investor behavior: Evidence from the COVID-19. International Review of Financial Analysis, 83, Article e102315. https://doi.org/10.1016/j.irfa.2022.102315

- Zahra, A., Oktavia, T., Gaol, F. L., & Hosoda, T. (2022, December 17–19). Personal development model: cognitive behavioural therapy [Paper presentation]. Proceedings of 11th International Congress on Advanced Applied Informatics. Jakarta, Indonesia.