| Review | Open Access |

|---|

Impact of Financial Independence and Societal Expectations on the Role Played by Women in Household Dynamics |

|

|---|

Saima Shafiullah and Asma Jabeen*

Department of Economics, COMSATS University-Islamabad Campus, Islamabad, Pakistan

The current study aimed to link the societal challenges, wage discrimination, and financial independence with household dynamics of women. The research hypotheses were tested using a questionnaire survey and data was collected from the residents of Islamabad, Pakistan. Data was collected for 253 respondent women across diverse marital statuses, such as single, married, divorced, and widowed. For assessing the reliability of the study model, Composite Reliability (CR) and Average Variance Extracted (AVE) were used. By employing Structural Equation Modelling (SEM), the results demonstrated that progression in financial independence and financial decision-making of women could considerably enhance their specific role and interaction within a household. Similarly, societal expectations and women’s age also directly affect the household dynamics for women. On the other hand, societal challenges and workplace discrimination have no significant impact on the household dynamics for women. These results show the need for legislation which may remove obstacles to financial independence and financial decision-making of women in order to ensure their empowerment in family dynamics.

1. INTRODUCTION

The term “economic independence” means that an individual must be financially independent and self-sufficient. In the light of economic empowerment, financial independence would be a crucial step towards gender equality. In order to improve the economic empowerment of women, there is a need to invest in the education and health sectors of women. Furthermore, women should also be provided with stable job opportunities. Financial independence of women is not only a way to become individually empowered; however, it also significantly affects household dynamics. A reduction in structural barriers, such as unwritten cultural rules and the gender wage gap, makes it possible for women to attain economic freedom. Simultaneously, the rise in women's financial independence has been credited with family transitions in economic thought, particularly shifts in the gender role (Raybould & Sear, 2021). In many studies, paid work is considered an obstacle that delays establishing permanent relationships, marriage, and having children (Lesthaeghe, 2010). Some studies have focused on the exploration of factors affecting the reduction in male wages, declining labor force participation for men, and labor market uncertainty (Binder & Bound, 2019). At the same time, it is equally important to address the gender inequality in individual-oriented institutions as well as the gender inequality in family-oriented institutions. It would not only result in raising the fertility from low levels in developed countries but also help to achieve the lower fertility in less-developed countries (McDonald, 2000). Studies indicate that women with greater financial independence experience less family violence; on the other hand, financial dependency can trap them in abusive relationships (Abramsky et al., 2023). This relationship between financial independence and less family violence against women highlights the importance of economic empowerment of women as a means to improve women's safety.

A woman’s financial independence leads towards more equitable relationships between partners. Financially-sound women feel more empowered to negotiate roles and responsibilities, leading towards a balanced distribution of household roles. Grabka et al. (2013) argued that when both partners contribute financially, they experience less stress related to finances and are better equipped to focus on challenges together.

In many traditional Asian households, the older male members of the household select the partner for their daughters to get married. Similarly, the daughter-in-law is expected to be obedient to her mother-in-law who has the authority of the entire household. The parental character is mostly assumed from the grandfather, grandmother, and relatives (Patel, 2021). Although, modernization has taken place in urban areas, gender patterns have remained almost the same in urban areas (Farooq, 2020). These traditional gender roles lead towards conflicts within households, when women are engaged with the difficulty of balancing professional careers with caregiving responsibilities. Furthermore, lack of financial literacy and limited access to resources hinder women's ability to make economic decisions. Moreover, women are not considered important in financial matters and they often rely upon the male family members or their partners for guidance (Binsuwadan et al., 2024). In such situations, dominating partners mostly impose financial resource restrictions to exert power and control (Karmaliani et al., 2012).

In Pakistan, there are mainly three generations living together, comprising grandparents, adult children, and grandchildren. Cultural expectations dictate that women must prioritize family responsibilities over career progression. Hence, it creates a challenging environment for women seeking financial independence. Therefore, to improve women's safety and liberty, the discussion above highlights how crucial it is to support their financial independence. The global labor force participation rate of women is 47%, while it is 72% for men (Mukhopadhyay, 2023). In developing countries, such as Pakistan, the statistics for women are even lower. Therefore, women's empowerment in marriages and their financial freedom are key requirements in Pakistan. A United Nations Development Programme (UNDP) study has revealed that a working woman is more likely to have a say in household decisions and to raise her voice for her rights in families (Amaral et al., 2025).

The majority of earlier studies have used both qualitative and quantitative methods to examine how financial inclusion affects women's empowerment. However, there is limited research on how cultural norms and financial independence together affect women’s roles in household dynamics. This study aimed to fill these gaps by examining how social challenges and financial independence impact women's household dynamics in the city of Islamabad, Pakistan.

