Unveiling the Enigma of Tax Evasion: A Pakistani Perspective

Muhammad Sohail1*, Wajid Alim2, Ammar Ud din2, and Abdul Ghaffar2

1Department of Commerce and Finance, Government College University Lahore, Pakistan

2Lahore School of Accountancy and Finance, The University of Lahore, Pakistan

ABSTRACT

The current study aimed to unravel the factors that influence tax evasion behaviors among different income groups in Pakistan. The study used a robust multiple regression analysis to examine the complex phenomena of tax evasion and its compliance determinants. Furthermore, it also shed light on the complex relationship of economic, cognitive, and systemic factors. This study analyzed the data of 553 respondents collected through a structured questionnaire to explore the interplay between complexity, fairness perceptions, financial literacy, and access to financial services in the tax evasion context of Pakistan. Findings showed that low-income people in Pakistan are more vulnerable to tax evasion as well as they are more likely to be non-compliant than the high-income group. Additionally, the findings have significant implications for policymakers, providing a roadmap to increase tax compliance by simplifying tax regulations, promoting fairness, and investing in financial literacy programs. Such literacy would be helpful to improve fiscal health, increase voluntary compliance, and strengthen the economic and social development in the country. The current study provided actionable strategies to tackle tax evasion, leading to a more transparent and prosperous tax environment in Pakistan.

Keywords : : financial literacy, tax evasion, tax system complexity

JEL Codes: H26, H31, D91, D141. INTRODUCTION

Tax evasion is a global problem that considerably challenges collecting revenues and hampers the socioeconomic growth. Similarly, Pakistan faces several fiscal issues, especially tax collection problems (Kamal, 2019). Therefore, understanding how tax evasion grows from different socioeconomic levels and factors is crucial.

It is common in many countries, including Pakistan, that people want to avail government services and facilities, however, do not want to pay taxes (Tanzi & Zee, 2001). Tax avoidance and tax evasion are two common ways that people use to reduce their tax liability. According to the Royal Commission on the Taxation UK, tax avoidance refers to any action through which a person organizes their affairs in a manner that reduces their tax liability compared to what it would have been without the arrangement (Prest, 1956).

Tax avoidance involves legally reducing tax liabilities using tactics and loopholes in the tax system. Transactions are executed to minimize payable taxes; in certain instances, legislators may encourage tax avoidance with varying intentions. Tax avoidance is considered legal since it adheres to existing laws and regulations. It is different from fraud, deception, false representation, and other illegal practices. Tax evasion, however, usually occurs when the law is vague and must be interpreted and applied at the discretion of tax authorities (Brune et al., 2019).

The current study aimed to identify the underlying drivers of tax evasion practices in Pakistan by examining factors, such as complexity, perceptions of fairness, financial literacy, and access to formal financial institutions (Prichard et al., 2019). It also attempted to explain how these factors impact individuals' tax behavior in different income groups of Pakistan (Awan & Hannan, 2014). This is because understanding the dynamics of tax evasion across various socioeconomic groups is essential to formulate effective policy interventions (Jajja & Bhatti, 2022). It would also explore tax evasion practices between different income groups and how income inequality contributes to tax evasion (Vržina & Luković, 2023).

This study integrated multiple regression modeling and questionnaire to achieve its research objectives (Ghazo et al., 2021). The questionnaire was designed to collect respondents' opinions about tax evasion and compliance (McGee et al., 2016).

Objectives

This study sought to achieve two important research objectives mentioned as follows:

- To explore the determinant of tax evasion behavior in Pakistan

- To shed light on how such behavior exists in different income groups

Literature Review

The complex phenomenon of tax evasion has various and far-reaching effects on economies. Therefore, researchers studied this issue from economic, ethical, and sociological perspectives. According to Levi and Suddle (1989), tax evasion is any action that reduces, avoids, or defers tax liability and may lead to penalties for those found guilty. Literature also highlighted the need to understand tax evasion phenomenon since it affects revenue collection (Alstadsæter et al., 2022; Kar & Banerjee, 2018).

