Shahid Mahmood1, Muhammad Adnan Ali1, Ahsan Riaz1*, Nimra Riaz1, and Marium Azad2

1Government College University, Faisalabad, Pakistan

2National University of Modern Language, Pakistan

* Corresponding Author: [email protected]

Commercial banks are involved in uncontrolled credit risk management that negatively affects their sustainable banking performance. Many guidelines, strategies, and judgments have been made, such as the Basel Accords, to control these issues and adequately manage their lending and borrowing policies. This study aims to analyse the impact of credit risk management on the sustainable performance of commercial banks. For this purpose, secondary panel data was collected from the annual financial reports of 27 commercial banks out of the 31 listed on the Pakistan Stock Exchange (PSX) for the period 2017-2021. E-views 10 software was applied to perform descriptive correlation and multiple regression analyses. In the current study’s model, credit risk management proxies, return on assets (ROA), return on equity (ROE), and net interest margin (NIM) were employed as dependent variables. At the same time, capital adequacy ratio (CAR), loan and advances (LA), non-performing loans (NPL) ratio, market profit opportunity (MPO), and bank liquidity (BL) were employed as independent variables. The study concludes that bank liquidity has a significant positive relationship with bank performance. Comparably, capital adequacy ratio, non-performing loans, bank liquidity, market profit opportunity, and loan and advances harm the sustainable performance of commercial banks. The research suggests that implementing stricter policies and strategies, such as the regulation of customer loans, is required to control these issues.

Keywords: bank liquidity, banking sector, commercial banks, capital adequacy ratio, credit risk management, economy, interest rate spread, loan and advances, profitability, market profit opportunity, non-performing loan

JEL Codes: G21, G21, C23, C33

The banking sector is the backbone of any developing country. Pakistan's banking infrastructure plays a crucial and supportive role in fostering the economic growth and sustainability of the financial sector (Shafiq et al., 2023). According to 'The Pakistan Financial Institutions Ordinance 1962,' banks are tasked with collecting and depositing money, making investments, providing services, and being repayable. Many significant changes have been made in Pakistan's banking sector over the last few years by incorporating different types of corporate configurations, such as investment banks (IBs), conventional banks (CBs), Islamic banks (IBs), foreign banks (FBs), and development banks (DBS). With these diverse banking configurations, technological innovations have intensified competition, resulting in enhanced performance(Anees et al., 2023).

According to the list issued by the State Bank of Pakistan in 2022, there are twenty-two (22) local private banks, five (5) public limited banks, eleven (11) microfinance banks, one (1) development bank, four (4) foreign banks, and five (5) Islamic banks operating in Pakistan. All these different types of banks actively contribute to the country's development. Pakistan's financial sector, which includes commercial banks, the Pakistan Stock Exchange (PSX), and insurance companies, are sources of national savings, financing, investment, and economic growth (Nazeer et al., 2022).

Pakistan's banking sector faces numerous challenges, including capital shortages, an uncertain political environment, and socioeconomic uncertainties. Moreover, many other risk factors affect not only the financial sector but also non-financial sectors, such as market risk, liquidity risk, capital adequacy risk, loan and advances, credit risk, foreign exchange/legal risk, and loan loss provisions. These factors create a barrier to the development and sustainable growth of the banking system. Pakistan's commercial banks have adopted the Tier II system, and one of its primary functions is to meet the requirements for economic development (Mushafiq et al., 2023; Rafique et al., 2020).

In 1948, Pakistan established its central bank, whose primary function is to monitor all the activities related to financial institutions. The State Bank of Pakistan (SBP) Ordinance, 1962 and the State Bank of Pakistan Act, 1956 granted SBP an autonomous status, and it became the centralised authority responsible for resolving disputes among financial institutions. SBP issues all the strategies, policies, and credit structure guidelines to the financial sector to ensure the sustainability of financial services. It follows the Basel Accords guidelines/rules and strictly imposes checks and balances on all the commercial banks' activities regarding credit risk management (CRM), non-performing loans (NPLs), loan procedure, and credit strategies, which contributes significantly to the growth of the banking sector (Khan, 2023).

Commercial banks are financial institutions that aim to generate maximum profit under minimum risk. For this purpose, commercial banks deposit money from the public at a low-interest rate and provide loans to those in need at a higher rate. The difference between the low and high rates becomes the profit of the banks. A deposit is considered a bank liability to be paid by the bank to the depositor. Conversely, a loan is considered an income source that is expected to generate profit after collecting the interest and principal amount from the bank. Risk remains inevitable for both borrowers and lenders.

Consequently, banks have diversified their profit-making strategies by venturing into new products and services, such as providing goodwill on instalments, business-to-business market, payment of utility bills, credit card facilities, ATMs, mortgages, and account aggregation (Cao et al., 2023).

The Basel Committee on Banking Supervision (BCBS) was established in December 1988 under the supervision of the central bank governor with the consent of 12 countries, including Germany, Switzerland, UK, USA, Canada, Sweden, Belgium, Germany, Italy, France, Japan, and Netherlands (BCBS, 2013). The main objective of this committee was to make strategic rules and regulatory frameworks through which the global financial crisis and risks may be reduced. Moreover, it aimed to facilitate international relationships among the banking sector and enhance its capital positions. (Quaglia, 2023).

