Kaneez Fatima1, Aisha Javaid2*, Musarrat Karamat2

1 Institute of Management Sciences, University of Baluchistan, Quetta, Pakistan

2 Department of Management Sciences, Baluchistan University of Information Technology, Engineering and Management Sciences, Quetta, Pakistan.

* Corresponding author: [email protected]

This paper analyzes the trends in earnings management (EM) practices of 500 non-financial firms across 8 major industries operating in both developing and developed economies for the period 2008-2017. It significantly contributes to the literature by identifying the country-specific, industry-specific, and over the time trends in accrual and real earnings management practices prevailing in the non-financial sector of both developed and developing economies of the world. EM trends are analyzed across countries, across industries, and over the sample period. The sample consists of 500 non-financial firms from 8 different industries of 22 developed and developing economies for the period 2007-2018. Accrual and real earnings management are alternatively used in the non-financial sector across the world. This study uses the Modified Jones Model (Dechow et al., 1996) and the Roychowdhury model (2006) to estimate accrual and real earnings management. The analysis of variance (ANOVA) is used to examine the mean differences between countries and industries as well as over the time differences. The country-wise analysis concludes that Pakistan is on the top of the list in managing earnings followed by Canada, particularly in accrual-based earnings management. It may be attributed to poor accounting standards and regulatory frameworks. The industry-wise analysis shows that the mining industry, characterized by high dependency on capital markets and the uncertainty associated with the prospects of mineral reserves, is highly involved in EM. Finally, the year-wise analysis determines that the year 2009 was highly escorted with accrual and real earnings management practices, which may be the result of the global financial crisis of 2007-2008. The findings imply that the policymakers of developing economies should strongly emphasize improving the general macroeconomic environment of the economy by controlling inflation, improving law and order conditions, and ensuring political stability. Additionally, the findings have potential implications for corporate managers while formulating strategies to restrict them from EM that may diminish both firm value and the economy.

Keywords: accrual earnings management (AEM), country, earnings management (EM), industry, non-financial sector, real earnings management (REM)

JEL Classification: C50, C52, C53

The major accounting scandals of the world's leading economies, including the UK (Tesco), USA (WorldCom and Enron), Japan (Olympus), Canada (Biovail), and Australia (One. Tel) raised questions about the integrity and reliability of the financial reporting system. The primary objective of a financial reporting system is to assist stakeholders in decision-making by providing reliable and consistent information. Both internal and external stakeholders use the company's annual financial statements to formulate corporate policies (Ghazali & Shafie, 2015). Annual reported earnings provide a snapshot of a firm's financial performance, economic growth, and efficient resource allocation. So, considering the importance of a sound reporting mechanism, an efficient accounting system should deliver valuable information to creditors, investors, government agencies, customers, and employees in order to guide them regarding future investment and business decisions (Watts & Zimmerman, 1986; Spohr, 2005). The more this information is reliable and relevant, the more it is useful for decision-making (Spohr, 2005).

The use of discretionary power by managers in reporting accounting information in a way that is most appropriate for themselves or the company is known as earnings management (EM). It is a topic of interest for academicians and practitioners and has been discussed by them widely (Jiraporn et al., 2008). Healy and Wahlen (1999) defined EM as managerial judgment in reporting financial information and structuring financial transactions to modify financial statements. This modification either misleads the stakeholders regarding the annual economic performance of the firm or influences contractual outcomes associated with the reported accounting figures.

Leuz et al. (2003) stated that EM comprises an intentional adjustment in the firm's reported earnings, either to misguide outsiders regarding the firm’s economic performance or to control the future contractual outcomes which depend on the annual reported earnings. Although there is no universal definition of EM, the focal point is that managerial intention is its prerequisite. Meanwhile, the legitimacy of the managerial intention remains unclear, whether it is discretionary or opportunistic. The opportunistic or illegitimate manipulations in reported earnings lead to fraudulent and fake financial statements, which surely mislead the stakeholders during decision-making. However, some researchers argued about the fairness of the managerial intention and used the term discretionary instead of opportunistic while discussing the concept of EM (Dechow & Skinner, 2000; Scott, 2003).

According to Dechow et al. (2010), EM is an important factor affecting the quality of accounting information. There are two types of EM namely accrual-based earnings management (AEM) and real earnings management (REM). Accruals are the most powerful approach to EM. Accruals comprise the difference between the firm's earnings after taxes and cash flows. Discretionary accruals are manipulated when the managers use their judgment to report earnings to meet or beat the analysts' forecasts (Tabassum et al., 2015). In comparison, REM involves the timing and structuring of actual business activities to achieve the desired financial reporting results (Roychowdhury, 2006).

AEM and REM are the widely used tools by the executives to manipulate the reported earnings of the firms. Although these strategies are used as each other’s substitutes according to managerial discretion and accounting procedures prevailing in the economy (Zang, 2012). The predictions of agency theory (Meckling & Jensen, 1976) and positive accounting theory (Watt & Zimmerman, 1986) imply that EM practices are highly responsive to information asymmetry, agency issues, and managerial intentions towards alternative accounting policies. Moreover, there are some industry-specific and country-specific reasons which motivate managers towards EM (Enomoto et al, 2018; Saona & Muro, 2018). These country-specific differences include the development of financial system, law and order situation, and financial monitoring mechanisms. Further, industry level characteristics, such as board size, audit committee independence, financial leverage, CEO/Chair duality, firm size, and firm performance may also affect the EM practices of firms (Bui & Le, 2021). Hence, identifying these differences is a worthwhile task. This study argues that if EM is attributed to agency problem, information asymmetry, and flexibility in accounting standards, then its practices should vary over time depending on firm specific, industry-specific, and country-specific characteristics. Therefore, this study intends to analyze the over the time variations in the above discussed motives behind EM, which may influence the level of AEM and REM trends across countries and industries.