Researchers also explored the causes of tax evasion in many nations and highlighted the factors affecting people's decisions to evade taxes. Early on, Allingham and Sandmo (1972) and Mirrlees (1971) provided theoretical foundations of tax evasion, and Yitzhaki (1974) further explained the connection between tax evasion and penalty rates. In contrast, Górecki and Letki (2021) found key factors of tax evasion and proposed various solutions. Similarly, Ibrahim et al. (2023) explained why social and moral changes are needed to reduce tax evasion. Tanzi (1983) described the role of shadow economy in tax evasion as well as the use of cash transactions to conceal taxes. In the same way, other authors also discussed some additional forces that play a crucial role in tax evasion. These forces include education level, guilt, humiliation, corruption, and informal sectors (De Simone et al., 2020).

Earlier studies conducted on tax evasion revealed that ethical factors also contribute to tax evasion practices. For instance McGee (2006) analyzed the moral aspect of tax evasion and discovered that it might be justified in certain circumstances. Carvalho and Ávila (2022) examined the impact of tax evasion and tax avoidance on the economic growth of a country. Van Dunem and Arndt (2009) discovered certain difficulties that developing nations face in their tax systems. These include high tax rates, corruption, and ineffective tax administration.

Research from various countries, including Iran (Samadi & Tabande, 2013), India (Srivastava et al., 2018), and Nigeria (Nnenna, 2016) further reinforces the belief that these issues are dominant worldwide. Alm et al. (2009) highlighted that law enforcement and punishment strategies help to prevent tax evasion through deterrence. Meanwhile, Hanlon and Heitzman (2010) studied how the complexity of financial reporting facilitates corporate tax evasion. Furthermore, comparative cross-country studies on tax evasion also provided practical insights into worldwide tax evasion patterns. This indicates that a linkage between the higher level of corruption leads towards severe tax evasion issues. Allingham and Sandmo (1972) explained how tax evasion affects the government's revenue and fiscal policy and highlighted that a rise in tax evasion increases the tax rate, ultimately affecting growth.

Tax Evasion in Pakistan: Magnitude and Implications

The economy of Pakistan encounters various challenges, including stability and fiscal problems, mainly due to increased tax evasion practices (Kamal, 2019). The persistently low tax-to-GDP ratio indicates an ineffective capability to raise government revenues in order to fund government spending, which also hinders public services and infrastructure programs (Cyan et al., 2016). Resultantly, development programs and poverty alleviation efforts are jeopardized.

The consequences of tax evasion are not just fiscal; it increases income inequality on a large scale (Khan & Padda, 2021). Low-income groups bear the heavy burden of taxes, whereas the wealthy find ways to avoid paying taxes. Such an unequal tax burden increases the income gap and causes socioeconomic inequalities, making difficult to achieve equity within society. The scale of tax evasion in Pakistan also questions governance and public trust. When the majority of a country's population evades tax payments, people tend to have less confidence in the government and tax administration's competency (Cyan et al., 2016).

The perception that some persons and businesses are evading taxes fosters a sense of unfairness and erodes taxpayers' willingness to comply voluntarily. It also reduces tax collection and hinders the government's ability to invest in key sectors, such as education, healthcare, and infrastructure (Hassan et al., 2021). Insufficient revenue collection for key sectors and essential services may further increase poverty and deter the social mobility of low-income groups. Besides the financial consequences of tax evasion, it fosters a culture of non-compliance as well as a perception of unfairness among different income groups. According to Hassan et al. (2021), the belief that tax evasion is a normal behavior and goes unpunished may encourage more people and companies to violate the law and evade taxes. It may fuel-up tax evasion behavior and make the financial situation of the country more difficult by lowering tax revenue.

Determinants of Tax Evasion in Pakistan

There are various psychological, social, institutional, and economic factors that may affect tax evasion behavior. Furthermore, researchers have also identified different key factors that influence the compliance decisions of people (Alm, 2012; Luttmer & Singhal, 2014). The economic conditions, complex tax laws, and increased tax rates encourage individuals to evade taxes. People and firms might use tax evasion as a survival strategy during financially challenging periods (Bahl, 2017). It is also highlighted that people who try to retain more of their income minimize their tax liability, especially during high tax rates, as it provides them more incentives through tax evasion. Weaknesses in tax enforcement mechanisms and persistent corruption in Pakistan create a conducive environment to evade tax (Jajja & Bhatti, 2022). Poor tax administration, insufficient surveillance, and corruption within government institutions damage public trust in tax system, decreasing compliance among taxpayers who perceive unfairness.