The rest of the study is organized as follows: After the introduction in section 1, the literature review of the current study is provided in section 2. Section 3 highlights the data span, variables of the study, and methodology employed. Analysis and findings are reported in section 4. Section 5 provides the discussion on the results of the study. Finally, section 6 concludes the study.

Literature Review

Table 1 represents the existing literature highlighting the variables affecting women's financial independence.

Table 1

Review of the Existing Literature

|

Author(s) |

Study Focus |

Summary |

|---|---|---|

|

Wijewardana and Dedunu (2017) |

Impact of microfinance on female entrepreneurs in Mihinthale. |

The study determined that microfinance access significantly enhances women's empowerment by improving their economic capacities. |

|

Bhatia and Singh (2019) |

Financial inclusion’s impact on women’s empowerment in urban slums. |

Significant impact of financial inclusion was observed; challenges include the need for customized financial services. |

|

Mikolai et al. (2020) |

Connections between family transitions and housing. |

The study examined how family formation impacts housing conditions, calling for more in-depth research on housing quality on relationship dynamics. |

|

Bhatpahari (2021) |

Gender equality and financial independence. |

Financial independence is linked to gender equality; challenges include societal barriers to empowerment. |

|

Mirpourian et al. (2021) |

Women's economic empowerment and financial inclusion. |

The study found a strong link between financial inclusion and economic empowerment, suggesting policies are like equal inheritance rights to promote women's participation. |

|

Misra et al. (2021) |

Women's role in financial decision-making in rural India. |

The study emphasized the need for education and financial literacy to improve women’s participation in financial decision-making, particularly in rural areas. |

|

Tarar (2022) |

Women's financial status, autonomy, and household bargaining in Punjab. |

This study explored how women's financial independence affects their bargaining power in household decision-making. Moreover, it emphasized the importance of financial empowerment and policy changes to improve women's roles in the family. |

|

Rughoobur-Seetah et al. (2023) |

Legal measures for women’s financial independence in SIDS. |

The authors investigated factors affecting women’s financial independence, emphasizing the role of legal measures to overcome gender disparities. |

|

Anusuya and Reena (2024) |

Financial assistance’s role in women’s entrepreneurial success. |

Positive effects of financial aid were observed; challenges include barriers to financial access and business sustainability. |

|

Bhojani et al. (2024) |

Women’s economic empowerment and family dynamics in Mwanza, Tanzania. |

Economic empowerment affects family dynamics; challenges include shifting gender norms and support for women’s workforce participation. |

|

Chikwe et al. (2024) |

Financial literacy’s role in women’s empowerment. |

The study highlighted the importance of gender-responsive policies; challenges include cultural and socioeconomic barriers. |

|

Javeed (2024) |

Women's empowerment and financial inclusion. |

The study highlighted barriers to women's access to formal financial services as well as suggested tailored financial products and literacy programs. |

|

Kaushik et al. (2024) |

Women’s financial independence and decision-making. |

Financial independence is supported by social and familial factors; challenges include limited financial literacy and support. |

|

Mishra et al. (2024) |

Impact of social support, legal frameworks, and financial barriers on women’s businesses. |

Social support and legal frameworks are crucial; challenges include overcoming legal and financial obstacles. |

|

Pemasiri and Swarnapali (2024) |

Microfinance’s impact on women’s empowerment in entrepreneurship. |

The study observed a positive impact on empowerment; challenges include limited policy support for microfinance access. |

|

Sánchez‐Mira (2024) |

Female breadwinning and gender role challenges during the Great Recession. |

The study highlighted the female breadwinning challenges, insufficient gender roles, and conflicts that arise from unequal household contributions. |

|

Ankita (2025) |

Indian women entrepreneurs and their contribution to financial independence. |

The study identified challenges faced by female entrepreneurs in India, advocating for policies to support women’s entrepreneurship and financial independence. |

|

Mboli and Jude (2025) |

Gender disparities in financial services. |

Women rely on costly alternatives; challenges include limited access to stable financial options. |

Methodology

The research is cross-sectional in nature, relying on primary data collected on a single point in time from the residents of the city of Islamabad, Pakistan.

Data and VariablesHousehold Dynamics (Hd)

This dependent variable reviews the roles, duties, and procedures of decision-making that happens in a household. It deals with how power relations, interactions and role allocation evolve or change due to internal and external influences. Most often, changes in household dynamics reflect larger changes influenced by factors associated with the workplace discrimination, social expectations, and financial independence.