Hence, this paper contributes to the literature by identifying the country-wise, industry-wise, and year-wise trends of EM practices in the non-financial firms of different countries. The research also investigates whether AEM and REM behavior of executives significantly differs from country to country, industry to industry, or year to year. This research is important and distinctive in nature as it helps to identify the countries and industries which highly practice EM. The results make a significant contribution to the existing literature by guiding potential investors, policymakers, and corporate managers in formulating their governance strategies and foreign investment plans to avoid unfavorable consequences or outcomes.

The study uses the Modified Jones Model (Dechow et al., 1996) and the Roychowdhury (2006) model to estimate AEM and REM, respectively. The Generalized Method of Moments (GMM) is applied to estimate the models and residuals are used as measures of EM. The mean values of AEM and REM are used to analyze trends in EM practices in countries, industries, and over time.

It was found that at the firm level, some countries, including Pakistan and Canada, highly practice AEM. In contrast, Indonesian firms highly use REM as a tool to manipulate their reported earnings. The year-wise analysis indicates that 2009, the year after the financial crisis, was escorted with the highest AEM and REM levels, which is not surprising. Further, at the industry level, the current study confirmed that both AEM and REM are more prevalent in the mining industry than in other industries.

The rest of the paper is organized as follows. Section two reviews the literature briefly, section three lays out the methodology, section four presents the result, and section five concludes the research findings.

EM has become an issue of global concern since the failure of some mega corporations due to financial misreporting in the recent past. These corporate failures and scandals have raised questions regarding the reliability and informativeness of annual financial reports. Earnings are a very important figure on a company's financial statements since they provide the snapshot of its financial performance (Johari et al., 2009). Earnings influence stock price fluctuations and also serve to gauge the prospects of shareholder's wealth (Tabassum et al., 2014). Managers use this gadget through earning management either to communicate their private information to capital markets or to obtain their rewards such as bonuses and Perks etc., which, in turn, affect the informativeness of accounting earnings (García-Meca & Sánchez-Ballesta, 2009).

Agency conflicts, arising from the divergence of interest between managers and shareholders, are the main cause of EM (Yang et al., 2008; Yimenu & Surur, 2019). Agency conflicts, coupled with information asymmetry, incur agency costs[1] to the firms and induce mangers to manipulate earnings (Healy, 1985; García-Meca & Sánchez-Ballesta, 2009). Agency issues can be attributed to the segregation of ownership and control in the corporate sector. This creates room for managers to use the flexibility of the generally accepted accounting principle (GAAP) opportunistically, with the aim to manipulate the accounting figures intentionally, in order to secure economic benefits at the cost/expense of shareholder's wealth (Jiraporn et al., 2008).

Agency theory was presented by Meckling and Jensen (1976). This theory thoroughly discusses agency problems arising from the separation of ownership and control. The foundation of agency theory is the conflict of interest aligned with the separation of ownership and control. The proponents of this theory assert that agency relationship leads to information asymmetry, which inclines corporate executives towards the window dressing of financial reports without violating the accounting principles (Yimenu & Surur, 2019). Therefore, the misalignment of interest between owners and managers motivates managers towards EM with the intention to increase earning-based incentives or to avoid contractual constraints (Healy, 1985; Weisbach, 1988).

Further, positive accounting theory is a widely discussed theory in the EM literature. The essence of positive accounting theory is the reason why managers choose alternative accounting methods and the economic consequences of financial accounting and reporting. However, this theory is very much associated with the concepts of efficient market hypothesis (EMH) and the capital asset pricing model (CAPM) (Whittington, 1987). A more precise definition of the positive accounting theory has been presented by Watt and Zimmerman (1986) stating that "PAT is a theory concerned with the explanation and prediction of accounting choices and the response of agents for new accounting standards or policies." This argument highlights the importance of accounting numbers in facilitating contracting parties and helps to reduce information asymmetry as well as agency conflicts.

Further, questions can be raised regarding how managers manipulate reported earnings? Numerous studies have strived to answer this question and documented different methods of EM. Using AEM, managers exploit the latitude of accepted accounting procedures under the most widely used accounting system, known as the generally accepted accounting principle (GAAP). AEM allows managers to record the effects of financial information at the time of the occurrence of a specific transaction, instead of recording the particular transaction when cash inflow and outflow occur. Hence, the impulsive nature of this method of accounting, as well as the information asymmetry between managers and stockholders, promote discretionary managerial practices to determine the level of accounting income reported by the firm in the concurrent period. Consequently, while using GAAP, managers are more inclined towards the opportunities to hunt their benefits and to pursue the signaling of the insider information to financial markets, leading to a shift in the market prices of certain securities (Healy, 1985). Moreover, by manipulating earnings, managers can exercise their power to control the timings of reporting revenues and expenses in order to determine the firm's financial performance, particularly to upsurge their remuneration and promotion plans linked with the betterment of its performance.

One can argue that how can one decide whether the managerial intention is legitimate or illegitimate? In this context, the legitimacy of managerial intentions can be justified by applying GAAP. If managerial activities are within the boundaries of GAAP, then they are considered legitimate. If such activities go beyond the defined rules of GAAP, they would be considered illegitimate (Al Khabash & Al Thuneibat, 2009). Managers have the power and control to adopt the accounting policies suitable for the firm among the acceptable accounting methods to report their accounting earnings (Dechow & Skinner, 2000). This discretionary power in the managerial position is mandatory in employment of EM policies (Jiraporn et al., 2008).

Another strand of literature postulates that the concept of EM has two facets. It may be either good or bad for the organization. Parfet (2000) categorizes EM into bad and good EM. Bad EM is "improper earnings management because it intervening to hide real operating performance by creating artificial accounting entries or stretching estimates beyond a point of reasonableness". In contrast, good EM is the "reasonable and proper practices that are part of operating a well-managed business and delivering value to shareholders".

Further, literature documents different EM methods (Fudenberg & Tirole, 1995; Healy & Wahlen, 1999; Dechow & Skinner, 2000; Roychowdhury, 2006). Executives can manage accounting earnings by using their discretionary power embedded within the varying nature of accounting accruals (AEM) or by restructuring the real activities REM). AEM does not directly affect cash flows; rather, it reflects discretionary alteration by the managers in the firm's financial reports (Zang, 2012; Cohen & Zarowin, 2010).