Basel-II was introduced in 1997 to mitigate risk management, especially capital risk and risks in the banking sector. Basel-II introduced three guidelines. Firstly, the financial organisation must hold 8% of its total capital to keep saving for solvency in the market. Secondly, there would be a strong relationship between the supervisor and the bank to ease internal and external risk assessment. Thirdly, it emphasised the discipline of the market and the use of capital adequacy techniques. However, many changes were required after the banking sector's crisis in 2007-08 to sustain the capital and credit risk accuracy. Hence, Basel-III was introduced in 2009. It provided six objective points regarding leverage ratio, counterparty credit risk, capital requirements, liquidity ratio, capital conservation barrier, and counter-cyclical capital barrier (Grzeta et al., 2023).

Uncertainty and potential losses at any stage or time can disrupt business transactions, which is referred to as risk. There are two types of risk, namely systematic and unsystematic risk. Unsystematic risk is a type of risk that cannot be measured statistically; therefore, it can be mitigated through diverse techniques. On the other hand, risk management methods can quickly assess and minimise systematic risk. In the financial sector, there are different types of risks, including market risk, credit risk, portfolio risk, interest risk, operational risk, and some other kinds of risks. In the banking sector, risk can be identified through the annual financial statement analysis, examined by the branch manager, internal and external audit reports, physical assessment, and market view (Abdesslem et al., 2022).

Credit risk management (CRM) is a critical process undertaken by banks, particularly commercial banks and other financial institutions. The 5Cs structural tools, namely capital, capacity, collateral, condition, and character, are essential to this process. Before loan approval, financial institutions such as commercial banks conduct qualitative and quantitative assessments of the loan structure. The evaluation committee of banks conducts a systematic analysis of the borrower's credibility and creditworthiness with the intention to determine their ability to repay the principal amount and interest within the specified time. According to Dimitrov and van Wijnbergen (2023), lenders use a multifaceted process to evaluate and quantify various aspects of the borrower's financial profile, assigning each component a corresponding score. Initially, the borrowers convey their historical standing and degree of fidelity to the creditor concerning the timely reimbursement of debts. In the event of delayed payment or default, it is recommended to withhold approval for subsequent loans.

Conversely, a favourable historical standing and rapport with the lender serve as positive indicators for approving subsequent loan sums. Capacity is a metric utilised to assess a borrower's ability or aptitude in order to fulfil their loan obligation within the designated timeframe. This includes evaluating the borrower's debt-to-income ratio (DTI) and their monthly income or profit. Moreover, capacity also refers to the borrower's employment type, whether contractual or permanent, with a preference for regular employees over contractual ones. Thirdly, the capital gauge computes the borrower's overall net worth, encompassing their earnings invested in a commercial enterprise and their outstanding debt. The fourth factor to consider in lending is the degree of emphasis the lender places on collateral, which refers to the security provided by the borrower in the form of pledged assets to protect against bankruptcy. The fifth condition requires borrowers to analyse a situation based on two factors, namely the borrower's purpose and objective, which comprise the internal factor, while the external factor exerts significant influence over prospects.

An additional model, referred to as ‘CAMEL’, outlines five distinct components, namely asset quality, management role, liquidity ratio, earnings, and capital adequacy ratio (CAR). The central bank of a given nation serves as the regulatory entity that oversees the operations of its constituent banks. Through the analysis of annual financial reports, the central bank assesses the performance of these banks, identifying their strengths, weaknesses, opportunities, and threats. The United States of America and the National Credit Union Administration implemented the CAMEL parameters as a ratio system in 1987. Subsequently, BCBS incorporated these rating systems to evaluate other nations' CAMEL framework (Keqa, 2023). CAR is a regulatory requirement that mandates banks to maintain a certain level of capital or earnings retention to safeguard the interests of depositors and investors and to ensure the banks' financial stability. The ratio can be computed using the growth plan and economic milieu.

The asset quality parameter comprehensively describes the bank's current holdings, including loans, investments, cash reserves, government securities, and other assets. It is recommended that the bank should initiate the loan recovery process from the customer within 90 days. A bank's management team identifies, measures, and controls organisational risks. To manage credit risk, it is essential to identify it appropriately. The bank would then assess the risk through a sophisticated model, which would help assess the borrower's financial position. Many researchers use non-performing loans (NPL) as a proxy for credit risk management.

Along with numerous challenges and crises, Pakistan's banking system is facing alarming concerns regarding NPLs. The increase of branches in the banking sector has led to the number of NPLs escalating yearly. NPL to LA is decreased in the private sector as compared to the public sector (Naili & Lahrichi, 2022; Gjeci et al., 2023).

This research aims to recognise and assess the problem in Pakistan's commercial banks and provide empirical evidence. Some prior studies have stated the negative impact of NPL on sustainable bank performance. Conversely, some researchers investigated the positive impact of NPL on bank performance. The current study aims to investigate the effect of NPL on the sustainable performance of commercial banks operating in Pakistan.

The information available is very limited to answer these questions.

This section first discusses different management theories and their implications for credit risk management in the banking sector. It then moves the discussion to the variables of interest and how they affect the banks’ performance.

Agency theory states the relationship between the organisation's common shareholders (owners or principals) and agents (managers or employees). Principals hire agents to work and make decisions on their behalf in the organisation. The agents (managers) and principals (owners) are interested in a relationship where the owner wants to maximise the value of shares and profit. On the other hand, the agent wants incentives, such as salary increments, bonuses, house rent allowance, medical allowance, and conveyance allowance. When there is a conflict between the agents and principals, this is called the agency problem. Agency problem significantly impacts organisational performance, which produces agency cost. An increase in agency cost decreases the value of a firm (Chike and Ebere, 2023; Duho et al., 2023).

In the commercial banking sector, the managers perform tasks as agents of the organisation. Bank managers know about decision-making and are authoritative in making decisions. The top-level management formulates strategies, policies, rules, and regulations to mitigate risks, especially with respect to credit risk management. Moreover, the owner must bear all the risk. So, the agents utilise the owner's resources for decision-making without worrying about risk.