Social norms and the perceived prevalence of tax evasion among peers significantly influence compliance decisions (Al-Rahamneh & Bidin, 2022). A culture of tax compliance and social disapproval of tax evasion may promote responsible taxpayer behavior. The complexity of tax system also feeds tax evasion behavior (Jajja & Bhatti, 2022), and a difficult tax system may create hinderances in understanding tax regulations, accidentally encouraging non-compliance tax behavior. In Pakistan, cultural factors also affect tax evasion behavior (Jajja & Bhatti, 2022). Moreover, fairness perceptions of tax system, including public services delivery in exchange for taxes paid, also influence taxpayers' willingness to comply with tax laws. Similarly, psychological factors play a significant role in shaping the tax behaviors of individuals, for instance, risk perception and attitudes of taxpayers (Hasseldine & Bebbington, 1991). Some individuals are non-compliant with tax laws and evade payable taxes because they may perceive tax evasion as a low-risk activity. On the other hand, some risk-averse individuals pay their taxes on time to avoid legal trouble if they perceive it as a high-risk activity.

Dynamics of Tax Evasion Among Different Income Groups

As discussed above, it is crucial to understand cultural, social, and other factors that lead towards differences in tax evasion behavior among various income groups in Pakistan. It is also important to formulate appropriate tax policies and address tax compliance problems in the context of Pakistan. Previous literature suggests that different income groups show different behaviors, and these varying behaviors are influenced by multiple economic and social factors (Khan & Ahmad, 2014). Furthermore, literature also indicates that high-income groups use more sophisticated tax planning techniques to minimize tax liability since these individuals tend to have more resources. High-income groups utilize tax exemption and deduction tactics and exploit tax loopholes to effectively lower their tax liability (Kangave et al., 2016). This is because, high-income groups have more resources and access to professional tax consultants who help them plan tax strategies in a way that minimizes tax liability and makes it difficult for authorities to find evidence of tax evasion (Bin-Nashwan et al., 2020).

In contrast, middle-income and low-income groups usually find it hard to fulfill complex tax laws; they might not comply due to their perception of the unfair tax system. Motivation to comply would also decline if they perceive that their contribution is not utilized fairly to provide public goods and services at large (Khan & Ahmad, 2014).

It is equally true that the low-income bracket's knowledge of tax systems and filing compliance are negatively affected by the level of financial literacy and availability of financial services (Nnenna, 2016). Their lack of understanding of tax systems, access to financial services, and compliance to tax laws makes it increasingly more challenging to understand tax regulations. Due to the lack of financial inclusion, some of the people in this bracket may be more prone to engaging in illicit activities, such as greater tax evasion. It is also assumed that some people from lower brackets of income view tax evasion through different lenses. For some, it may be a means to survive financial hardships as well as tax avoidance can be a response to a lack of confidence in government's capacity to utilize tax revenue for societal good (Al-Rahamneh & Bidin, 2022). Beyond financial problems, tax evasion goes hand-in-hand with socio-economic development challenges. Thus, the current study focused on the deeper dimensions of tax evasion practices which presents challenges for governance, economic development, and social cohesion in Pakistan. It is crucial to focus on specific ways through which tax evasion occurs. Additionally, it is also important to analyze its effects on different income classes and institutional, economic, and psychological determinants of the tax paying attitude.

Theoretical Background

The current study combined several traditional theories to determine the complicated issue of tax evasion. Furthermore, it also discussed the impact of financial knowledge, complexity, and perceived fairness of tax system on tax compliance behavior of different income groups in Pakistan. It used the "Theory of Planned Behavior", which notes that people's actions are shaped by their norms, attitudes, and perceived control over behavior (Ajzen, 1991). If taxpayers see the tax system as fair and clear, they are more likely to meet their tax responsibilities (Castañeda, 2024). Additionally, the study referenced behavioral economics, bounded rationality, and prospect theory, which suggested that limited thinking and views on risks may lead people to choose short-term benefits of tax evasion over long-term risks (Djajanti, 2020). Additionally, behavioral finance theory points out that having good financial knowledge is important to pay taxes. Those with better financial skills are less likely to evade taxes since they understand their tax duties and the risks of not complying (Djajanti, 2020). The current research merged these significant theories to create a broader view of what drives tax evasion in Pakistan and provided practical suggestions to improve tax compliance in that setting.