In contrast, REM can be conducted through operational, investment, and financing decisions. Literature reports the most widely used methods of REM (Herrmann et al., 2003; Gunny, 2005; Roychowdhury, 2006; Hribar et al., 2006; Burnett et al., 2012; Ghaemi et al., 2012; Enomoto et al., 2018). These methods include sales manipulation through temporary price discounts, reduction in discretionary expenses, overproduction, and changing shipment schedules (operating activities). Further, real earnings can also be managed by reducing investment in research and development, selling fixed assets (investing activities), and restructuring the financing mix via stock option and stock repurchases (financing activities).

In this context, Zang (2012) contends that the two types of EM can substitute each other. Managers can alternatively use these strategies, depending on the prevailing accounting procedures and the regulatory framework of the country's financial system. However, strict legal requirements and tight accounting policies restrain AEM and ultimately increase REM (Ewert & Wagenhofer, 2005).

This extensive review of the literature manifests the following facts regarding EM. Firstly, agency theory and the positive accounting theory are the two underlying theories of EM. Secondly, the detrimental role of GAAP was identified in increasing the discretionary power of managers. Thirdly, prior studies have documented the legitimacy of EM while addressing the questions that whether EM is legal or illegal and good or bad. Fourthly, many studies have documented different AEM and REM methods, which can be used alternatively.

Conclusively, this critical review reveals that EM is a widely used managerial tactic to manipulate accounting numbers in various industries and economies. In this regard, several studies have investigated the EM behaviors of executives in different contexts and economies at firm and industry level. However, this review shows that the country wise, industry wise, and time wise differences have not been addressed in the literature. The current study argues that if EM is attributed to agency problem, information asymmetry, and flexibility in accounting standards, then the EM activities should vary over time depending on firm-specific, industry-specific, and country-specific characteristics. The country-specific differences include the development of financial system, law enforcement, investor protection laws, and financial monitoring mechanisms. Whereas, industry level characteristics, such as board structure, audit structure, financial leverage, and firm size and performance may affect the EM practices of firms (Bui & Le, 2021; Flayyih & Khiari, 2022; Al-Zaqeba et al., 2022). This study is an addition to earlier studies as it analyzes the EM practices across different countries and industries for a period of ten years. Furthermore, it significantly contributes to the literature by identifying the countries and industries escorted with higher EM over the sample period. Moreover, it identifies the years with higher EM across the world. To meet the above objectives, the following hypotheses are proposed.

Hypothesis 1: Country-specific characteristics may significantly influence the level of EM practices.

Hypothesis 2: Industry-specific characteristics may significantly influence the level of EM practices.

Hypothesis 3: Trends in EM practices significantly differ over the sample period.

Population, Sample, and Data

The population of this study comprises the non-financial firms listed on the stock exchanges of various developing and developed economies. Initially, a sample of 672 non-financial firms was drawn from the population. After applying the missing value analysis and some filtering techniques, the final sample consisted of 500 non-financial firms from 8 different industries of 22 developed and developing economies.[2] The study period covers the years 2007-2018. The sample period starts form 2008 as it is the year after the global financial crisis. The period before the global financial crisis is ignored to avoid any structural breaks in the data. However, 2007 and 2008 are considered lag years for the unbiased estimation of AEM and REM. The final data for this study comprises 4000 firm-year observations. The annual financial reports of the sample firms, their respective websites, and stock exchanges of sample countries remain the major sources of data for the firm-specific information and market information required for the estimation of EM.

Depending on the endogenous nature of the selected EM variables, the generalized method of moments (GMM) is used as the estimation technique (1-5 in section 3.2). GMM is an estimation technique with robust standard errors to control unobservable individual heterogeneity and endogeneity problems, which are the major econometric problems observed in panel data analysis. Ordinary least squares (OLS) estimation produces inefficient and biased results in the presence of these issues. Particularly, some variables of the underlying study, such as AEM and REM, include multiple lag values. These endogenous variables cause serial correlation between residuals and lagged values. Hence, the problem arises of biasness and unreliability in results. Hence, to resolve the problem of misspecification, the GMM method is used as the estimation technique which includes the first lag of dependent variables in the level equation and lagged values of dependent and independent endogenous variables as instrument variables in regression analysis (Arellano & Bond, 1991; Arellano & Bover, 1995).

Before applying GMM, some preliminary tests were applied to check whether this method is appropriate for the panel data estimation of the underlying research. These include variance inflation factor (VIF) to test multicollinearity, Bruesch Pagan test for heteroskedasticity, and Hansen j statistics for the over-identification of instruments (see Hansen, 1982).

Estimation of EM

AEM and REM are the proxies of EM used in this study. AEM is used to investigate the effects of income increasing and income decreasing discretionary accruals. Further, the absolute value of abnormal accruals is used as a proxy of AEM (Cohen et al., 2008; Nugrahanti, 2016; Nazir & Afza, 2018; Enomoto et al., 2018). Following prior studies, including Koh (2005) and Nugrahanti (2016), a modified version of the Jones cross-sectional model (Dechow et al., 1996) is applied for the estimation of country-wise, year-wise, and industry-wise AEM.

TACCijt=α0 (1⁄Assets(ijt-1))+α1 (∆REVijt-∆RECijt )+α2 (PPEijt )+εijt (1)

where,

TACC(ijt)= Total accruals

Assets(ijt-1)= Lagged value of total assets

∆REVijt= Change in revenue

∆RECijt = Change in receivables

PPEijt= = Gross property, plant, and equipment

α0-n 0-n = Estimated parameters of the models

εijt = Residuals of the model

Subscripts i, j, and t refer to firm, country, and time, respectively

All variables are to be scaled by the lagged values of total assets (1⁄Assets(ijt-1)).