Progression in Financial Independence (Fi)

This independent variable reflects gaining control over income, savings, and overall resources while reducing reliance on others. The key to changing household roles, influencing decision-making authority, and empowering women is financial independence. Financially-independent women may facilitate more balanced relationships in the home and may break gender stereotypes in the family (Mboli & Jude, 2025). Progression in financial independence is a powerful tool that increases the bargaining power of women within the household by direct contribution to household resources. Therefore, it plays a major role in societal and familial transformations.

H0: The progression in financial independence has no significant effect on household dynamics.

H1: The progression in financial independence has a significant effect on household dynamics.

Financial Decision-making (Fd)This variable assesses the level of a person's involvement in making decisions about household finances. It includes budgeting, saving, and investing. Active engagement, therefore, represents a change from traditional roles to empowerment. Thus, it promotes family autonomy and economic literacy. Women who have their role in financial decision-making feel more empowered, which helps in improving family stability (Bhatia & Singh, 2019). The study indicated that financial inclusion has a positive influence on social, political, and economic dimensions of women empowerment.

H0: Financial decision-making has no significant impact on household dynamics.

H1: Financial decision-making has a significant impact on household dynamics.

Societal Challenges (S)This independent variable consists of obstacles that limit the opportunities of women through societal norms and structural injustices. It impacts household dynamics and financial independence of women through work, education, and resource availability. Such social constraints prevent women from obtaining economic and other opportunities of employment (Wijewardana and Dedunu, 2017), as well as hamper their financial independence and decision-making in their families. The findings indicated that women’s access to loans, non-financial services, and better repayment procedures positively and significantly affect the empowerment of women entrepreneurs in Mihinthale Pradeshiya Sabha area.

H0: Societal challenges have no significant effect on household dynamics.

H1: Societal challenges have a significant effect on household dynamics.

Societal Expectations (Exp)This variable focuses on social and cultural values that set norms for behaviour and responsibility, both inside households and in society at large. This notion was further supported by Khairullah (2022), who argued that changing social norms are increasingly recognizing women's roles outside the household. Thus, it allows them to play a more significant role in decision-making within the household. Traditional expectations often enforce the dominant gender roles and power structures. Therefore, changes in social expectations can deeply influence decision-making procedures and the distribution of household responsibilities.

H0: Societal expectations have no significant effect on household dynamics.

H1: Societal expectations have a significant effect on household dynamics.

Workplace Discrimination (Wd)The biases or unfair treatments faced by working individuals within the professional settings are termed as ‘workplace discrimination’. Mirpourian et al. (2021) concluded that gender-based employment discrimination does not allow women to have promotions. This eventually fails them in gaining financial independence since they cannot achieve what is called economic empowerment. According to the feminist economics, women’s roles should be recognized in all fields, for instance domestic and economic affairs.

Gender equality impacts career progression, financial security, and job satisfaction. Since employment is the crucial ingredient for economic empowerment, these usually have a knock-on effect on household dynamics, affecting financial independence and decision-making capacity.

H0: Workplace discrimination has no significant effect on household dynamics.

H1: Workplace discrimination has a significant effect on household dynamics.

Methodological FrameworkThis section discusses the research design, sample selection, and data collection method. Details about the questionnaire construction, reliability, validity, and analytical tools are also provided in this section.

DataThe research hypotheses were tested using a questionnaire survey and data was collected from the residents of Islamabad. The analysis comprised primary data collected by using a convenience sampling technique. Sample size was calculated with the formula:

S=Z^2×P×( (1-P))/M^2

where,

S = Sample size

Z = Z-score for a confidence level of 95% (t-value = 1.98)

P = Proportion of the population assumed to have the characteristic of interest (taken as 0.5 for maximum variability)

M = Margin of error (5%, or 0.05)

QuestionnaireThe current study employed a structured questionnaire to collect the data for analysis. The questionnaire comprised various separate sections.

Demographic InformationThis section of the questionnaire collected basic demographic details of respondents to understand their socioeconomic backgrounds. Key variables included:

Age: Respondents' ages in years

Marital Status: Single, married, divorced, or widowed

Number of Dependents: Total individuals financially or physically dependent on the respondent

Level of Education: Highest level of formal education achieved

Employment Status: Current occupational status (e.g., employed, unemployed, homemaker, student)

Approximate Monthly Income: Income categories

Sampling StrategyA convenience sampling technique, although quick and cost-effective, is based on the accessibility of the participants. This approach introduces selection bias in the sample. However, by including women across diverse marital statuses, such as single, married, divorced, and widowed. the study attempted to minimize the biases and created heterogeneity in the data.