There are several tools which can help to overcome agency problems. The organisation's owner may announce rewards for loyal managers in the shape of shares in the organisation, thus providing better opportunities for promotion and job security. Therefore, the managers may make profitable decisions for enhanced organisational performance.

In 1952, portfolio theory was introduced by Markowitz. The main objective of this theory was to maximise the level of return by minimising the risk for the collection of investments. With time, Markowitz's portfolio theory became the modern portfolio theory. Markowitz famously said, "Do not put all the eggs in a single basket", which emphasises diversified business investments. So, if some investments fail, there may be a chance of profit from other investments. Later on, this theory faced criticism from various authors(Keqa, 2023; Musa & Nasieku, 2019; Mushafiq et al., 2023).

Furthermore, the post-modern portfolio theory (PMPT) was introduced using the beta and alpha coefficients to calculate risk and the expected return statistically. PMPT is the best calculation gauge for predicting risk and expected return in the future. 'Beta' is used to measure the market investment return, and 'alpha' is used to measure investment performance.

The crux of this theory states that investors are risk-averse. This theory suggests the loan portfolio strategic management concept, which helps avoid risk and enhance the bank's performance. For this purpose, the banks should combine different loan types carefully, maximising the returns. The diversification of loan portfolio practice is the best tool for maximising returns. The lending officer evaluates the weaknesses and strengths in the financial banking sector according to the future perspective. On the other hand, it must be securitised and sold before taking the capital (Khan et al., 2023).

Non-Performing Loans (NPLs) Affect Bank Performance

When a commercial bank cannot collect the expected amount from the borrower in the form of interest and principal amount within 90 days, it is called a non-performing loan or NPL. In other words, NPLs are also known as bad or impaired loans. Commercial banks consider these loans as risky assets, and they can significantly affect their performance. NPL is used by many researchers as a significantly strong indicator to identify the management’s approach regarding credit risk and its impact on bank performance. A bank's management should implement the proper guidelines of the State Bank of Pakistan and the Basel Accord with reference to risk (Khan et al., 2023; Akhter, 2023).

As postulated by some prior research, NPL and bank performance have a negative relationship (Syafrizal & Ilham, 2023). On the other hand, some researchers have stated a positive relationship between NPL and bank performance. The current study hypothesises that NPL has a negative impact on bank performance.

H1 = Non-performing loans (NPLs) have a negative effect on bank performance in Pakistan.

Capital Adequacy Ratio (CAR) Effect on Bank Performance

The capital adequacy ratio (CAR) is a key financial metric that measures a bank's ability to absorb potential losses arising from its operations and assets, particularly loans and investments. It is a critical aspect of bank regulation and supervision aimed at ensuring the stability and soundness of financial institutions. CAR determines the organisation's performance and is used to examine the strength of a financial organisation. Banks with adequate CAR can generally absorb the losses of expected risk, meet financial obligations, and provide sustainable shelter to avoid solvency. For an ideal financing structure, banks should use the combination of debt and equity, which would help them improve the values of common and preferred stock. Capital adequacy has two types. Tier I capital adequacy emphasises absorbing losses, while Tier II assures the safety of depositors by making such strategies which aim to avoid losses. The Pakistani banking system uses the Tire II type strategies, which obligate the bank to take an 8% reserve against the loan given to a borrower (Orden‐Cruz et al., 2022; Amissah & Opoku, 2023; Emmanuel et al., 2021).

The results of the past research show the positive effect of CAR on bank performance (Akbar, 2023). On the other hand, some researchers exhibited a negative relation between CAR and bank performance (Wahyuni et al., 2023). This study hypothesises that CAR negatively affects bank performance.

H2 = CAR has a negative effect on bank performance in Pakistan.

Loan and Advances (LA) Effect on Bank Performance

In commercial banks, loans and advances (LA) are the sources of income and are used for calculating the difference between the depositor’s amount and the borrower's amount (interest + principle). LA indicate bank liquidity. Liquidity is a very important determinant for banks, which helps to prevent them from becoming insolvent. To sustain the condition of liquidity, banks use strategic planning under deposit demand and time framework. Several studies show that LA positively affects the performance of commercial banks (Nguyen et al., 2023). On the other hand, some researchers have also investigated the negative effect of LA on bank performance (Uddin et al., 2023; Kolsi et al., 2023). This study hypothesises that LA has a negative effect on bank performance.

H3 = LA has a negative effect on bank performance in Pakistan.

Market Profit Opportunity (MPO) Effect on Bank Performance

Market profit opportunities or MPOs can have a significant effect on the performance of commercial banks. MPO refers to the potential for banks to generate profit by identifying and exploiting opportunities in the market. Opportunities can arise due to various factors, including changes in interest rates, economic conditions, customer behaviour, and regulatory changes. MPO indicates that the bank's performance and deposits play a vital role. With the increase in deposits, there is a better chance to increase profitability, as the transformation of deposits into loans and interest creates/marks the difference between depositors and borrowers (Proença et al., 2023). This study hypothesises that MPO negatively impacts the bank's performance.

H4= MPO has a negative effect on bank performance in Pakistan.