To measure REM, three methods of sales manipulation, reduction in discretionary expenses, and overproduction are employed (Roychowdhury, 2006). For this purpose, three models are used based on the abnormal levels of operating cash flows, discretionary expenses, and overproduction, respectively. These models are depicted in the equations below.

OCF(ijt)=β0+β1 (1⁄Assets(ijt-1) )+β2 (Salesijt)+β3 (∆Salesijt)+εijt (2)

DEijt=β0+β1 (1⁄Assets(ijt-1) )+β2 (Salesijt )+εijt (3)

PROD(ijt)=β0+β1 (1⁄Assets(ijt-1) )+β2 (Salesijt)+β3 (∆Salesijt)+β3 (∆Sales(ijt-1) )+εijt (4)

where,

OCF(ijt)= Operating cashflows

DEijt= Discretionary expenses (General + Administrative)

PROD(ijt)= Production cost (Cost of goods sold + Change in inventory)

Salesijt= Current level of sales

∆Salesijt= Change in sales

β0-n0-n = Estimated parameters of the model

εijt= Residuals of the model

Subscripts i, j, and t refer to firm, country, and time, respectively.

All variables are to be scaled by the lagged values of total assets

By applying GMM analysis on models 2-4, their residuals such as OCF, DE, and PROD values are analyzed, respectively. Afterwards, absolute values of these three proxies are used to apprehend the total effect of REM. Further, the absolute values of OCF and DE are multiplied with a negative one and then added to the absolute value of PROD to calculate the aggregate effect of REM (Enomoto et al., 2018; Cohen & Zarowin, 2010; Tabassum et al., 2014).

REMijt=(OCFijt )(-1)+(DEijt )(-1)+PRODijt) (5)

Hence, model 1 is used to estimate the AEM practices and model 5 is used to estimate the REM practices of sample firms. Finally, ANOVA is used to find the significant differences in the EM practices of sample firms across countries and across industries over the sample period.

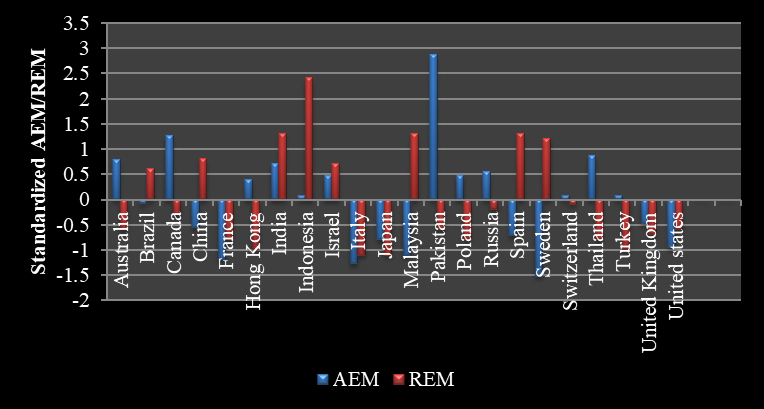

Country-wise EM Analysis

Country-wise analysis of accrual and real earnings management is performed using ANOVA. The results are reported in Table 1. The table shows the standardized mean comparison of the sample countries' AEM and REM practices. Figure 1 graphically presents the results.

Table 1

Country-wise AEM and REM Analysis

|

Country |

N11 |

AEM |

N2 |

REM |

|

Australia |

351 |

0.7983 |

193 |

-0.5980 |

|

Brazil |

184 |

-0.0798 |

115 |

0.6071 |

|

Canada |

450 |

1.2773 |

261 |

-0.2967 |

|

China |

360 |

-0.5588 |

188 |

0.8080 |

|

France |

450 |

-1.1975 |

222 |

-0.7989 |

|

Hong Kong |

441 |

0.3991 |

272 |

-0.9997 |

|

India |

355 |

0.7185 |

185 |

1.3102 |

|

Indonesia |

153 |

0.0798 |

84 |

2.4150 |

|

Israel |

87 |

0.4790 |

54 |

0.7076 |

|

Italy |

144 |

-1.2773 |

68 |

-1.1002 |

|

Japan |

90 |

-0.7983 |

51 |

-1.1002 |

|

Malaysia |

261 |

-1.1176 |

161 |

1.3102 |

|

Pakistan |

331 |

2.8740 |

214 |

-0.5980 |

|

Poland |

90 |

0.4790 |

38 |

-0.7989 |

|

Russia |

153 |

0.5588 |

72 |

-0.1963 |

|

Spain |

144 |

-0.7185 |

55 |

1.3102 |

|

Sweden |

126 |

-1.5168 |

75 |

1.2098 |

|

Switzerland |

117 |

0.0798 |

58 |

-0.0958 |

|

Thailand |

99 |

0.8781 |

49 |

-0.7989 |

|

Turkey |

117 |

0.0798 |

66 |

-0.9997 |

|

United Kingdom |

387 |

-0.4790 |

224 |

-0.6984 |

|

United States |

450 |

-0.9580 |

290 |

-0.5980 |

|

Total |

3876 |

2995 |

||

|

F values |

6.875** |

2.018*** |

||

Note. This table presents the country-wise analysis of accrual and real earnings management using one-way ANOVA. N1 and N2 show the number of observations used to estimate AEM and REM values, respectively. F values indicate the significance of the mean difference between sample countries. Furthermore, *, **, and *** indicate the significance level at 10%, 5%, and 1%, respectively.

As evident by Table 4.1 and Figure 4.1, all the sample countries are involved in income increasing AEM[3]. In this context, Pakistani firms are highly involved in increasing their discretionary accruals (with a standardized AEM value of 2.8740). Canadian firms have the second highest rank in accrual earnings manipulations (with a standardized AEM value of 1.2773). Swedish firms are less involved in AEM (with a standardized AEM value of -1.5168), followed by Italy and France (with a standardized AEM value of -1.2773 and -1.1975, respectively).