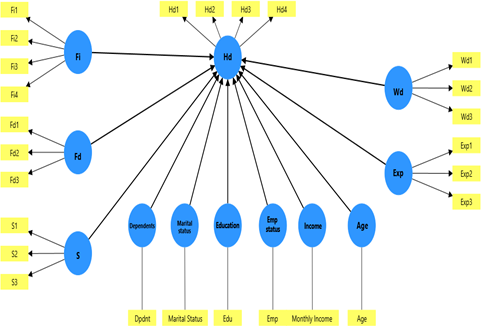

Conceptual FrameworkItems related to progression in financial independence, financial decision-making, societal challenges, societal expectations, and workplace discrimination were included to evaluate their influence on the dependent variable.

Items on household dynamics assess subjective perspectives about roles, relationships, and decision-making within the household. Based on the above discussion, the conceptual framework is presented in Figure1 below.

Figure 1

Structural Model

The structural model describes the relationship between the latent variables of the study. The path parameter coefficients of Partial Least Squares (PLS) are determined from the bootstrapping sample of 253 questionnaires.

Convergent ValidityThe convergent validity was tested to determine whether or not indicator variables portray the latent variables in important and clear ways. Convergent validity also involves tests on both validity and reliability. High values of the standardized loading factor are a manifestation of good convergent validity. As Hair et al. (2010) noted, any value ≥ 0.5 means a convergent validity has been achieved. The importance of these findings is that the structural model only depends on reliability for measuring the indicators, which truly represent the latent variables, leading to accuracy and authenticity.

Reliability StatisticsThe reliability test measures the consistency of measurement indicators for latent variables. For assessing the reliability of the study model, Composite Reliability (CR) and Average Variance Extracted (AVE) were used.

Results and Discussion

This section presents the results obtained from the data analysis using SEM. It begins with the demographic profile of the respondents and proceeds to evaluate the structural relationship between the variables.

Demographic InformationTable 2 presents the demographic statistics of households from which the data were collected. The statistics reported in Table 2 showed that age is a demographic attribute that influences the extent to which a respondent may make choices and become responsible. The majority of respondents were less than 25 years with a percentage of 46.20%, followed by those aged between 25 and 34 years with a percentage of 25.69% of all people in the group. Others were between 35–44 years with a percentage of 15.40%, some were between 45 and 54 years of age group with a percentage of 8.69%, while 55 years and older had a percentage of 3.95%. Table 2 showed that the majority of respondents were single (46.20%), closely followed by those who had been married (42.30%). Fewer of them said that they were separated but not divorced (3.10%), the percentage of divorced respondents was 4.30%, while others were widowed (4.10%). Education levels are important since they affect how people think and make choices, especially about money and social issues. Most people (37.20%) said that they had a Master’s degree or higher. Close behind, 29.40% reported having a Bachelor’s degree. It is worth noting that only a small number of respondents (5.50%) had a primary education, showing that the surveyed group had a good level of education.

Another critical factor that determines who owes what financially, to an extent, is their preferences. Most of the respondents said they had 1-2 dependents (46.84%), followed by no dependents (37.15%), while others reported having 3–4 dependents (11.85%). Still, others reported having 5–6 dependents (4.30%) and only 0.80% had 6 or more dependents. Employment status is an important determinant of economic stability and individual choices. Most of the respondents (36.0%) said they were full-time employees. Next, 26.50% said they were part-time employees. Freelancers or contractors made up 17.80% of the respondents. Meanwhile, 14.60% were unemployed and looking for work. A smaller group (5.10%) was unemployed and not looking for work. Monthly income is crucial to understand how financially stable and capable people are. The highest percentage of respondents was between 30,000 and 50,000 PKR per month, with a share of 36.80%.

Table 2

Demographic Characteristics

|

Demographics |

Frequencies |

Percentages (%) |

|---|---|---|

|

Age Under 25 25–34 35–44 45–54 55 and above |

117 65 39 22 10 |

46.20% 25.69% 15.40% 8.69% 3.95% |

|

Marital status Single Married Separated (not divorced) Divorced Widowed Level of Education Primary Education Secondary Education Intermediate Education Bachelor’s Degree Master’s Degree or Higher Number of Dependents None 1–2 3–4 5–6 6+ Employment Status Full-time Employee Part-time Employee Freelancer/Contractor Unemployed (looking for work) Unemployed (not looking for work) Approximate Monthly Income 30,000 - 50,000 PKR 51,000 - 1,00,000 PKR 1,00,000 - 2,00,000 PKR 2,00,000 - 3,00,000 PKR More than 3,00,000 PKR |