Methodology

The current study utilized a close-ended questionnaire to collect primary data from 553 respondents. The selection of sample size followed statistical principles, such that the data gathered would be adequate for regression analysis and its expected results. With respect to the study conducted by Lakens (2022), it is a better practice to collect a sample that is at least ten times the value of the items in the questionnaire. This method adds value to the reliability of findings and the validity of research as a whole. The survey questionnaire was administered face to face as well as through the Internet, so that all different types of respondents are considered for better outcomes (Regmi et al., 2017).

Convenience sampling allowed the collection of responses from all relevant income strata which is a great need for nuanced and detailed analysis of tax evasion behaviour. This sampling strategy allowed to gather perceptions from a large number of participants, enabling a more in-depth analysis of tax compliance determinants (Gioacchino & Patriarca, 2017).

The respondents of this study comprised professionals, employed and entrepreneurs from different fields. The diversity in occupation and income greatly enhanced the relevance of the findings itself.

Model Equation

The binary logistic regression model to analyze tax evasion behavior among different income groups in Pakistan can be represented as follows:

TE = β0 + β1IG2 + β2IG3 + β3CTS + β4PF + β5FL + β6AFFS + ε

where:

- TE = Tax Evasion

- β0, β1, β2, β3, β4, β5, and β6 are the coefficients to be estimated

- IG2 and IG3 are dummy variables representing the middle-income and low-income groups, respectively

- CTS, PF, and FL are continuous independent variables

- AFFS is a binary independent variable

| Variable | Definition | Measurement |

|---|---|---|

| Tax Evasion (TE) | A binary variable (0 or 1) indicates tax evasion behavior. | Respondents were asked whether they filed their tax returns regularly. |

| Income Group (IG) | A categorical variable representing income groups. - IG2: Middle-income group (1 if the individual belongs to this group, 0 otherwise). - IG3: Low-income group (1 if the individual belongs to this group, 0 otherwise). |

The income group was measured as a categorical variable, and respondents were selected from income categories 50k–100k, 101k–200k, and above 200k. |

| Complexity of Tax System (CTS) | A continuous variable representing the tax system's perceived complexity for each income group. | The perceived complexity of the tax system was measured on a 5-point Likert scale (Very Poor to Very Good). |

| Perception of Fairness (PF) | A continuous variable representing the tax system's perceived fairness for each income group. | Perception of fairness was measured using a Likert scale. |

| Financial Literacy (FL) | A continuous variable representing the level of financial literacy for each income group. | Financial literacy was assessed through three questions (Not Fair at all to Completely Fair). |

| Access to Formal Financial Services (AFFS) | A binary variable (0 or 1) indicating each income group's access to formal financial services. | Respondents were asked whether they had access to formal financial services, such as a bank account or credit card. A response of "Yes" was coded as "1", and "No" was coded as "0". |

Results and Discussion

Descriptive Statistics

The participants in the current study were diverse in genders, with 55% identified as men and 45% as women. Notably, no respondents selected "Other" or preferred not to answer their gender. Regarding age distribution, most participants, comprising 35% of the sample, fell within the age range of 30-40 years, indicating a relatively balanced representation across different age groups. Meanwhile, 30% of participants were 20-30 years old, showing a significant proportion of younger individuals engaged in the study. Additionally, 20% of respondents were between 40 and 50 years of age, while 15% were 50 or above.

Regarding marital status, half of the participants (50%) were married, while 45% were unmarried. Interestingly, 5% of the respondents preferred not to disclose their marital status. Approximately, 40% of the participants had completed their Master's degree, making it the most common educational attainment among respondents. Moreover, 25% of the participants had an M.Phil. or a higher degree, reflecting many individuals with advanced educational backgrounds. Meanwhile, 20% had completed graduation and the remaining 15% held other levels of education not explicitly listed in the questionnaire (see Appendix – I).

The data collected from participants' responses provided insights into their perceptions of Pakistan's tax system, particularly regarding their understanding and fairness assessments.