Moreover, these results depict that Indonesia has the highest rank (with a standardized REM value of 2.4150) in REM[4], whereas firms in India, Malaysia, and Spain also highly practice REM (with a standardized REM value of 1.3102). On the contrary, firms of Japan and Italy (with a standardized REM value of -1.1002) make the least use of REM practices, followed by those of Hong Kong and Turkey (with a standardized REM value of -0.9997).

Figure 1 depicts that firms in all developing and developed countries selected as sample are engaged in AEM and REM practices. It is interesting to observe that firms in developed economies are less engaged in EM than developing economies. Indeed, firms in developed countries, such as Italy, Japan, U.S.A., and the U.K. are least involved in both types of EM. On the contrary, firms in developing countries, such as India, Indonesia, and Israel are highly involved in both types of EM. These results are consistent with the findings of Javaid et al. (2021). They found that firms operating in developing economies are highly involved in AEM and REM practices. The results of the current descriptive analysis confirm that at the firm level, AEM practices highly prevail in some countries, including Pakistan and Canada. The higher level of EM in Pakistan may be due to political and economic instability and market pressures, which negatively affect financial performance and yield low accounting profits. In this business environment, corporate managers in developing countries amend their financial statements to show profitability by manipulating temporary income increasing discretionary accruals and restructuring various business transactions in order for them to be in line with stock market fluctuations (Türegün, 2020). Moreover, corporate managers in developing economies can opportunistically manipulate earnings, particularly discretionary accruals, in the absence of a strict regulatory framework and standardized accounting procedures (Enomoto et al., 2018). These results are also consistent with Zang (2012), who recommends that both AEM and REM practices be used as substitutes. However, managers prefer REM in the presence of better accounting standards and strict legal requirements. Further, F values (6.875 and 2.018 in table 4.3) of one-way ANOVA indicate significant differences among sample firms using AEM and REM practices

Figure 1

AEM and REM Practices across Countries

Note. This figure shows the trends in accrual and real earnings management practices in the sample countries. Standardized AEM and REM values on the vertical axis above the origin indicate above-average EM, while values below the origin show EM below the mean in standardized units.

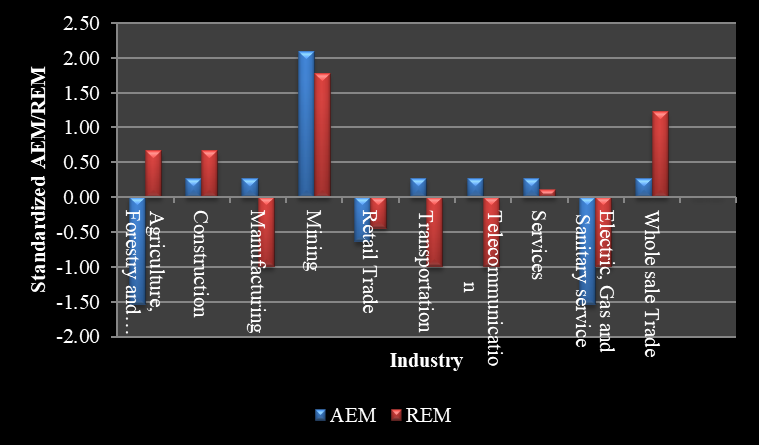

In this section, the industry-wise analysis of accrual and real earnings management practices is performed using ANOVA. The results are reported in Table 4.2. The table shows the standardized mean comparison of AEM and REM practices in sample industries. Figure 4.2 graphically presents the results.

Table 2

Industry-wise AEM and REM Analysis

|

Industry |

N1 |

AEM |

N2 |

REM |

|

Agriculture, Forestry, and Fishing |

45 |

-1.55 |

21 |

0.67 |

|

Construction |

393 |

0.27 |

225 |

0.67 |

|

Manufacturing |

2251 |

0.27 |

1253 |

-1.00 |

|

Mining |

613 |

2.09 |

329 |

1.78 |

|

Retail Trade |

279 |

-0.64 |

162 |

-0.44 |

|

Transportation |

298 |

0.27 |

107 |

-1.00 |

|

Telecommunication |

368 |

0.27 |

198 |

-1.00 |

|

Services |

509 |

0.27 |

299 |

0.11 |

|

Electric, Gas and Sanitary service |

423 |

-1.55 |

300 |

-1.00 |

|

Wholesale Trade |

161 |

0.27 |

101 |

1.22 |

|

Total |

3876 |

2995 |

||

|

F values |

6.868*** |

2.650** |

||

Note. The table presents the industry-wise analysis of accrual and real earnings management using one-way ANOVA. N1 and N2 show the number of observations used to estimate AEM and REM values, respectively. F values indicate the significance of the mean difference between sample countries. Furthermore, *, **, and *** indicate the significance level at 10%, 5%, and 1%, respectively.

Table 2 and Figure 2 show the industry-wise analysis of accrual and real earnings management for sample firms in both developing and developed countries. These results indicate that both AEM and REM are more prevalent in the mining industry, with standardized mean AEM and REM values of 2.09 and 1.78, respectively. These EM practices may be highly prevalent in the mining industry due to several reasons. Firstly, this industry is highly dependent on capital markets to finance the mining projects. Such projects usually incur a very high cost, resulting in low income during this period. Secondly, the uncertainty associated with the prospects of mineral reserves and resources may sometimes induce managers to manage accounting earnings upwards, temporarily (Arponen, 2015).

On the other hand, the results show that the firms in electric, gas, and sanitary services are less involved in EM practices. These industries obtained the lowest rank in AEM and REM with standardized AEM and REM values of -1.55 and -1.00, respectively. The reason for the low AEM and REM levels in the electric, gas, and the sanitary services industry may be that these industries are highly profitable which may be due to the market powers these types of firms hold. Hence, corporate executives of these industries do not need EM tools to exacerbate their reported earnings.

Figure 2

AEM and REM Practices across Industries

Note. This figure shows the trends in accrual and real earnings management practices in the sample industries. Standardized AEM and REM values on the vertical axis above the origin indicate above-average EM. The values below the origin show EM below the mean in standardized units.