117 107 8 11 10

14 29 42 74 94

94 116 30 11 2

91 67 45 37 13

93 65 57 18 20 |

46.20% 42.30% 3.10% 4.30% 4.10%

5.50% 11.50% 16.50% 29.40% 37.20%

37.15% 46.84% 11.85% 4.30% 0.80%

36% 26.50% 17.80% 14.60% 5.10%

36.80% 25.70% 22.50% 7.10% 7.90% |

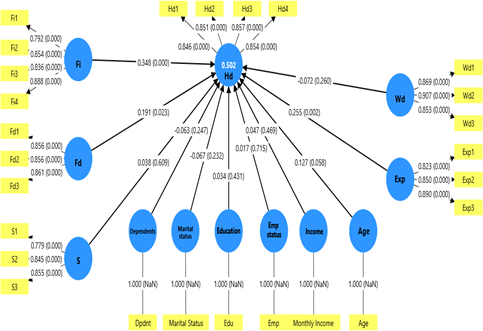

Figure 2

Path Coefficients of Structural Model

Verifying the Structural Model

According to Hair et al. (2010), a value of the standardized loading factor (λ) ≥ 0.05 represents that good convergent validity has been achieved.

The loading factors of all the indicator variables show their contributions to their respective hidden constructs, and all of them reached above the threshold value of 0.5, hence establishing good convergent validity. This ensures that the indicators clearly explain their associated constructs and guarantee valid and reliable measurements for further analysis. The results indicate that the value of R-square of the model is 0.502.

Structural Model Evaluation and Hypothesis Testing

Table 3 presents the values of Cronbach’s alpha, CR, and AVE for the variables of the study.

Table 3

Reliability Test Results

|

Construct |

Items |

Loading Factors |

Cronbach's alpha |

Composite Reliability (rho_a) |

Composite Reliability (rho_c) |

Average Variance Extracted (AVE) |

|

|---|---|---|---|---|---|---|---|

|

Societal Expectations (Exp) |

|

0.817 |

0.833 |

0.890 |

0.731 |

||

|

I feel pressure from others to follow traditional gender roles |

Exp1 |

0.823 |

|

|

|

|

|

|

Social pressures make it hard for women to balance work and family |

Exp2 |

0.850 |

|

|

|

|

|

|

When women earn, people see their role at home differently |

Exp3 |

0.890 |

|

|

|

|

|

|

Progression in Financial Independence (Fi) |

0.864 |

0.870 |

0.908 |

0.711 |

|||

|

My level of financial independence has improved significantly over the past five years |

Fi1 |

0.792 |

|

|

|

|

|

|

Being financially independent has resulted in a more equal sharing of financial duties within my household |

Fi2 |

0.854 |

|

|

|

|

|

|

I actively include my partner/family in long-term financial planning, reflecting my sense of independence |

Fi3 |

0.836 |

|

|

|

|

|

|

My financial independence empowers me to make confident financial decisions |

Fi4 |

0.888 |

|

|

|

|

|

|

Household Dynamics (Hd) |

0.874 |

0.875 |

0.914 |

0.726 |

|||

|

I believe my contribution to the household has improved over time |

Hd1 |

0.846 |

|

|

|

|

|

|

Financial independence has positively impacted the distribution of household responsibilities |

Hd2 |

0.851 |

|

|

|

|

|

|

Financial independence has led to a positive change in my family relationships |

Hd3 |

0.857 |

|

|

|

|

|

|

My contribution to household income strongly influences my relationships with family members |

Hd4 |

0.854 |

|

|

|

|

|

|

Societal Challenges (S) |

0.773 |

0.796 |

0.866 |

0.684 |

|||

|

Societal challenges create significant barriers for women in achieving financial independence |

S1 |

0.779 |

|

|

|

|

|

|

There is enough community support available for women pursuing financial independence |

S2 |

0.845 |

|

|

|

|

|

|

There are systemic barriers in society that prevent women from achieving financial independence |

S3 |

0.855 |

|

|

|

|

|

|

Workplace Discrimination (Wd) |

0.850 |

0.859 |

0.909 |

0.769 |

|||

|

Workplace discrimination has negatively impacted career progression and financial decisions |

Wd1 |

0.869 |

|

|

|

|

|

|

Women are treated unfairly at work, stopping them from earning money freely |

Wd2 |

0.907 |

|

|

|

|

|

|

I have personally experienced workplace discrimination |

Wd3 |

0.853 |

|

|

|

|

|

|

Financial Decision- making (Fd) |

0.820 |

0.821 |

0.893 |

0.735 |

|||

|

Financial independence allows me to take on leadership roles in financial decisions at home |