Bank Liquidity (BL) Effect on Bank Performance

Bank liquidity (BL) is vital in determining a commercial bank's overall performance and stability. It affects a bank's risk management capabilities, depositor confidence, funding costs, lending capacity, investment opportunities, regulatory compliance, market perception, stress resilience, and operational efficiency. Banks that balance short-term liquidity needs and long-term growth goals are better positioned to navigate the challenges and capitalise on the opportunities available in the financial landscape. BL is directly associated with the bank's performance; as the value of liquidity changes, it changes the sustainable performance of the bank. Many other factors bring changes in liquidity value that result in insolvency or failure of the bank. The better management of banks for the value of liquidity can bring positive changes in the value of this variable. Many researchers (Awaluddin et al., 2023; Zamore et al., 2023) have stated that BL significantly affects the sustainable performance of commercial banks. This study hypothesises that BL positively affects bank performance.

H5= BL has a positive effect on bank performance in Pakistan.

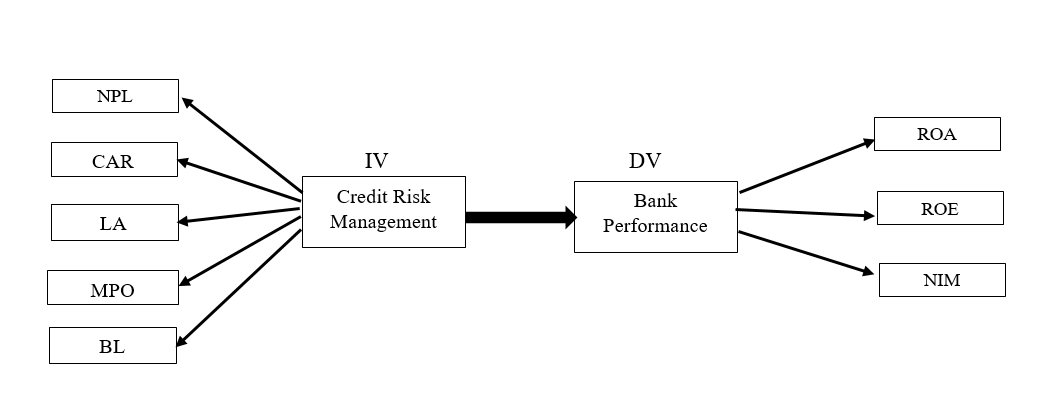

Figure 1

Theoretical Research Framework

This study aimed to identify and compare risk and credit risk and their impact on commercial banks operating in Pakistan. A total of 18 private banks were selected as samples for the period 2010-2020. The Generalised Method of Moments (GMM) model was used to analyse the data consisting of one dependent variable, namely return on assets (ROA) or profitability and two independent variables, namely non-performing loans or NPL and liquidity risk, along with three control variables including size, GDP, and inflation. The results manifested that NPLs have a significant negative effect on bank profitability, while liquidity risk positively affects sustainable bank performance.

Hersugond et al. (2021) described the impact of non-performing assets, insolvency risk, and capital adequacy ratio (CAR) on bank performance in Indonesia. They used bank age and bank size as control variables. Data was collected for the period 2015-2019. Markowitz's portfolio and agency theory were used to provide the theoretical background to the study. The results indicate that both CAR and NPL negatively affect bank performance. Conversely, the control variables of insolvency risk and bank size positively impact bank performance.

Sharma and Kaur (2021) studied the impact and relationship between profitability and non-performing loans through the enactment and management of credit risk in Indian public banks. The researchers took data for the years 2009-2019 and used the analysis of variance (ANOVA)to analyse the data. ROA and ROE were used as indicators of bank performance, market capitalisation was used as control variables, and NPL, CAR, and LR were used as indicators of CRM. The results showed that NPLs have a negative impact on ROA and ROE. The results further indicated that CAR has a positive impact on bank performance, while liquidity risk does not have a significant relationship with bank performance.

Another study investigated the relationship between the quality management of credit risk and financial sustainability in Nigerian banks. For this purpose, 12 banks were selected out of 14 listed deposit money banks (DMBS) in Nigeria. Secondary panel data (time series and cross-section) was collected for the period 2010-2019. As independent variables, CRM proxies were used, namely loan deposit ratio, non-performing loans, and assets growth percentage. Further, financial sustainability proxies were used, namely capital adequacy ratio and return on capital employed, along with bank size as control. After statistical analysis, the results exposed that CRM significantly and positively affects financial sustainability.

Furthermore, it was found that non-performing assets and capital adequacy negatively impact the bank performance indicators, namely ROA, ROE, and NIM. While insolvency risk significantly and positively affects bank performance. On the other hand, a Z-score was used to measure insolvency risk, which suggested that a higher Z-score would improve the banks’ sustainability.

Another research explored the listed commercial banks in Ghana. The results suggested that NPLs and LLP have a statistically significant but negative impact on bank performance. Further, the results also revealed a significant positive effect of CAR on bank performance. Moreover, it was found that bank size also has a positive effect on bank performance. Further, the researcher recommended properly utilising portfolio management's CAR. Increasing bank size helps to sustain healthy bank performance.

The current empirical study used a panel data framework to investigate the relationship and the impact of independent variables (NPL, CAR, LA, MPO, BL) on dependent variables (ROA, ROE, NIM). The analyses were descriptive and correlated with independent and dependent variables. Further, multiple regression analysis and the Eview-10 software program were used to analyse the panel data. All 31 commercial banks listed on the Pakistan Stock Exchange (PSX) formed the population of the study. Finally, 27 commercial banks were selected as a sample out of the total population. Data was collected through all the financial statements published by the banks annually. The data was collected using the following inclusion criteria for this study.

Descriptive Analysis

The table below shows that LA has the highest SD value, which is 0.1475. The difference between the highest and the lowest SD values of LA is 0.9. This variable's minimum ratio is 0.2296, while the maximum ratio reaches 1.1296. This result indicates that the LA ratio has greater diversification in the sample banks of our study. It also indicates that the quality of CRM fluctuates among the banks.