Moreover, agriculture, forestry, and the fishing industry score below average in using AEM practices, although their involvement in REM practices remains above average. Contrary to this finding, manufacturing, transportation, and the telecommunication industry secure the lowest rank in REM, although they achieve the highest rank in AEM. These results further indicate that both types of EM are highly prevalent in some industries, such as mining, construction, and wholesale trade. While, in several industries, AEM and REM are used as alternative techniques to manage earnings, depending on the industry-specific characteristics and the subsequent risk and return ratios. Country-specific characteristics may include macroeconomic factors, political instability, and prevailing accounting and auditing standards (Saona & Muro, 2018). Further, F values of one-way ANOVA for AEM (6.868 in table 4.2) and REM (2.650 in table 4.2) indicate that the differences in EM practices of sample industries are statistically significant.

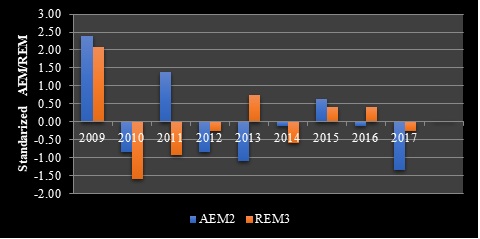

This section analyzes year-wise accrual and real earnings management using ANOVA. The results are reported in Table 3, with their graphical presentation in Figure 3. The table indicates the standardized mean comparison of AEM and REM practices during the sample period.

Table 3

Year-wise AEM and REM Analysis

|

Year |

N1 |

AEM |

N2 |

REM |

|

2009 |

595 |

2.39 |

340 |

2.07 |

|

2010 |

598 |

-0.86 |

327 |

-1.59 |

|

2011 |

599 |

1.39 |

336 |

-0.93 |

|

2012 |

599 |

-0.86 |

335 |

-0.26 |

|

2013 |

598 |

-1.11 |

327 |

0.74 |

|

2014 |

598 |

-0.11 |

320 |

-0.59 |

|

2015 |

597 |

0.64 |

329 |

0.41 |

|

2016 |

578 |

-0.11 |

348 |

0.41 |

|

2017 |

578 |

-1.36 |

333 |

-0.26 |

|

Total |

3876 |

2995 |

||

|

F values |

2.103** |

0.577** |

||

Notes. This table presents the year-wise analysis of AEM and REM using one-way ANOVA. N1 and N2 show the number of observations used to estimate AEM and REM values, respectively. F values indicate the significance of the mean difference between sample countries. Furthermore, *, **, and *** indicate the significance level at 10%, 5%, and 1%, respectively.

Table 3 and Figure 3 present the year-wise accrual and real earnings management analysis of the sample firms. The results show that the year 2009 was escorted with the highest level of AEM and REM, with standardized mean AEM and REM values of 2.39 and 2.07, respectively. This may be attributed to the global financial crisis of 2007-2008, which hit the economies particularly hard and caused the major stock exchanges of the world to crash overnight. In 2009, after the financial crisis, stock markets across the globe faced many challenges due to the credit crunch caused by the burst of the house pricing bubble and the default of subprime borrowers, which ultimately resulted in a lack of investor confidence. Later, the investors gained confidence when the government and large corporations injected liquidity into capital markets through quantitative easing to finance the banking operations and avoid stock market crash.

Consequently, during financial crunch, the managers of the firms started the window dressing of their financial statements, particularly by manipulating discretionary accruals to avoid showing losses from the global financial crisis. These EM practices were subsequently reduced in 2010 and 2011. The year 2010 secured the lowest rank in REM with the standardized mean REM value of -1.59.

Figure 3

AEM and REM Practices during 2009-2017

Note. This figure shows the trends in accrual and real earnings management practices during the sample period. Standardized AEM and REM values on the vertical axis above the origin indicate above-average EM. Values below the origin show EM below the mean in standardized units.

Moreover, 2017 is the year with the lowest level of AEM and REM. This year, AEM practices remained below the origin (mean value), with a standardized mean AEM value of -1.36. These variations in EM trends may be due to variations in industry-specific and country-specific characteristics of the sample firms. The proponents of EM theories (agency theory and positive accounting theory) assert that the impact of agency issues and discretionary managerial power in exploiting the latitude of accounting procedures may push the EM trends upwards or downwards. F values (2.103 for AEM and 0.577 for REM) confirm that these yearly practices of discretionary earnings manipulation and altering business transactions are statistically significantly dissimilar from each other at 5% level of significance.

This study analyzes the trends in EM practices of firms operating in both developing and developed economies. For this purpose, three different types of analysis, that is, country-wise, industry-wise, and year-wise analysis are conducted using firm-level data. AEM and REM are used as proxies of EM. AEM and REM estimates are obtained by applying GMM on the panel data of 500 non-financial firms listed on the stock exchanges of 22 developing and developed economies.

The findings show that firms operating in developing economies are more inclined towards AEM and REM practices. In this regard, Indonesian firms are highly using REM as a tool to manipulate their accounting earnings. Further, the year-wise analysis shows that 2009 was escorted with the highest AEM and REM levels. The incremental earning manipulation in 2009 can be attributed to the financial distress caused by the global financial crisis of 2007-2008. Further, at the industry level, the study confirms that both AEM and REM are more prevalent in the mining industry. This industry is characterized by the uncertainties associated with the prospects of mineral reserves and resources, as compared to other industries included in the sample.

To conclude, the findings provide valuable insights to all stakeholders, including investors, policymakers, and corporate managers. Crucially, investors should plan their future investments keeping in view the EM activities prevalent in the targeted markets which, in turn, may affect the potential performance of the firms and their subsequent stock returns. Further, the findings imply that favorable domestic economic and political conditions improve the financial performance of firms and may ultimately reduce the earning management practices. Hence, policymakers of developing economies should strongly emphasize improving the general macroeconomic environment of the economy by controlling inflation, improving law and order conditions, reducing economic policy uncertainty, and ensuring political stability. Additionally, the findings have potential implications for corporate managers while formulating strategies to limit EM that may diminish both firm value and the economy.