Perceptions of the Tax System

In terms of occupation, the study's participant pool represented various fields. The two most common occupations were "teacher" and "web and IT," comprising 15% of the respondents. Additionally, various professions were observed among the participants including engineers, healthcare professionals, lawyers, business owners, financial analysts, and bankers, each constituting 5% to 15% of the sample. It is worth noting that 15% of the participants preferred not to disclose their occupations. Lastly, the study explored the participants' monthly incomes. Results revealed that the most significant percentage (30%) fell within the monthly income range of PKR 75,000 to PKR 100,000. Additionally, 25% of the respondents had a monthly income between PKR 50,000 and PKR 75,000, while 20% reported earnings above PKR 100,000 monthly. On the other hand, 20% of the participants had a lower monthly income, below PKR 50,000.

Table 2 Perceptions of the Tax System (Understanding)| Very Good | Good | Average | Poor | Very Poor | Total |

|---|---|---|---|---|---|

| 15% | 30% | 35% | 15% | 5% | 100% |

Results showed that different participant perspectives existed about understanding the tax system. Only 5% of respondents ranked their comprehension as "very poor", indicating confusion or a lack of familiarity with the tax system. Another 15% of the respondents stated that their understanding was "poor", indicating that they needed to comprehend better how taxes work. Moreover, 35% of participants said that their understanding was "average", indicating a modest degree of knowledge with room for improvement. Overall, 30% of those surveyed claimed to know the topic "well", indicating that they had an in-depth understanding of the tax code. Approximately, 15% of participants achieved a "very good" knowledge score, indicating that they had a high knowledge and ability regarding the tax system.

Table 3 Perceptions of the Tax System (Fairness)| Completely Fair | Very Fair | Fair | Slightly Fair | Not Fair at all | Total |

|---|---|---|---|---|---|

| 10% | 20% | 20% | 30% | 20% | 100% |

Results on the fairness of the tax system in Pakistan were highly diverse; 20% of participants viewed it as "not fair at all", expressing their discontent and concerns about it. The survey also indicated that 30% of respondents had some uncertainties about the system's fairness and that they believed it to be "slightly fair". However, 20% of respondents stated that their belief in the tax system was "fair", which indicates some disagreement. Additionally, 20% of respondents awarded the system a "very fair" grade, indicating a higher degree of confidence in its equity. Majority of the final group thought the tax system was fair, with 10% of participants rating it as "completely fair".

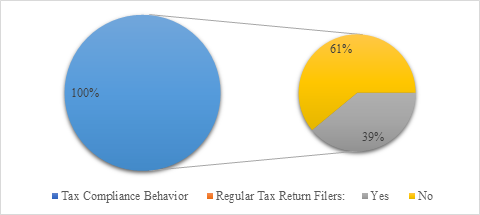

Tax Compliance Behavior

The data on tax compliance behavior revealed that 39% of respondents regularly filed their tax returns, demonstrating a commitment to fulfilling their tax obligations. However, a majority of 61% of participants reported not filing their tax returns regularly, which may indicate non-compliance, tax evasion, or lack of awareness about tax responsibilities. This finding raises concerns about tax collection and government revenue.

Factors Influencing Tax ComplianceData revealed that most participants (80%) complied with tax regulations primarily due to the "legal obligation" to file tax returns. Additionally, 60% of respondents cited the "fear of penalties" as a motivating factor for tax compliance. Around 35% of participants perceived tax filing as a means of "contribution to national development," demonstrating civic responsibility. Furthermore, 20% of respondents recognized the importance of tax compliance for "access to formal financial services".

Figure 1 Tax Compliance

Various other reasons indicated that individual motivations for tax compliance can be diverse. Overall, the study highlighted the importance of legal obligations and enforcement in encouraging tax compliance while suggesting potential avenues to promote tax compliance by emphasizing national development contributions and access to formal financial services.