Fd1 |

0.855 |

|

|

|

|

|

|

Achieving financial independence helps women challenge societal norms and expectations |

Fd2 |

0.856 |

|

|

|

|

|

|

I actively participate in financial planning and budgeting for my household |

Fd3 |

0.861 |

|

|

|

|

|

The structural model describes the relationship between latent variables. The results reported in Table 4 reveal that monthly income has a positive but insignificant influence on household dynamics with a coefficient of 0.047 units and a t-statistic value of 0.724 (< 1.98) at a p-value of 0.469. Age presents a positive and marginally significant influence on household dynamics with a coefficient of 0.127 units and a t-statistic value of 1.899 (< 1.98) at a p-value of 0.058. Educational level has a positive but insignificant influence on household dynamics with a coefficient of 0.034 units and a t-statistic value of 0.787 (< 1.98) at a p-value of 0.431. Employment status also has a positive but insignificant influence on household dynamics with a coefficient of 0.017 units and a t-statistic value of 0.365 (< 1.98) at a p-value of 0.715. Marital status shows a negative but not significant influence on household dynamics with a coefficient of -0.067 units and a t-statistic value of 1.197 (< 1.98) at a p-value of 0.232. The number of dependents also reveals a negative but not significant influence on household dynamics with a coefficient of -0.063 units and a t-statistic value of 1.157 (< 1.98) at a p-value of 0.247.

Financial independence (Fi) has the strongest positive and significant influence on household dynamics with a coefficient of 0.348 units and a t-statistic value of 3.832 (> 1.98) at a p-value of 0.000. Societal challenges (S) have a positive but not significant influence on household dynamics with a coefficient of 0.038 units and a t-statistic value of 0.512 (< 1.98) at a p-value of 0.609. Workplace discrimination (Wd) has a negative but insignificant influence on household dynamics with a coefficient of -0.072 units and a t-statistic value of 1.126 (< 1.98) at a p-value of 0.26.

Finally, financial decision-making (Fd) has a significant positive influence on household dynamics with a coefficient of 0.191 units and a t-statistic value of 2.279 (>1.98) at a p-value of 0.023. Lastly, societal expectations (Exp) have a positive significant positive effect on household dynamics with a coefficient of 0.255 units and a t-statistic value of 3.109 (>1.98) at a p-value of 0.002.

Table 4Results of Marital Status Respondents

Thus, age of women, societal expectations, progression in financial independence, and financial decision-making have a significant impact on role of women in household dynamics.

Discussion

The most significant variable is progression in financial independence (Fi) with β = 0.348 and p < 0.05. It indicates that economic freedom plays a significant role at home in fostering family cohesion. The results are in line with the study carried out by Wijewardana and Dedunu (2017).Financial independence helps women make choices about spending and savings. If more members of the household work, then the family would face fewer financial problems. Household dynamics also significantly improve with the increase in financial decision-making (Fd). A significant positive effect of financial decision-making, with β=0.191, and p < 0.05, reveals that engaging women in financial planning helps improve the decisions made at the household level. The results reveal that if a woman participates in the family’s financial management, more balanced and sensible decisions of the household would be taken.

The finding has supported the argument of Misra et al. (2021), that if a woman is capable to take part in financial matters, she feels more valued. Furthermore, societal expectations (Exp) also exert a significant positive effect on the dynamics of the household. The societal expectations variable is significant and positive with β = 0.255, and p < 0.05, suggesting that normative change also plays a crucial role in shaping household dynamics.

Positive change in social norms makes women assume greater responsibilities within the household as well as decisions made at home and advocate for gender equality. Chikwe et al. (2024) argued that, changing cultural norms regarding gender roles have the potential to revolutionize family dynamics and how tasks are allocated according to the comparative advantage. On the other hand, the impact of workplace discrimination is insignificant with β = -0.072, and p > 0.05. This result indicates that the income sacrificed due to the workplace discrimination may be a small portion of the total household income, where husband is the primary breadwinner. Due to this reason, the household dynamics of women are not affected.

ConclusionThis study used SEM to analyze the data collected from 253 respondents in order to assess how financial independence and societal constraints impact women's home dynamics in Islamabad, Pakistan. The results showed that financial decision-making, progression in financial independence, and social expectations are the significant factors that transform the power and affect positive household dynamics for women. Indirectly, necessity was demonstrated since demographic characteristics, such as marital status, employment status, level of education, number of dependents, monthly income, and job-based discrimination made no significant impact. The findings showed that women in Islamabad are empowered to question conventional home norms as well as actively contribute to the well-being of their families when they are financially independent. The results indicated that social expectations have a positive impact on household dynamics. This means changing standards in Islamabad would improve women's responsibilities in their homes.