The current study has some limitations. Firstly, due to limited time and resources, only non-financial firms are included in the sample, while the financial sector firms are ignored. Both sectors significantly differ in terms of the preparation of financial statements, among other characteristics (La Porta et al., 1997). Secondly, this study investigates the cross-country, cross-industry, and cross-time period variations in EM practices independently. However, the over the time trends in EM at country or industry level are not analyzed.

This research opens the doors for future researchers so that they can simultaneously analyze the cross-period, cross-industry, and cross-country trends in EM by applying the generalized method of moments (GMM) or simultaneous equation modeling (SEM) on panel data. Based on the current findings, future researchers can analyze the over the time variation in EM behaviors in a particular industry or a country and determine the factors causing this variation. Further, the substitution effect of AEM and REM can be investigated at sector, industry, or country level so as to determine whether EM is opportunistic or discretionary.

Al-khabash, A. A., & Al-Thuneibat, A. A. (2008). Earnings management practices from the perspective of external and internal auditors: Evidence from Jordan. Managerial Auditing Journal, 24(1), 58–80. https://doi.org/10.1108/02686900910919901

Al-Zaqeba, M. A. A., Abdul Hamid, S., Ineizeh, N. I., Hussein, O. J., & Albawwat, A. H. (2022). The effect of corporate governance mechanisms on earnings management in Malaysian manufacturing companies.Asian Review, 12(5), 354–367.

Arellano, M., & Bond, S. (1991). Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations.The Review of Economic Studies,58(2), 277–297. https://doi.org/10.2307/2297968

Arellano, M., & Bover, O. (1995). Another look at the instrumental variable estimation of error-components models.Journal of Econometrics,68(1), 29–51. https://doi.org/10.1016/0304-4076(94) 01642-D

Arponen, E. (2015). Earnings management in the mining industry. Aalto University, Learning Centre. https://aaltodoc.aalto.fi/handle/ 123456789/18370

Bui, H. T., & Le, H. H. N. (2021, November 3–4). Factors affecting the earnings management: the case of listed firms in Vietnam [Paper presentation]. International Conference on Emerging Challenges: Business Transformation and Circular Economy (ICECH 2021). Hanoi, Vietnam.

Burnett, B. M., Cripe, B. M., Martin, G. W., & McAllister, B. P. (2012). Audit quality and the trade-off between accretive stock repurchases and accrual-based earnings management.The Accounting Review,87(6), 1861–1884. https://doi.org/10.2308/accr-50230

Cohen, D. A., & Zarowin, P. (2010). Accrual-based and real earnings management activities around seasoned equity offerings.Journal of Accounting and Economics,50(1), 2–19. https://doi.org/10.1016/j. jacceco.2010.01.002

Cohen, D. A., Dey, A., & Lys, T. Z. (2008). Real and accrual-based earnings management in the pre-and post-Sarbanes-Oxley periods. The Accounting Review, 83(3), 757–787. https://doi.org/10. 2308/accr. 2008.83.3.757

Dechow, P. M., & Skinner, D. J. (2000). Earnings management: Reconciling the views of accounting academics, practitioners, and regulators. Accounting Horizons, 14(2), 235–250. https://doi.org/10.2308/acch.2000.14.2.235

Dechow, P. M., Sloan, R. G., & Sweeney, A. P. (1996). Causes and consequences of earnings manipulation: An analysis of firms subject to enforcement actions by the SEC. Contemporary Accounting Research, 13(1), 1–36. https://doi.org/10.1111/j.1911-3846.1996.tb00489.x

Dechow, P., Ge, W., & Schrand, C. (2010). Understanding earnings quality: A review of the proxies, their determinants and their consequences. Journal of accounting and economics, 50(2-3), 344–401. https://doi.org/10.1016/j.jacceco.2010.09.001

Enomoto, M., Kimura, F., & Yamaguchi, T. (2018). A cross‐country study on the relationship between financial development and earnings management. Journal of International Financial Management & Accounting, 29(2), 166–194. https://doi.org/10.1111/jifm.12078

Ewert, R., & Wagenhofer, A. (2005). Economic effects of tightening accounting standards to restrict earnings management. The Accounting Review, 80(4), 1101–1124. https://doi.org/10.2308/accr.2005.80.4.1101

Flayyih, H. H., & Khiari, W. (2022). A comparative study to reveal earnings management in emerging markets: Evidence from Tunisia and Iraq.International Journal of Professional Business Review,7(5), Article e0815. https://doi.org/10.26668/businessreview/2022.v7i5.815

Fudenberg, D., & Tirole, J. (1995). A theory of income and dividend smoothing based on incumbency rents. Journal of Political Economy, 103(1), 75–93. https://doi.org/10.1086/261976

Garcia-Meca, E., & Sanchez-Ballesta, J. P. (2009). Corporate governance and earnings management: A meta-analysis. Corporate Governance: An International Review, 17(5), 594–610. https://doi.org/10.1111/j.1467-8683.2009.00753.x

Ghaemi, M. H., Dorosti, A. A., & Masoumi, J. (2012). Earnings management through real activities manipulation: The evidence from Tehran stock exchange. American Journal of Scientific Research, 66(1), 162–166.