Table 4 Factors Influencing Tax Compliance| Factors Influencing Tax Compliance | % |

|---|---|

| Legal Compliance | 80% |

| Fear of Penalties | 60% |

| Contribution to Nation Development | 35% |

| Access to Formal Financial Services | 20% |

| Others | 20% |

The data showed varying degrees of tax compliance among participants. Only 15% of respondents reported being "fully compliant" with tax regulations, indicating a high adherence to tax obligations. Another 25% stated they were "mostly compliant", implying a relatively good level of tax compliance with occasional deviations. A smaller proportion of 15% reported being "partially compliant", suggesting that they comply with tax regulations to some extent, however, not consistently. However, a concerning finding was that 5% of participants admitted to being "rarely compliant", indicating infrequent tax compliance. Most respondents (40%) were identified as "non-compliants", indicating that many people do not abide by tax laws. This conclusion highlights the need for focused interventions and tactics to increase overall tax compliance rates. Furthermore, it also raises significant questions about tax enforcement and the efficacy of compliance initiatives.

Table 5 Compliance with Tax Regulation| Overall Compliance with Tax Regulation | % |

|---|---|

| Fully Compliant | 15% |

| Mostly Compliant | 25% |

| Partially Compliant | 15% |

| Rarely Compliant | 05% |

| Non-Compliant | 40% |

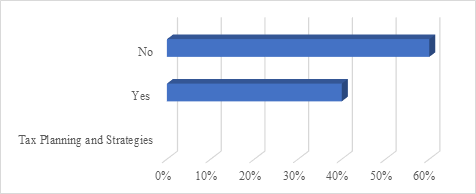

Tax Planning and Strategies

According to the evidence on tax tactics and preparation, 40% of the participants said that they used tax methods to reduce their tax obligations. Approximately, 60% of people still do not use any tax planning strategies. About 40% of those who use tax planning claimed to benefit from tax deductions and exemptions, and a similar percentage stated that they invested in financial goods that reduced their tax burden. Additionally, a few people reported shifting income to shady sources and using vague tax preparation techniques. These results underlined how crucial tax planning strategies are to lower tax liabilities and recommended that people use various methods to improve their tax status.

Figure 2Tax Planning

Additional research into the particular informal channels used as well as other tactics employed by participants may offer insightful information about the behavior of taxpayers and help policymakers develop more practical tax planning incentives and measures

Financial Literacy and Access to Formal Financial Services

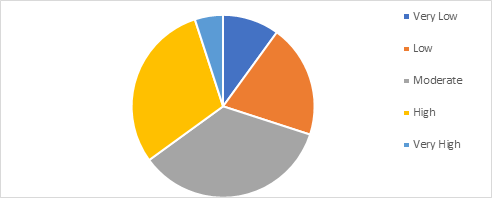

Empirical evidence on financial literacy and access to formal financial services revealed useful insights into the participants' financial awareness and access to financial institutions. Around 10% of respondents reported having a "very low" level of financial literacy, while 20% indicated a "low" level. The majority (35%) fell into the "moderate" financial literacy category and 30% demonstrated a "high" level, with only 5% having a "very high" level of financial literacy.

Figure 3Level of Financial Literacy

A certain percentage (75%) claimed to have access to formal financial services in comparison to 25% of respondents who reported otherwise. These findings underscore the importance to enhance financial education in order to ensure that individuals may effectively utilize formal systems of finance for economic development and financial decision-making. Financial education enables the individuals to better respond to economic challenges and aids in the unearthing of new market opportunities as well as tax issues.

Multiple Regression Results

The multiple regression analysis yields significant insights into the determinants of tax evasion behavior across income groups in Pakistan. The results reveal a pronounced pattern among low-income individuals (IG3), who demonstrate a significantly higher propensity for tax evasion compared to the high-income reference group (IG1) (Khan et al., 2024). This finding suggests an inverse relationship between income level and tax compliance, contrary to conventional assumptions about resource availability and evasion capacity. The observed behavior among low-income respondents may stem from perceptions of reduced audit risk, as they might anticipate less scrutiny from tax authorities relative to their higher-income counterparts. Meanwhile, the non-significant difference among high-income groups indicates that while these individuals possess greater resources for sophisticated tax planning, they may be equally likely to engage in evasion behaviors when opportunities arise, albeit through different mechanisms.