Policy RecommendationsThe current study proposed the following recommendations:

- Incentives should be provided to the organizations that promote women to leadership positions and adopt gender-neutral rules at the workplace.

- Women can be empowered through community-based programs focusing on education, skills development, and access to resources that may enable them to overcome social barriers and become economically-independent.

- The organizations should provide women with flexible working hours, maternity leave benefits, and childcare facilities so that women could achieve a balance between work and home life.

- The government should implement various schemes and policies to provide financial assistance, interest-free loans, and business loans to promote economic independence and entrepreneurship among women.

- Literacy programs can be designed to provide women with financial awareness about budgeting, savings, and investment.

Study Limitations and Future Research Agenda

A major limitation of this study is that the analysis exclusively focused on urban households using a convenience sampling methodology. To overcome this limitation in the future, other robust sampling techniques, for instance, stratified random sampling can be employed to incorporate a representative sample from rural households. This would help better understand women’s economic empowerment in Pakistan.

Conflict of Interest

The authors of the manuscript have no financial or non-financial conflict of interest in the subject matter or materials discussed in this manuscript.

Data Availability Statement

Data supporting the findings of this study will be made available by the corresponding author upon request.

Funding Details

No funding has been received for this research.

REFERENCES

Abramsky, T., Guadarrama, D. S., Kapiga, S., Mtolela, G., Madaha, F., Lees, S., & Harvey, S. (2023). Pathways to reduced physical intimate partner violence among women in north-western Tanzania: Evidence from two cluster randomised trials of the MAISHA intervention. PLOS Global Public Health, 3(11), Article e0002497. https://doi.org/10.1371/journal.pgph.0002497

Amaral, S., Sheth, S., Aggarwal, P., Guhu, A., Osama, S., & Shirleen, M. (2025). Women's economic empowerment in Pakistan: An evidence guided toolkit for more inclusive policies. World Bank Group. https://thedocs.worldbank.org/en/doc/e02bd4872b983fc0b4a1809489231e35-0310012024/original/Womens-Economic-Empowerment-in-Pakistan.pdf

Ankita, R. A. (2025). Breaking barriers: A study on the rise of women entrepreneurs in India. Journal of Marketing & Social Research, 2, 717–727. https://doi.org/10.61336/jmsr/25-02-72

Anusuya, B., & Reena, R. (2024). A study on the impact of financial assistance programs for women entrepreneurs with reference to Coimbatore district. ShodhKosh: Journal of Visual and Performing Arts, 5(4), 456–471. https://doi.org/10.29121/shodhkosh.v5.i4.2024.1974

Bhatia, S., & Singh, S. (2019). Empowering women through financial inclusion: A study of urban slum. Vikalpa, 44(4), 182–197. https://doi.org/10.1177/0256090919897809

Bhatpahari, G. (2021). Financial independence of women for gender equality. UGC Care Group 1 Journal, 51(2), 215–1218.

Bhojani, A., Alsager, A., McCann, J. K., Joachim, D., Kabati, M., & Jeong, J. (2024). "If my wife earns more than me, she will force me to do what she wants": Women's economic empowerment and family caregiving dynamics in Tanzania. World Development, 179, Article e106626. https://doi.org/10.1016/j.worlddev.2024.106626

Binder, A. J., & Bound, J. (2019). The declining labor market prospects of less-educated men. Journal of Economic Perspectives, 33(2), 163–190. https://doi.org/10.1257/jep.33.2.163

Binsuwadan, J., Elhaj, M., Bousrih, J., Mabrouk, F., & Alofaysan, H. (2024). The relationship between financial inclusion and women's financial worries: Evidence from Saudi Arabia. Sustainability, 16(19), Article e8317. https://doi.org/10.3390/su16198317

Chikwe, C. F., Kuteesa, K. N., & Ediae, A. A. (2024). Gender equality advocacy and socio-economic inclusion: A comparative study of community-based approaches in promoting women's empowerment and economic resilience (2022). International Journal of Scientific Research Updates, 8(2), 110–121. https://doi.org/10.53430/ijsru.2024.8.2.0066

Farooq, A. (2020). Gendered perceptions in Punjab, Pakistan: Structural inequity, oppression and emergence. Journal of Gender Studies, 29(4), 386–402. https://doi.org/10.1080/09589236.2019.1635876

Grabka, M. M., Marcus, J., & Sierminska, E. (2013). Wealth distribution within couples. IZA Discussion Papers. https://ideas.repec.org/p/iza/izadps/dp7637.html

Hair, J. F., Black, W. C., & Babin, B. J. (2010). Multivariate data analysis: A global perspective. Pearson Education.