Table 2

Descriptive Statistics

|

Minimum |

Maximum |

Range |

Mean |

Std. Dev. |

N |

|

|

ROA |

-0.49 |

0.35 |

0.84 |

0.09 |

0.14 |

125 |

|

ROE |

-0.05 |

0.02 |

0.08 |

0.005 |

0.01 |

125 |

|

NIM |

0.01 |

0.04 |

0.04 |

0.03 |

0.01 |

125 |

|

BL |

0.46 |

0.86 |

0.39 |

0.73 |

0.08 |

125 |

|

CAR |

0.03 |

0.49 |

0.46 |

0.08 |

0.05 |

125 |

|

LA |

0.23 |

1.13 |

0.9 |

0.61 |

0.15 |

125 |

|

MPO |

0.64 |

0.97 |

0.32 |

0.929 |

0.04 |

125 |

|

NPL |

0.00 |

0.44 |

0.44 |

0.09 |

0.08 |

125 |

Correlation analysis was used to investigate the positive versus negative relationship, as well as the strength of the relationship (strong, weak, poor, or moderate), between the independent and dependent variables. Moreover, the analysis indicates the direction and nature of the relationship between the study variables. According to Gujarati (2009), the correlation coefficient should be less than 0.8, indicating no multicollinearity among independent variables.

In the above table, the value of (1.00) demonstrates that all independent variables (IVs) and dependent variables (DVs) are mutually correlated. As the value of all the independent variables is less than 0.8, there is no multicollinearity among them.

Furthermore, there is a weak and negative correlation of the bank performance indicator (ROA) with the credit risk indicators, namely CAR, LA, and NPL (with values of -0.197853, -0.357861, and -0.676680, respectively). Conversely, there is a weak but positive correlation of ROA with BL and MPO (with the values 0.149022 and 0.161580, respectively). It reveals that as the value of BL and MPO increases, ROA also increases.

As compared to ROA, ROE has a weak and negative correlation with credit risk indicators, namely NPL, CAR, and LA (with the values -0.687325, 0.094112, and -0.309009, respectively). It reveals that as the value of NPL, CAR, and LA increases, the value of bank profitability decreases. On the other hand, there is a positive but weak correlation of ROE with BL and MPO with bank profitability (with values of 0.030753 and0.065910, respectively). It indicates that there is a positive increase in bank profitability with an increase in MPO.

The net interest margin (NIM) has a weak but negative correlation with NPL, LA, and MPO (with values of -0.153022, -0.267567, and -0.411586, respectively). On the other hand, there is a positive but weak correlation of NIM with BL and CAR (with values of 0.245534 and0.198015, respectively). It indicates that with the increasing value of NPL, LA, and MPO, the value of NIM decreases. On the contrary, with the increasing value of BL and CAR, the value of NIM also increases.

Table 3

Correlation Matrix

|

ROA |

ROE |

NIM |

BL |

CAR |

LA |

MPO |

NPL |

|

|

ROA |

- |

|||||||

|

ROE |

0.72 |

- |

|

|

|

|

|

|

|

NIM |

0.58 |

0.60 |

- |

|

|

|

|

|

|

BL |

0.15 |

0.03 |

0.24 |

- |

|

|

|

|

|

CAR |

-0.20 |

-0.09 |

0.20 |

-0.33 |

- |

|

|

|

|

LA |

-0.36 |

-0.30 |

-0.15 |

-0.34 |

0.29 |

- |

|

|

|

MPO |

0.16 |

0.06 |

-0.27 |

0.34 |

-0.72 |

-0.23 |

- |

|

|

NPL |

-0.68 |

-0.69 |

-0.41 |

0.10 |

0.03 |

-0.08 |

-0.04 |

- |

Panel data is a combination of time series and cross-sectional data. Three main models are typically used to analyse panel data, namely the common effects model, the fixed-effects model, and the random-effects model.

Model I: ROAit = β0 + β1NPLit + β1CARit + β1LAit + β1MPOit + β1BLiteit

The coefficient of CAR, NPL, LA, and MPO variables is significant and negative (with the values -0.409994, -1.233196, -0.330898, and -0.562511, respectively). The results indicate that one unit change in CAR, NPL, LA, and MPO would result in -0.409994, -1.233196, -0.330898, and -0.562511 units decrease in ROA. It reflects that a higher CAR, NPL, LA, and MPO value would cause a decline in bank performance.

The impact of BL is significant and positive on ROA (with a value of 0.106614). A one-unit increase in BL would result in a 0.106614 unit increase in ROA, indicating that bank performance increases due to an increase in BL, which is more favourable for the smooth running of commercial banks.

In the table above, the t-test value of NPL, LA, and BL is less than (0.05), significantly affecting ROA. Thus, hypotheses H1, H3, and H5 are acceptable, while H2 and H4 are rejected as their values are more than the significant value (0.05). In regression analysis, R2 determines the percentage of variance (rate of change) due to the change in independent variables that affect dependent variables.

In the above table, the R2 value in Model 1 is (0.643113). The mean-variance change in ROA is (64.31%), which is due to the change in BL, CAR, LA, MPO, and NPL. The remaining change (35.63%) is due to other factors. Adjusted R2 is the shrinkage value of R2, which determines the closeness and goodness of fit of the data for the model. The higher the value of adjusted R2, the more fit the data. The adjusted R2 value is 0.628117, the shrinkage value to determine the model's goodness of data fit.

F-test (Fisher statistics) is used to identify the overall significance and goodness of fit of the model. An expected value is significant at a 5% level. In Model 1, the F-value is less than (0.05), which indicates that the overall model is significant and shows a strong relationship between IVs and DVs.