Ghazali, A. W., Shafie, N. A., & Sanusi, Z. M. (2015). Earnings management: An analysis of opportunistic behaviour, monitoring mechanism and financial distress. Procedia Economics and Finance, 28(1), 190–201. https://doi.org/10.1016/S2212-5671(15)01100-4

Gunny, K. A. (2010). The relation between earnings management using real activities manipulation and future performance: Evidence from meeting earnings benchmarks. Contemporary Accounting Research, 27(3), 855–888. https://doi.org/10.1111/j.1911-3846.2010.01029.x

Hansen, L. P. (1982). Large sample properties of generalized method of moments estimators. Econometrica: Journal of the Econometric Society, 50(4), 1029–1054. https://doi.org/10.2307/1912775

Healy, P. (1985). The impact of bonus schemes on the selection of accounting principles. Journal of Accounting and Economics, 7(1-3), 85–107. https://doi.org/10.1016/0165-4101(85)90029-1

Healy, P. M., & Wahlen, J. M. (1999). A review of the earnings management literature and its implications for standard setting. Accounting Horizons, 13(4), 365–383. https://doi.org/10. 2308/acch.1999.13.4.365

Herrmann, D., Inoue, T., & Thomas, W. B. (2003). The sale of assets to manage earnings in Japan. Journal of Accounting Research, 41(1), 89–108. https://doi.org/10.1111/1475-679X.00097

Hribar, P., Jenkins, N. T., & Johnson, W. B. (2006). Stock repurchases as an earnings management device. Journal of Accounting and Economics, 41(1–2), 3–27. https://doi.org/10.1016/j.jacceco.2005.10.002

Javaid, A., Fatima, K., & Ahmed, J. (2021). Relationship between corporate governance and earnings management: Moderating role of financial development.Indian Journal of Economics and Business,20(3), 1543–1576.

Jiraporn, P., Miller, G. A., Yoon, S. S., & Kim, Y. S. (2008). Is earnings management opportunistic or beneficial? An agency theory perspective. International Review of Financial Analysis, 17(3), 622–634. https://doi.org/10.1016/j.irfa.2006.10.005

Johari, N. H., Saleh, N. M., Jaffar, R., & Hassan, M. S. (2009). The influence of board independence, competency and ownership on earnings management in Malaysia. International Journal of Economics and Management, 2(2), 281–306.

Koh, P. S. (2005). Institutional ownership and income smoothing: Australian evidence. Accounting Research Journal, 18(2), 93–110. https://doi.org/10.1108/10309610580000678

La Porta, R., Lopez‐de‐Silanes, F., Shleifer, A., & Vishny, R. W. (1997). Legal determinants of external finance. The Journal of Finance, 52(3), 1131–1150. https://doi.org/10.1111/j.1540-6261.1997.tb02727.x

Leuz, C., Nanda, D., & Wysocki, P. D. (2003). Earnings management and investor protection: an international comparison. Journal of Financial Economics, 69(3), 505–527. https://doi.org/10.1016/S0304-405X(03) 00121-1

Meckling, W. H., & Jensen, M. C. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure.Journal of Financial Economics,3(4), 305–360.

Nazir, M. S., & Afza, T. (2018). Does managerial behavior of managing earnings mitigate the relationship between corporate governance and firm value? Evidence from an emerging market. Future Business Journal, 4(1), 139–156. https://doi.org/10.1016/j.fbj.2018.03.001

Nugrahanti, T. P. (2016). Risk assessment and earning management in banking of Indonesia: Corporate governance mechanisms. Global Journal of Business and Social Science Review, 4(1), 1–9.

Parfet, W. U. (2000). Accounting subjectivity and earnings management: A preparer perspective. Accounting Horizons, 14(4), 481–488. https://doi.org/10.2308/acch.2000.14.4.481

Roychowdhury, S. (2006). Earnings management through real activities manipulation. Journal of Accounting and Economics, 42(3), 335–370. https://doi.org/10.1016/j.jacceco.2006.01.002

Saona, P., & Muro, L. (2018). Firm-and country-level attributes as determinants of earnings management: An analysis for Latin American firms. Emerging Markets Finance and Trade, 54(12), 2736–2764. https://doi.org/10.1080/1540496X.2017.1410127

Scott, W. R. (2003). Financial accounting theory (5th ed). Prentice Hall.

Spohr, J. (2005). Essays on earnings management [Doctorla dissertation]. Swedish School of Economics and Business Administration. https://helda.helsinki.fi/server/api/core/bitstreams/4792ef8d-1978-4a42-b963-33c77476e14f/content

Tabassum, N., Kaleem, A., & Nazir, M. S. (2014). Earnings management through overproduction and subsequent performance: An empirical study in Pakistan. International Journal of Indian Culture and Business Management, 9(3), 267–282. https://doi.org/10.1504/IJICBM. 2014.064693

Tabassum, N., Kaleem, A., & Nazir, M. S. (2015). Real earnings management and future performance. Global Business Review, 16(1), 21–34. https://doi.org/10.1177/0972150914553505

Türegün, N. (2020). Does financial crisis impact earnings management? Evidence from Turkey.Journal of Corporate Accounting & Finance,31(1), 64–71. https://doi.org/10.1002/jcaf.22418

Watts, R. L., & Zimmerman, J. L. (1986). Positive accounting theory. Prentice Hall.

Weisbach, M. S. (1988). Outside directors and CEO turnover. Journal of Financial Economics, 20(1), 431–460. https://doi.org/10.1016/0304-405X(88)90053-0

Whittington, G. (1987). Positive accounting: A review article. Accounting and Business Research, 17(68), 327–336. https://doi.org/10.1080/00014788.1987.9729816

Yang, C. Y., Lai, H. N., & Tan, B. L. (2008). Managerial ownership structure and earnings management. Journal of Financial Reporting and Accounting, 6(1), 35–53. https://doi.org/10.1108/19852510880000634

Yimenu, K. A., & Surur, S. A. (2019). Earning management: From agency and signalling theory perspective in Ethiopia.Journal of Economics, Management and Trade,24(6), 1–12.

Zang, A. (2012). Evidence on the trade-off between real activities manipulation and accrual-based earnings management. The Accounting Review, 87(2), 675–703. https://doi.org/10.2308/accr-10196

[1] The additional cost of monitoring agents in the principal-agent relationship.

[2] The sample of developed economies includes the USA, UK, Hong Kong, Italy, Japan, Canada, Australia, France, Switzerland, Spain, and Sweden. Whereas, developing economies include Brazil, Malaysia, Russia, India, Indonesia, China, Turkey, Thailand, Poland, Israel, and Pakistan.

[3]As estimated by residuals of Larcker and Richardson's (2004) model.

[4]As estimated by residuals of models proposed by Roychowdhury's (2006) Model