Table 6 Regression Results| Variable | Coefficient | Std. Error | t-value | p-value |

|---|---|---|---|---|

| Intercept | -0.203 | 0.072 | -2.82 | 0.005 |

| IG1 (High-income group) | 0.045 | 0.041 | 1.102 | 0.271 |

| IG2 (Middle-income group) | -0.086 | 0.045 | -1.91 | 0.057 |

| IG3 (Low-income group) | 0.129 | 0.053 | 2.431 | 0.016 |

| The Complexity of the Tax System | 0.204 | 0.081 | 2.507 | 0.013 |

| Perception of Fairness | 0.321 | 0.076 | 4.228 | 0.000 |

| Financial Literacy | 0.179 | 0.067 | 2.683 | 0.008 |

| Access to Formal Financial Services | 0.091 | 0.042 | 2.157 | 0.032 |

| R-squared | 0.356 | |||

| Adjusted R-squared | 0.347 |

Second, perceptions of tax system complexity significantly influence compliance behavior (Akitoby, 2018). The strong positive coefficient for the complexity of tax system variable indicates that taxpayers who perceive greater complexity in tax regulations demonstrate higher evasion tendencies. Complex systems create ambiguity in understanding obligations, potentially leading to unintentional non-compliance or deliberate misreporting.

Third, attitudes toward systemic fairness substantially impact compliance (Akitoby, 2018). The positive coefficient for perception of fairness reveals that taxpayers who view the system as equitable demonstrate greater voluntary compliance. This fairness perception fosters a sense of civic obligation and reduces evasion motivations.

Furthermore, financial literacy emerges as a key compliance factor. Financially literate individuals better understand both the penalties for evasion and benefits of compliance, making them more likely to fulfill obligations (Górecki & Letki, 2021). Finally, access to formal financial services significantly reduces evasion (Awan & Hannan, 2014). The negative coefficient for access to formal financial services suggests that banking integration improves compliance through enhanced reporting mechanisms and reduced transaction costs for legitimate tax payments.

Conclusion

The current study offered an extensive explanation of tax evasion tendencies amongst differing income levels in Pakistan. The study revealed that tax evasion is more prominent in low-income individuals (IG3) as opposed to other income groups (IG1). These outcomes are consistent with past studies (Alstadsæter et al., 2022) which indicate that the financial situation of lower-income groups is what drives them towards tax avoidance and non-compliance of taxes. The research also revealed no significant differences in tax evasion behavior among high-income individuals. In contrast, this implies that middle-income groups are more compliant with laws and also displays a high level of self-restraint with regard to tax evasion. The study also highlighted that the concept of fairness in tax system is equally important in complying with taxes.

If people perceive the tax system as just, compliance levels significantly increase. Fairness perceptions correlate negatively with tax evasion (Górecki & Letki, 2021), and so, if perception of the tax system is considered fair, people tend to abide by the rules. People are more likely to follow the rules when they feel something is fair.

Additionally, it was also noticed that the more people know about finances, the less likely they are to evade taxes. People who understand financial matters know that tax evasion may lead to trouble later on and are more likely to play by the rules (Erard & Feinstein, 1994). Lastly, access to formal financial services emerged as an essential factor in encouraging tax compliance. Individuals having access to formal financial services are less likely to engage in tax evasion, as formal channels make tax payments easier and more transparent (Akitoby, 2018).

Policy Suggestions

Empirical evidence suggests that low-income groups (IG3) are more prone to tax evasion. Therefore, government and policymakers should pay special attention to helping lower-income individuals comply with tax rules. The policy should include a simple tax filing system and offer tax credits and financial assistance to reduce or offset tax liabilities. Tax system should be made less confusing and straightforward. The policymakers should establish independent committees that would build trust among taxpayers and foster voluntary compliance.

Investing in financial education focusing on tax obligations, financial planning, and long-term savings could be a game-changer. When people understand money better, they follow the rules, including paying taxes (Nnenna, 2016). Policymakers should work to expand access to formal financial services in remote or underserved regions by incentivizing banks and financial institutions in order to open branches in these areas. Encouraging formal financial services for tax payments may make the process smoother. Additionally, integrating tax payment options into the existing mobile banking platforms could make tax compliance easier for those in areas with limited access to traditional banking services.

CONFLICT OF INTEREST

TThe authors of the manuscript have no financial or non-financial conflict of interest in the subject matter or materials discussed in this manuscript.

DATA AVAILABILITY STATEMENT

The data associated with this study is not available due to ethical, legal, or commercial restrictions. Only Coded data can be provided on request.

FUNDING DETAILS

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.