Model II: ROEit = β0 + β1NPLit + β1CARit + β1LAit + β1MPOit + β1BLiteit

The coefficients for CAR, LA, MPO, and NPL (with the values -0.861105, -0.013281, -0.052968, and -0.103614, respectively) show that these variables significantly and negatively affect ROE. It indicates that a 1%/one unit increase in CAR, LA, MPO, and NPL would result in (-0.861105, -0.013281, -0.052968, and -0.103614 units decrease in ROE. On the contrary, the coefficient for BL is significant and positive, with a value of 0.001142. It shows that a one-unit increase in BL would result in a 0.001142 unit increase in ROE. In the above table, the t-test value of NPL, LA, and MPO shows that these variables significantly affect ROE. Thus, hypotheses H1, H3, and H4 are accepted. While the t-test value of CAR and BL shows that these variables insignificantly affect ROE. Thus, hypotheses H2 and H5 are rejected.

R2 value (0.974136) indicates that the rate of change in ROE (97.41%) is based on the change in independent variables, while the remaining variance (2.59%) is due to another source. The adjusted R2 value is 0.966240, which depicts the total exact variation. On the other hand, the overall model is significant and suitable to fit, as the F-value is less than (0.05), the traditional value of significance.

Model III: NIMit = β0 + β1NPLit + β1CARit + β1LAit + β1MPOit + β1BLiteit

The coefficients for NPL, LA, and MPO (with the values -0.009528, -0.057486, and -0.050946, respectively) show that these variables significantly and negatively affect ROE. It indicates that a one-unit increase in NPL, LA, and MPO would result in -0.009528, -0.057486, and -0.050946 units decrease in ROE, respectively. On the contrary, the coefficients for BL and CAR are significant and positive (with values of 0.039715 and 0.017799). It indicates that a one-unit increase in BL and CAR would result in 0.039715 and 0.017799 units increase in ROE.

The t-test value of NPL, LA, MPO, and BL shows that these variables significantly affect NIM. Thus, hypotheses H1, H3, H4, and H5 are accepted. At the same time, the t-test value of CAR shows that these variables have an insignificant effect on NIM. Thus, hypothesis H2 is rejected.

R2 value (0.453414) indicates the rate of change in NIM (45.341%) based on the change in independent variables, namely BL, CAR, LA, MPO, and NPL. The remaining variance (54.66%) is due to other sources. The adjusted R2 value is 0.43448, and it is the total exact variation in NIM. The F-value is less than (0.05), which indicates that the overall model is significant.

Table 4

Regression Analysis Using Panel EGLS (Cross-section Random Effects)

Variable |

ROA (Model I) |

ROE (Model II) |

NIM (Model III) |

||||||||

|

Coeff. |

t-Stat |

Prob. |

Coeff. |

t-Stat |

Prob. |

Coeff. |

t-Stat |

Prob. |

|||

|

C |

0.87 |

2.65 |

0.01 |

0.07 |

4.54 |

0.00 |

0.08 |

4.03 |

0.00 |

||

|

BL |

0.11 |

1.73 |

0.05 |

0.001 |

0.26 |

0.33 |

0.04 |

5.37 |

0.00 |

||

|

CAR |

-0.41 |

-1.29 |

0.20 |

-0.66 |

-0.03 |

0.47 |

0.02 |

1.22 |

0.22 |

||

|

LA |

-0.33 |

-8.25 |

0.00 |

-0.01 |

-6.19 |

0.00 |

-0.01 |

-2.41 |

0.02 |

||

|

MPO |

-0.56 |

-1.63 |

0.10 |

-0.05 |

-3.16 |

0.002 |

-0.06 |

-3.83 |

0.00 |

||

|

NPL |

-1.2 |

-10.67 |

0.00 |

-0.10 |

-29.02 |

0.00 |

-0.05 |

-7.10 |

0.00 |

||

|

R2 |

0.64 |

F-Stats |

42.89 |

0.97 |

F-Stats |

123.38 |

0.45 |

F-Stats |

19.74 |

||

|

Adj. R2 |

0.63 |

Prob (F-stat) |

0.00 |

0.97 |

Prob (F-stat) |

0.00 |

0.43 |

Prob (F-stat) |

0.00 |

||

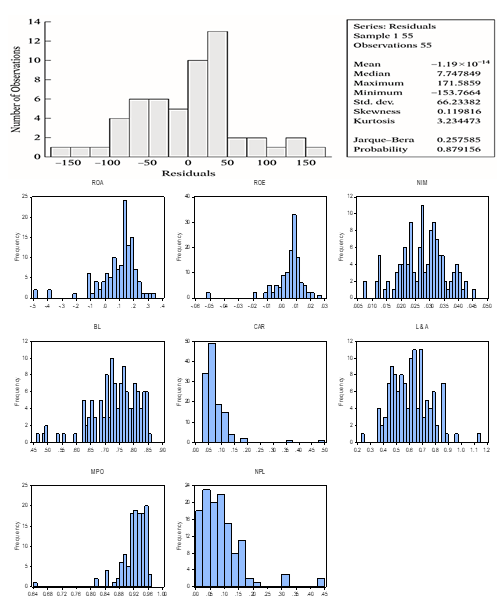

Normality test is widely used in statistics to identify if the data is normally distributed. It is also called the bell curve test or Gaussian curve. The rules of statistics allow us to convert non-normal data into normal to form a balanced or stable histogram and a bell-shaped curve, the mean. The median and mode are equal; moreover, it is symmetrical around the mean. The graph shows that each variable's mean, median, and mode are equal, indicating that the data is normally distributed. The value of Jarque Bera is also above 5%, indicating the normality of the data. The graphs of normality are shown below in Figure 2. Secondly, the probability value is less than 0.05, again indicating that the data is normally distributed. The value of skewness should be close to 1. Figure 2 shows that the skewed value is 0.07, which is highly acceptable. Similarly, the kurtosis value of 3.185 is more than the minimum value of 3.