Javeed, I. (2024). A study on financial inclusion and women empowerment in Jammu district. Journal of Business, Ethics and Society, 4(2), 1–13. https://doi.org/10.61781/4-2II2024/3bmlm

Karmaliani, R., Pasha, A., Hirani, S., Somani, R., Hirani, S., Asad, N., Cassum, L., & McFarlane, J. (2012). Violence against women in Pakistan: Contributing factors and new interventions. Issues in Mental Health Nursing, 33(12), 820–826. https://doi.org/10.3109/01612840.2012.718046

Kaushik, M. B., Rajharia, P., Soni, S., Jain, A., & Singh, J. (2024). Empowering women through education: A roadmap for financial and personal independence. European Economic Letters, 14(3), 1200–1207. https://doi.org/10.52783/eel.v14i3.1881

Khairullah, K. (2022). Changes in women's social roles and functions in gender dichotomy resistance. Perspektif, 11(3), 990–996. https://doi.org/10.31289/perspektif.v11i3.6536

Lesthaeghe, R. (2010). The unfolding story of the second demographic transition. Population and Development Review, 36(2), 211–251. https://doi.org/10.1111/j.1728-4457.2010.00328.x

Mboli, M. V., & Jude, F. A. (2025). Financial literacy and women's empowerment: The impact on family size and economic independence. Texila International Journal of Management, 11(1), 1–10. https://doi.org/10.21522/TIJMG.2015.11.01.Art019

McDonald, P. (2000). Gender equity in theories of fertility transition. Population and Development Review, 26(3), 427–439.

Mikolai, J., Kulu, H., & Mulder, C. (2020). Family life transitions, residential relocations, and housing in the life course: Introduction to the special collection on separation, divorce, and residential mobility. Demographic Research, 43, 35–58. https://doi.org/10.4054/DemRes.2020.43.2

Mirpourian, M., Torres, M., & Kelly, S. (2021). Determinants of women's financial inclusion and economic empowerment. Women World's Banking. https://www.womensworldbanking.org/wp-content/uploads/2021/06/2021_Determinants_of_Womens_Financial_Inclusion.pdf

Mishra, S., Mishra, A., Singh, S. P., & Upadhyay, B. (2024). Investigating the impact of financial barriers, regulatory landscape and societal backing on women-led enterprises in India: An empirical investigation using PLS-SEM. European Economic Letters, 14(1s), 236–244. https://doi.org/10.52783/eel.v14i1s.1364

Misra, R., Srivastava, S., Mahajan, R., & Thakur, R. (2021). Decision making as a contributor for women empowerment: A study in the Indian context. Journal of Comparative Asian Development, 18(1), 79–99. https://doi.org/10.4018/JCAD.2021010104

Mukhopadhyay, U. (2023). Disparities in female labour force participation in South Asia and Latin America: A review. Review of Economics, 74(3), 265–288. https://doi.org/10.1515/roe-2022-0061

Patel, D. (2021). Experience of gender role expectations and negotiation in second generation Desi couples [Doctoral dissertation, Antioch University]. AURA. https://aura.antioch.edu/etds/753

Pemasiri, B. W. N. K., & Swarnapali, R. M. N. C. (2024). Impact of microfinance on empowerment of women entrepreneurship: Evidence from Rathnapura District. Wayamba Journal of Management, 15(1), 112–127. https://doi.org/10.4038/wjm.v15i1.7620

Raybould, A., & Sear, R. (2021). Children of the (gender) revolution: How gendered division of labour influences fertility. Population Studies, 75(2), 169–190. https://doi.org/10.1080/00324728.2020.1851748

Rughoobur-Seetah, S., Hosanoo, Z., & Balla Soupramanien, L. D. (2023). Financial independence of women – The impact of social factors on empowerment in small island developing states (SIDS). International Journal of Organizational Analysis, 31(6), 2383–2408. https://doi.org/10.1108/IJOA-10-2021-2980

Sánchez-Mira, N. (2024). (Un)doing gender in female breadwinner households: Gender relations and structural change. Gender, Work and Organization, 31(4), 1196–1213. https://doi.org/10.1111/gwao.12775

Tarar, M. (2022). Women's financial status, autonomy and household bargaining in the Punjab: A feminist analysis. Pakistan Social Sciences Review, 6(2), 183–196 https://doi.org/10.35484/pssr.2022(6-II)17

Wijewardana, W. P., & Dedunu, H. (2017). Impact of microfinance to empower female entrepreneurs. International Journal of Business Marketing and Management, 2(7), 1–6