Figure 2

Normal Distribution of Data

The commercial banking sector is pivotal in developing the economy and smooth, progressive running of the GDP. This study aimed to analyse and determine positive or negative effects on the relationship between credit risk management and banking operation and profitability performance indicators (ROA, ROE, NIM) using proxies (NPL, CAR, LA, BL, MPO). Based on the availability of data for the period 2017-2021, 27 commercial banks were selected out of the 31 operating in Pakistan. Panel data was collected (time series and cross-section) from the financial reports, and descriptive, correlation, and multiple regression analyses were used to describe/calculate the results.

The study concludes that the independent variables (NPL, CAR, LA, and MPO) have a negative impact on bank performance indicators (ROA, ROE, NIM). On the other hand, BL has a positive impact on bank performance.

As credit risk management indicators (NPL, CAR, LA, MPO) increase, bank performance decreases, potentially negatively impacting the smooth operation of Pakistan's economy. Thus, these variables must be controlled through proper management techniques to recover the interest and the principal amount within a given period.

Pakistan's lack of credit risk management has been deeply involved for the historical decade. Many reasons have been involved in this perspective. A significant reason is political influence in the banking sector, which needs to be addressed. As a result, public banks are affected more than private banks. Moreover, credit and liquidity risks are barriers to the sustainable functioning of commercial banks. All credit risk management issues can be overcome by following the Basel guidelines and world banking instructions. The State Bank of Pakistan (SBP) and the Security and Exchange Commission of Pakistan (SECP) can significantly control the negative impacts on commercial banks' performance by introducing stricter rules and regulations. The higher regulatory authorities (top management) within the banking sector should take initial steps to make policies and strategies to forgive loan services and better manage these policies.

Recommendations for Further Research

The findings of this study provide valuable insights and information that can contribute to future research focused on credit risk management and the evaluation of bank performance. A suggestion for prospective researchers is to enhance the research model by incorporating additional indicators or variables. In addition to the indicators used in this research, researchers can consider including other variables, such as stock market return (SMR), risk-weighted asset (RWA), net profit margin (NPM), price-to-book ratio (PB), dividend per share (DPS), overhead efficiency ratio (OER), interest expense ratio (IER), and more. These variables can provide a comprehensive overview of profitability and CRM indicators, including Interest coverage ratio (ICR), loan to total deposit (LOANDEP), customer deposit to total liabilities (CUSDEP), non-interest income / total operating income (NONINT), and cost to income (CI) in commercial banks operating in Pakistan. Additionally, the current study utilised data from 27 out of 31 commercial banks. Future researchers can incorporate data from the remaining banks. With sufficient resources and time, the sample size could be increased by involving microfinance banks, investment banks, and other financial institutions.

Abdesslem, R. B., Chkir, I., & Dabbou, H. (2022). Is managerial ability a moderator? The effect of credit risk and liquidity risk on the likelihood of bank default. International Review of Financial Analysis, 80, Article e102044. https://doi.org/10.1016/j.irfa.2022.102044

Akbar, M. (2023). Analysis of the effect of Capital Adequacy Ratio (Car), Non-Performing Loan (Npl), and Operating Cost Operating Income (Bopo), Net Interest Margin (Nim) to Loan to Deposit Ratio (LDR) of state-owned banks in Indonesia. Journal of Social Research, 2(5), 1591–1607. https://doi.org/10.55324/josr.v2i5.868

Akhter, N. (2023). Determinants of commercial bank's non-performing loans in Bangladesh: An empirical evidence. Cogent Economics & Finance, 11(1), Article e2194128. https://doi.org/10.1080/ 23322039.2023.2194128

Amissah, M., & Opoku, O. A. (2023). Effect of capital adequacy requirement on profitability of selected banks listed on Ghana stock exchange. Journal of Management Studies and Development, 2(1), 13–25. https://doi.org/10.56741/jmsd.v2i01.174

Anees, Z., Iftikhar, K., & Rizvi, S. Z. A. (2023). Impact of Basel Accord on bank lending: A case study of Pakistani commercial banks. Pakistan Journal of Social Research, 5(1), 381–391.

Awaluddin, M. R., Haliah, H., & Kusumawati, A. (2023). The effects of non-performing loans and loan-to-deposit ratio toward return on asset. International Journal Of Humanities Education and Social Sciences (IJHESS), 2(6), 2164–2168. https://doi.org/10.55227 /ijhess.v2i6.501

Cao, Q., Giordani, P., Minetti, R., & Murro, P. (2023). Credit markets, relationship lending, and the dynamics of firm entry. Review of Economic Dynamics. Advanced online publication. https://doi.org/10. 1016/j.red.2023.02.001

Chike, C. B., & Ebere, C. C. (2023). The role of corporate heterogeneity in the relationship between credit risk management and bank performance. Central Asian Journal of Innovations on Tourism Management and Finance, 4(1), 72–85. https://doi.org/10. 17605/OSF.IO/FJX9C

Dimitrov, D., & van Wijnbergen, S. (2023). Macroprudential regulation: A risk management approach (DNB Working Paper No. 765). https://www.dnb.nl/media/yxwonyq1/working_paper_no-765.pdf

Duho, K. C. T., Duho, D. M., & Forson, J. A. (2023). Impact of income diversification strategy on credit risk and market risk among microfinance institutions. Journal of Economic and Administrative Sciences, 39(2), 523–546. https://doi.org/10.1108/JEAS-09-2020-0166

Emmanuel, A. O., Olaoye, A. F., & Afolabi, B. (2021). Impact of Credit Risk on Bank Performance in Nigeria. International Journal of Management, 12(3), 165–174. https://doi.org/10 .34218/IJM.12.3.2021.015

Gjeci, A., Marinč, M., & Rant, V. (2023). Non-performing loans and bank lending behaviour.Risk Management,25, Article e7. https://doi.org/10. 1057/s41283-022-00111-z

Grzeta, I., Zikovic, S., & Tomas Zikovic, I. (2023). Size matters: Analysing bank profitability and efficiency under the Basel III framework.Financial Innovation,9, Article e43. https://doi.org/10. 1186/s40854-022-00412-y

Gujarati, D. N., & Porter, D. C. (2009). Business & economics. McGraw-Hill Irwin.

Keqa, F. (2023).Testing capital adequacy ratio in western Balkan countries and it is compliance with Basel Accord III[Doctoral dissertation, EPOKA University]. EPOKA University Repository. http://dspace. epoka.edu.al/handle/1/2279

Khan, N., Ramzan, M., Kousar, T., & Shafiq, M. A. (2023). Impact of bank-specific factors on credit risk: Evidence from Islamic and conventional banks of Pakistan.Pakistan Journal of Humanities and Social Sciences,11(1), 580–592. https://doi.org/10.52131/pjhss.2023.1101. 0375

Kolsi, M. C., Al-Hiyari, A., & Hussainey, K. (2023). Does environmental, social, and governance performance mitigate earnings management practices? Evidence from US commercial banks.Environmental Science and Pollution Research,30(8), 20386–20401. https://doi.org/ 10.1007/s11356-022-23616-2

Musa, M. M., & Nasieku, D. T. (2019). Effects of credit risk management on loan performance of commercial banks in Kenya: A case of listed commercial banks in Kenya.International Journal of Recent Research in Social Sciences and Humanities (IJRRSSH),6(2), 140–146.

Mushafiq, M., Sindhu, M. I., & Sohail, M. K. (2023). Financial performance under influence of credit risk in non-financial firms: evidence from Pakistan.Journal of Economic and Administrative Sciences,39(1), 25–42. https://doi.org/10.1108/JEAS-02-2021-0018

Naili, M., & Lahrichi, Y. (2022). The determinants of banks' credit risk: Review of the literature and future research agenda.International Journal of Finance & Economics,27(1), 334–360. https://doi.org/10. 1002/ijfe.2156

Nazeer, N., Ali, S., & Rind, A. (2022). Using mixed-method to explore barriers and cues to action in the adoption of green banking practices in commercial banks of Pakistan.International Journal of Finance, Insurance and Risk Management,12(4), 136–153.

Nguyen, D. T., Le, T. D., & Tran, S. H. (2023). The moderating role of income diversification on the relationship between intellectual capital and bank performance evidence from Vietnam.Cogent Business & Management,10(1), Article e2182621. https://doi.org/10.1080 /23311975.2023.2182621

Orden‐Cruz, C., Paule‐Vianez, J., & Lobão, J. (2023). The effect of economic policy uncertainty on the credit risk of US commercial banks.International Journal of Finance & Economics,28(3), 3420–3436. https://doi.org/10.1002/ijfe.2600

Proença, C., Augusto, M., & Murteira, J. (2023). The effect of earnings management on bank efficiency: Evidence from ECB-supervised banks.Finance Research Letters,51, Article e103450. https://doi.org /10.1016/j.frl.2022.103450

Quaglia, L. (2023). The non‐reversal of delegation in international standard‐setting in finance: The Basel Committee and the European Union.Governance,36(1), 41–57. https://doi.org/10.1111/gove.12696

Rafique, Z. Z., Toor, K. N., & Bashir, Z. (2020). Capital adequacy and management quality for banking liquidity management decision in Pakistan. KASBIT Business Journal, 13(1), 25–42. http://dx.doi.org /10.2139/ssrn.3936408

Sharma, D. K., & Kaur, R. (2021). Relationship between credit risk management and profitability performance of Indian public sector banks. GE-International Journal of Management Research, 9(3), 2394–4226.

Syafrizal, A., & Ilham, R. N. (2023). Effect of capital adequacy ratio, non-performing financing, financing to deposit ratio, operating expenses and operational income on profitability at pt. Bank Aceh Syariah.Journal of Accounting Research, Utility Finance and Digital Assets,1(4), 312–322.

Uddin, M. M., Islam, M. T., & Al Farooque, O. (2023). Effects of politically controlled boards on bank loan performance: an emerging economy perspective.Journal of Accounting in Emerging Economies,13(3), 566–588. https://doi.org/10.1108/JAEE-11-2021-0353

Wahyuni, P. D., Umam, D. C., No, J. M. S., & No, J. S. K (2023). The Effect of Credit Risk, Capital Adequacy and Operational Efficiency on Banking Financial Performance with a Profitability Approach. International Journal of Economics, Business and Management Research, 7(6), 12–28. https://doi.org/10.51505/IJEBMR.2023.7602

Zamore, S., Beisland, L. A., & Mersland, R. (2023). Excessive focus on risk? Non‐performing loans and efficiency of microfinance institutions.International Journal of Finance & Economics,28(2), 1290–1307. https://doi.org/10.1002/ijfe.2477